“In theory, there is no difference between theory and practice. In practice there is.”

-Yogi Berra

I had a ton of feedback on yesterday’s Early Look (on how and why I use Twitter), so I wanted to thank you for that. Without having to answer to and consider your objective questions and thoughts, I’d just be a man in a room who is hostage to my own thinking. #scary

Your feedback generates more questions and ideas for our research team to work on. So I decided to take 6 minutes to walk through who scores as The 3 Most Overrated Economists in The World (for @HedgeyeTV video CLICK HERE ). I also crowd-sourced (on Twitter) who my followers thought were the most overrated. We came up with completely different answers.

Today, I’d like to throw that right back at you and add the follow-on question – who are The Most Underrated Economists (and/or strategists) that you follow? This has nothing to do with being mean or nice. This has everything to do with competence. We all need to find a better way. In theory, there are “experts” spewing on TV all day long. In practice, you (the players) know who gets it.

Back to the Global Macro Grind…

#Davos is a big deal. CNBC focused on Matt Damon’s "Save the World’s Water" thing yesterday and Reuters is all over actress Goldie Hawn this morning. Up next, after living large last night, Nouriel Roubini is Snapchatting the world a picture of him pecking Arianna Huffington on the cheek.

Great.

In other news, 2 of our Top 3 Global Macro Themes are trending in markets this morning, big time:

1. #InflationAccelerating

2. #GrowthDivergences

On Inflation, just to clarify:

- Our call here is like all the calls we make – rate of change – deflating the inflation (last year’s theme = #over)

- We aren’t purely focused on commodity deflation ending; but it’s a big part of the market expectations mismatch

- #InflationAccelerating is a bigger problem in the US than it is in Europe (that’s why we like European Equities more)

Got Commodity inflation in 2014 YTD?

- CRB Commodities Index (19 commodities) is beating both the Dow and the SP500 YTD (it’s up instead of down)

- CRB Food Index = +1.5% YTD (after food prices crashed last year from the 2012 all-time highs)

- YTD Food Inflations = Oats +12.9%, Cattle +5.1%, Coffee +3.9%

- Natural Gas at $4.76 (don’t tell Washington about heating your home) = +12.9% YTD

- Precious Metals YTD = Platinum +6.5%, Palladium +4.3%, Gold +3.7%

In stark contrast to what you would have seen in the Hedgeye Asset Allocation Model for the better part of the last year (0% allocation to Commodities), we have a 9% asset allocation to Commodities right now. From here, that’s going up, not down.

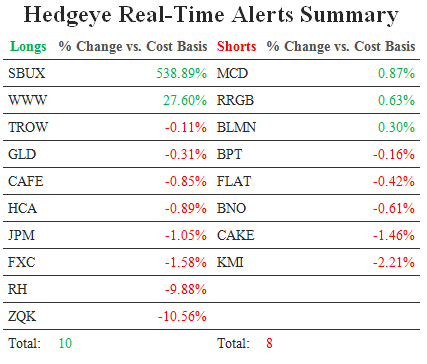

In Real-Time Alerts we are long of Gold in Gold terms (GLD) and Coffee via the CAFÉ (take the little chapeau off the French spellchecker and you’ll see the Coffee ETN – not a perfect security, so if you’re an Institutional investor, just buy the futures).

On the other side of this Q1 theme, there are plenty of short ideas to sink your teeth into; Restaurant Shorts in particular (Slowing Sales and Rising Food Costs). This is the highest # of short ideas our Food/Bev guru Howard Penney has had since 2008. He held a Best Short Ideas call last week @Hedgeye on Cheesecake Factory (CAKE). And he’ll write the Early Look for you tomorrow.

With Roubini going bullish, got short ideas? Here are some high-quality Food #InflationAccelerating ideas currently in Real-Time Alerts:

- Cheesecake (CAKE)

- Bloomin’ Brands (BLMN)

- Red Robin Gourmet Burgers (RRGB)

- McDonald’s (MCD)

In other words, 50% of my #timestamped short book is in Restaurant Shorts (10 LONGS, 8 SHORTS currently @Hedgeye after selling into yesterday’s all-time Russell2000 high of 1181).

In another @HedgeyeTV video this week titled Here’s What’s Working (for video CLICK HERE), I made a very simple point about our #GrowthDivergences theme (which syncs with #InflationAccelerating): country and sector picking matters as much as stock picking right now (i.e. pick the right sectors in the right countries and you’ll look like a good stock picker!).

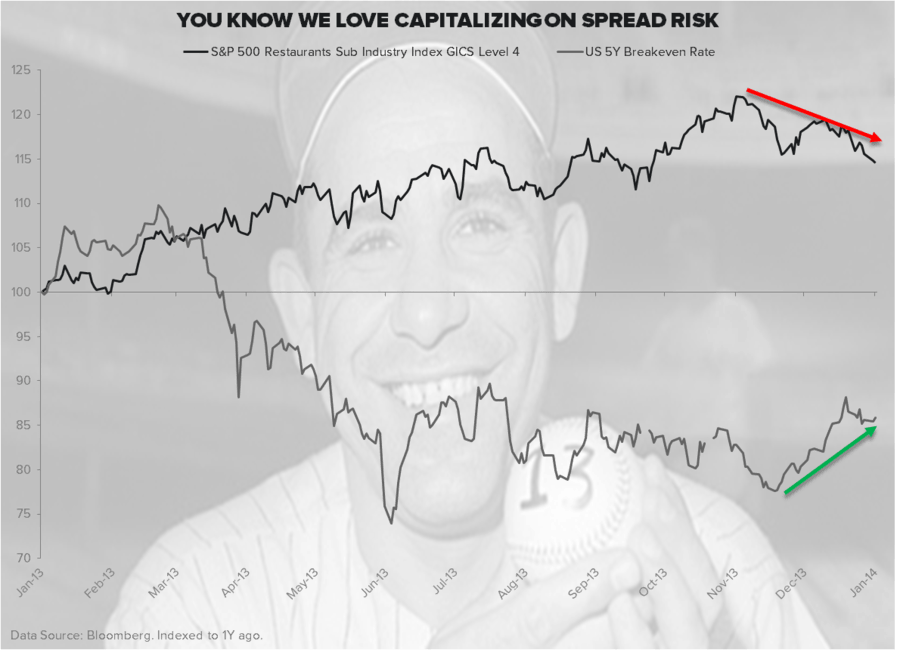

If you really want to boil that macro point down, for now you want to be:

A) Long Inflation Expectations assets (like breakevens)

B) Short US Consumption assets (like restaurants)

Since the European growth recovery is 1-2 years behind the US (and most of Asia, including Japan), that’s the other reason why we think you’re going to continue to see European Equities outperform the Global Equities league tables.

Remember, in theory consensus might think it’s about absolute levels of growth. In practice, it’s all about the rate of change of growth. And that’s all I have to say about that.

Our immediate-term Global Macro Risk Ranges are now:

SPX 1

Brent 105.87-108.75

NatGas 4.35-4.77

Gold 1

Copper 3.30-3.40

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer