Two More Weeks Until the Market Gets What's Going On

The initial jobless claims data continues to paint a picture of a strengthening, though not overheating, recovery in the labor market. The most important takeaway that varies from consensus is that the data is sharply at odds with the very weak December NFP print that caused a rally in long bonds. We expect, based on this claims data, that dynamic to reverse when the January NFP print is released two weeks from tomorrow, on Friday, February 7th.

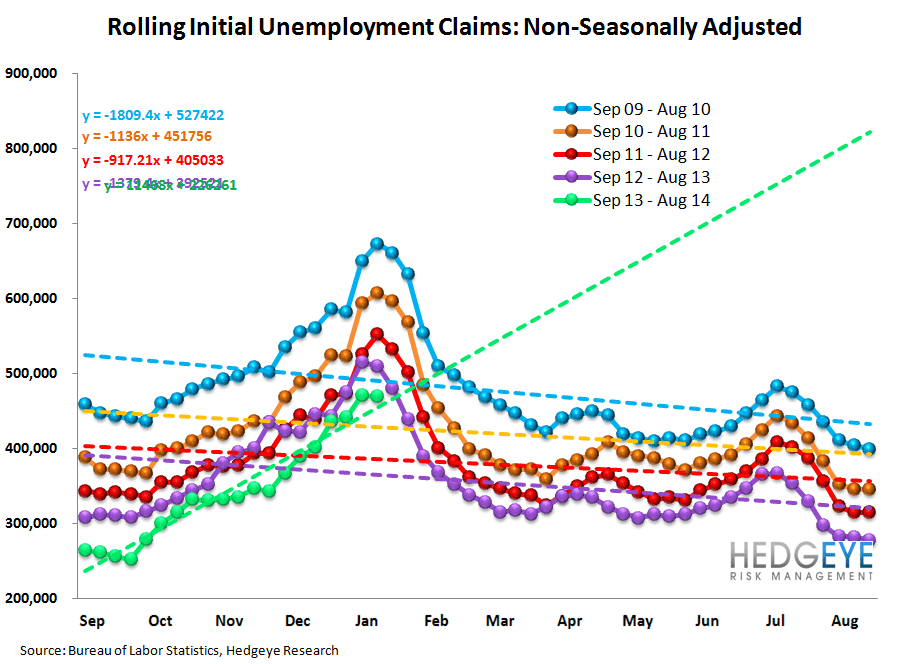

Our preferred measure of looking at the claims data remains the year-over-year rate of change in the rolling non-seasonally adjusted initial claims. This week that measure was 469,817, which was down 7.9% from the 510,350 at the same time last year. This compares with the previous week's rate of improvement of 8.5%. On the margin, there was modest deceleration in the rate of improvement, but not enough to warrant emphasis. On a single week basis, an inherently more volatile series, the Y/Y change was 5.8% better, which was better than the previous week's 4.3% improvement.

