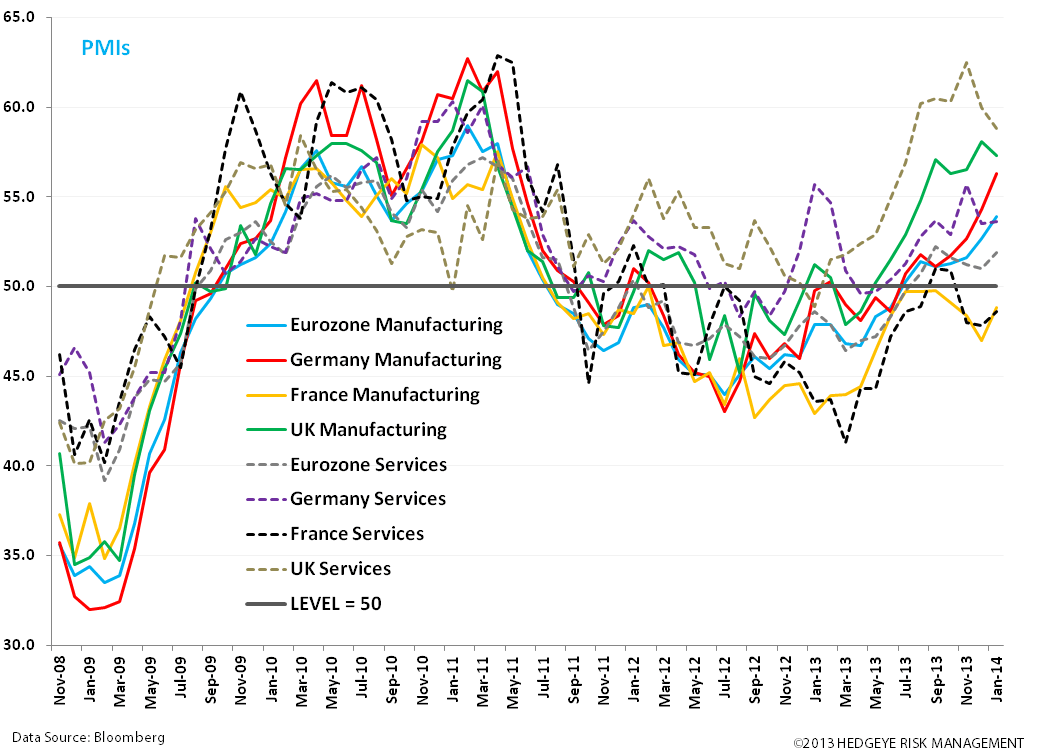

Strong European PMIs, a reduction in sovereign debt levels, and outperformance from the periphery (of note is Spain) continue to support our Q4 2013 and Q1 2014 macro themes of #EuroBulls and #GrowthDivergences, respectively, that forecast a bullish growth recovery in Europe, specifically with a bullish outlook for UK and German equities and the British Pound vs the USD.

Preliminary January PMIs were released this morning from the Eurozone, Germany, and France. The data showed a pop month-over-month for the Eurozone and Germany; in fact the Eurozone Composite PMI expanded at the fastest pace in two-and-a-half years! While France improved, it remains grounded under the 50 line (representing contraction) and continues to negatively diverge versus the region. UK PMIs took a slight leg down in January, however remain at/near 3-year highs.

- Eurozone PMI Manufacturing 53.9 JAN Prelim (exp. 53) vs 52.7 DEC

- Eurozone PMI Services 51.9 JAN Prelim (exp. 51.4) vs 51 DEC

- Eurozone PMI Composite 53.2 JAN Prelim (exp. 52.5) vs 52.1 DEC

- Germany PMI Manufacturing 56.3 JAN Prelim (exp. 54.6) vs 54.3 DEC

- Germany PMI Services 53.6 JAN Prelim (exp. 54) vs 53.5 DEC

- France PMI Manufacturing 48.8 JAN Prelim (exp. 47.5) vs 47 DEC

- France PMI Services 48.6 JAN Prelim (exp. 48.1) vs 47.8 DEC

Separately, Eurostat data showed that Eurozone government debt in Q3 2013 fell for the first time in nearly six years, signaling the region’s austerity push is in fact reducing fiscal excesses, despite debt levels still well above the EU's 60% limit. The UK remains our poster child for the positive economic impact of its early decision in the ‘crisis’ to reduce its fiscal excesses (debt and deficit).

The data shows that debt across the 17 countries in the region stood at €8.842T in Q3 2013, down from €8.875T in Q2 2013, or slipped to 92.7% as a % of GDP from 93.4% in the previous quarter.

The highest ratios of government debt to GDP at the end of the third quarter of 2013 were recorded in Greece (171.8%), Italy (132.9%), Portugal (128.7%) and Ireland (124.8%), and the lowest in Estonia (10.0%), Bulgaria (17.3%) and Luxembourg (27.7%). Germany's debt levels stands at 78.4%, France 92.7%, Spain 93.4%, and UK 89.5%. (two chart courtesy of Eurostat.com)

When comparing current debt versus Q3 2012, 23 of the 28 member states registered an increase in their debt to GDP ratio at the end of Q3 2013, and 5 a decrease. The highest increases in the ratio were recorded in Cyprus (+25.3%), Greece (+19.9%), Spain (+14.3%) and Slovenia (+14.1%), while decreases were recorded in Germany (-2.8%), Latvia (-2.0%), Bulgaria (-1.4%), Denmark (-0.9%) and Lithuania (-0.8%).

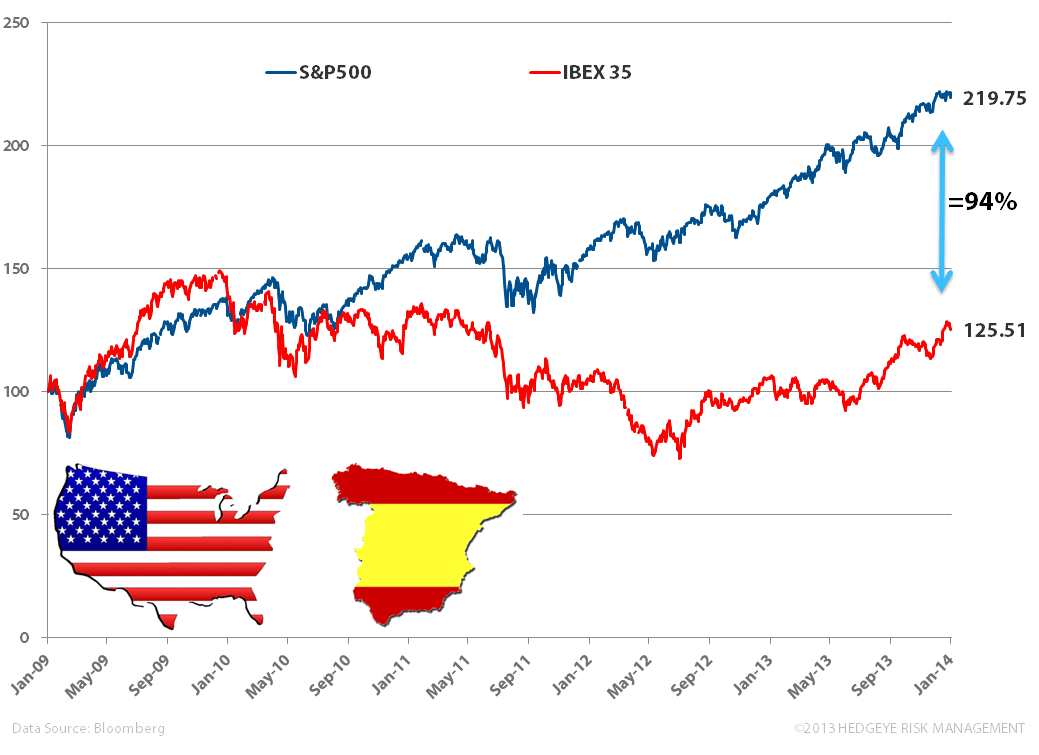

Spain’s Push and Pull Recovery is Encouraging

We noted this week the peripheral equity markets of Europe are off to a quick outperformance in 2014. We continue to see positive signs of economic recovery in Spain, and remain well aware of the structural overhangs that still linger, including high unemployment (26.03% in Q4 vs 25.98% in Q3). As we show in the chart below, if we look at Spain’s equity (IBEX35) performance over the last 5 years, there’s plenty of “catch-up” in the spread. Below are some recent data points to consider when sizing up Spain:

- Bond Issue Raises Record Orders: Spain's 10-bond issue raised a record €10B – and orders received were almost 4x oversubscribed. ~ 65% were sold to investors outside the country and institutional investors participation was the second biggest since the euro's launch in 1999, rivaled only by the €44B in demand from the debut deal from the EFSF.

- Spain formally exited its bailout program for banks: the €41B borrowed and earmarked for banks (out of the €100B made available in return for the Spanish banking sector reforms and a range of austerity measures) has been paid back. European Commission's Olli Rehn said the Spanish program had worked and cited more stable financial markets, increased liquidity for banks, rising deposits and improved access to funding markets.

- Bad Loans Spike: Bank of Spain data showed that bad loans at Spanish banks as a percentage of total lending reached a fresh record high of 13.08% in November, up from 12.99% in October. The value of bad loans rose on the month by €1.5B to €192.5B.

Matthew Hedrick

Associate