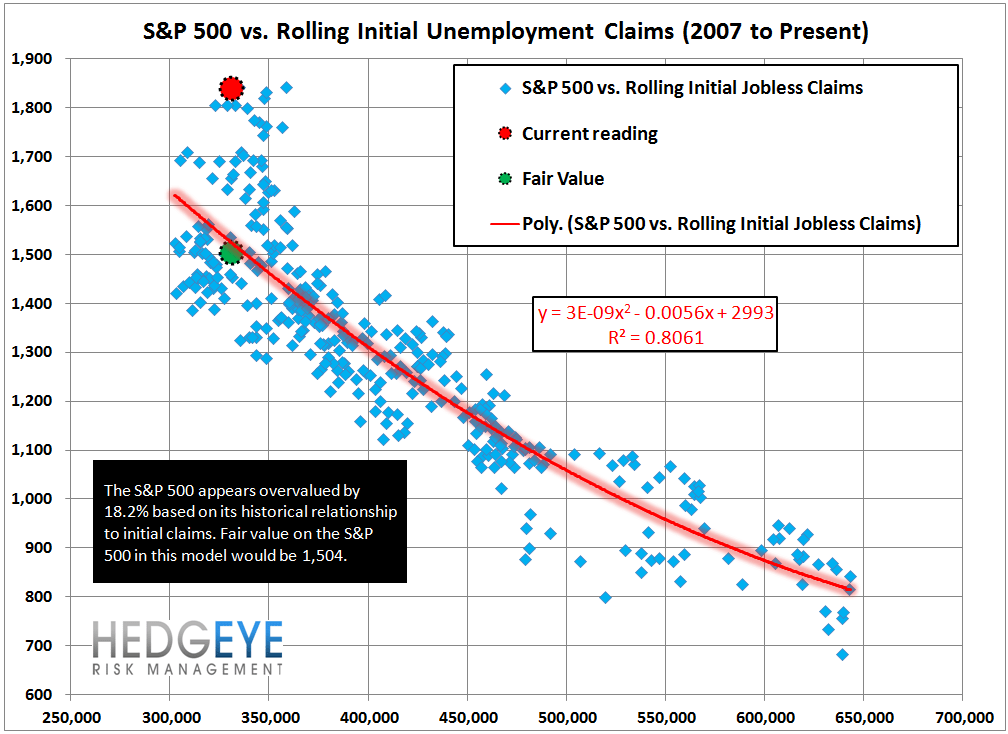

We continue to expect the 10-year treasury to re-test 3.00% on strengthening labor data that will become more apparent in ~2 weeks time. For more info on which stocks are best and worst positioned for a rise in rates, see our note from November 22 entitled "#Rates-Rising: A Current Look at Rate Sensitivity Across Financials", which can be found HERE.

The Numbers

Prior to revision, initial jobless claims were unchanged at 326k WoW, as the prior week's number was revised down by -1k to 325k.

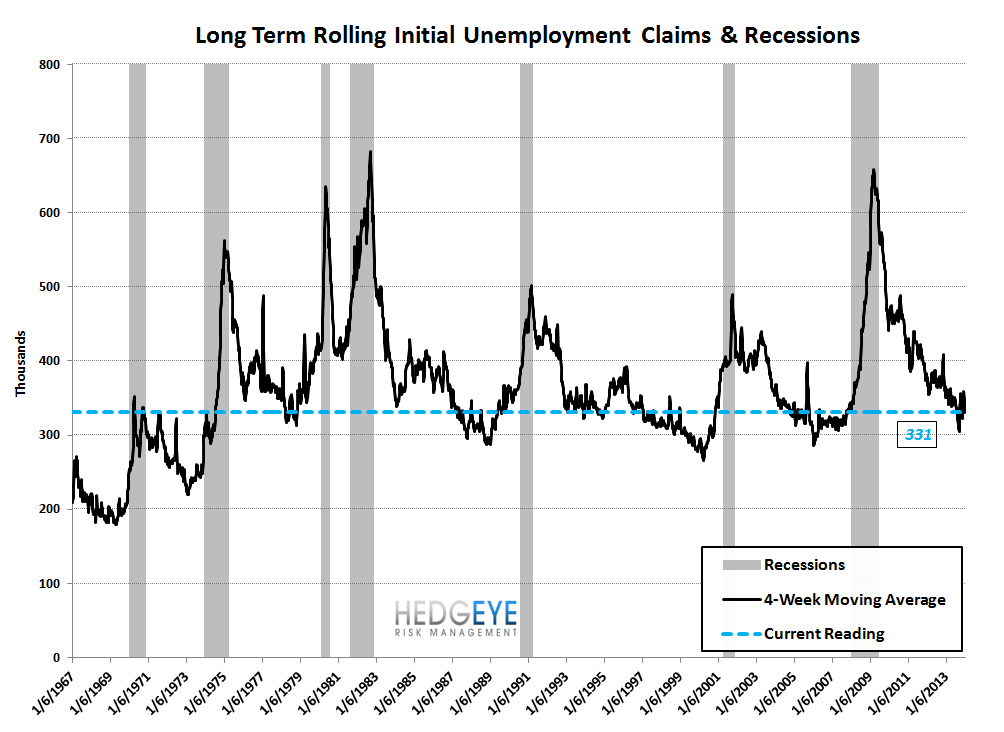

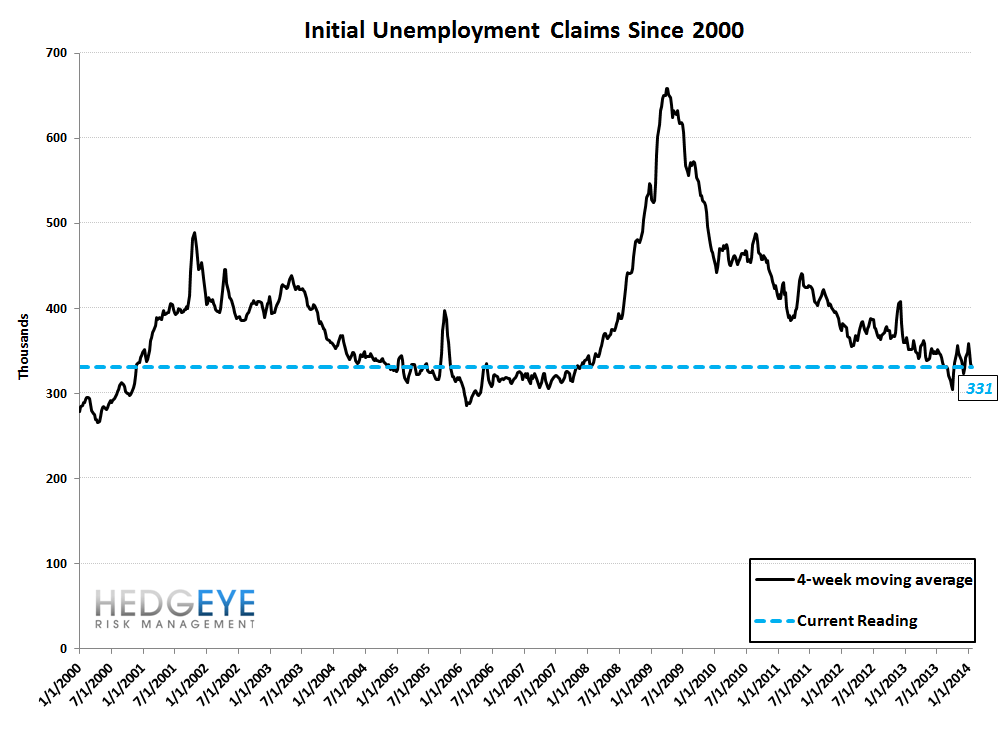

The headline (unrevised) number shows claims were higher by 1k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -3.75k WoW to 331k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -7.9% lower YoY, which is a modest sequential deterioration versus the previous week's YoY change of -8.5%

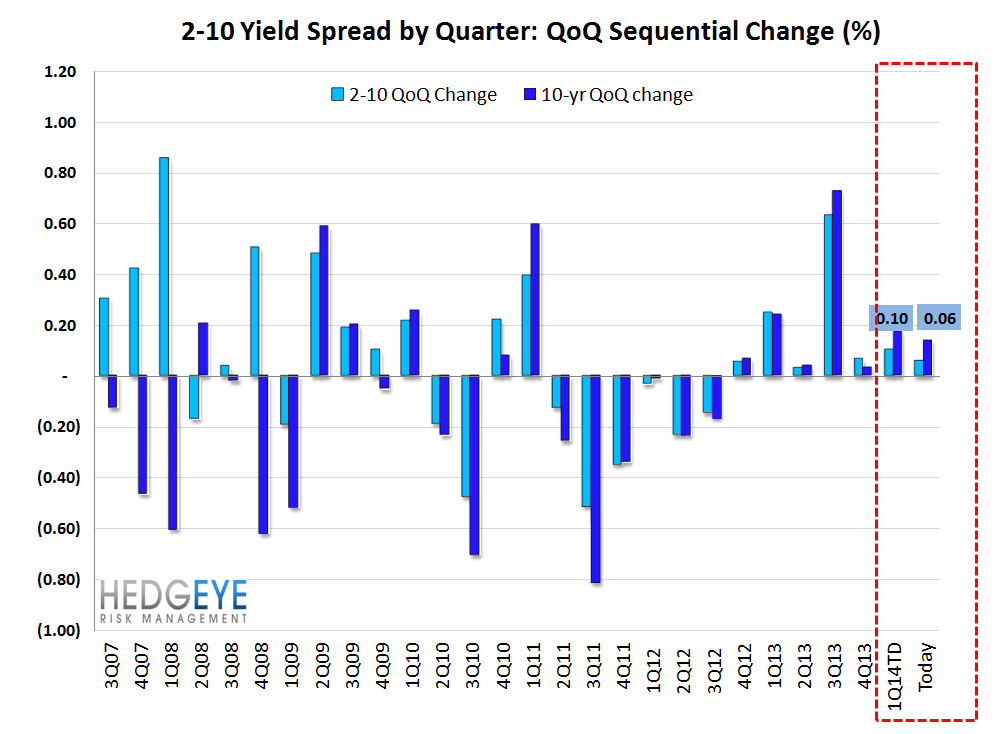

Yield Spreads

The 2-10 spread fell -2 basis points WoW to 247 bps. 1Q14TD, the 2-10 spread is averaging 251 bps, which is higher by 10 bps relative to 4Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT