Investment Company Institute Mutual Fund Data and ETF Money Flow:

Total equity mutual funds experienced strong inflows for the second week of 2014 with $8.2 billion flowing into all stock funds for the week ending January 15th, after a slight negative outflow last week to start the year. Within the total equity fund result, domestic equity mutual funds gained $4.2 billion, the biggest subscription in 10 weeks, with international equity funds posting a similar $4.0 billion inflow. This strong weekly inflow coupled with the slight outflow from last week has now moved the 2014 weekly average to a $3.9 billion average inflow for equities to start 2014, a follow through on 2013's positive trends where $3.0 billion per week on average flowed into stock funds.

Fixed income mutual funds had a slight inflow for the most recent 5 day period however the action was hardly robust. In the week ending January 15th, total fixed income mutual funds produced a $912 million inflow, which broke out into a $684 million inflow into taxable bonds and a $228 million inflow into tax-free bonds. This slight subscription into muni or tax-free bonds broke a streak of 33 consecutive weeks of outflow. The 2014 weekly average for fixed income mutual funds now stands at a $1.8 billion weekly inflow, an improvement from 2013's weekly average outflow of $1.5 billion. This improved 2014 weekly statistic however is still a far cry from the $5.8 billion weekly average inflow from 2012 (our view of the blow off top in the bond market).

ETFs experienced mixed trends during the week but essentially followed the direction of mutual funds with an inflow into passive equity funds and a slight outflow from bond ETFs. Stock ETFs gained a modest $421 million for the 5 day period ending January 15th with bond ETFs experiencing a slight $142 million outflow. The 2014 weekly averages considering this new production are now a $464 million outflow for equity ETFs and a $318 million inflow for fixed income ETFs.

The net of total equity mutual fund and ETF trends against total bond mutual fund and ETF flows totaled a positive $7.9 billion spread for the week ($8.7 billion of total equity inflows versus the $770 million inflow within fixed income; positive numbers imply inflows for stocks). The 52 week rolling average spread has been $7.3 billion (positive spread to equities), with a 52 week high of $30.9 billion (positive spread to equities) and a 52 week low of equity/debt weekly spread of -$9.2 billion (negative numbers imply a net inflow into bonds for the week).

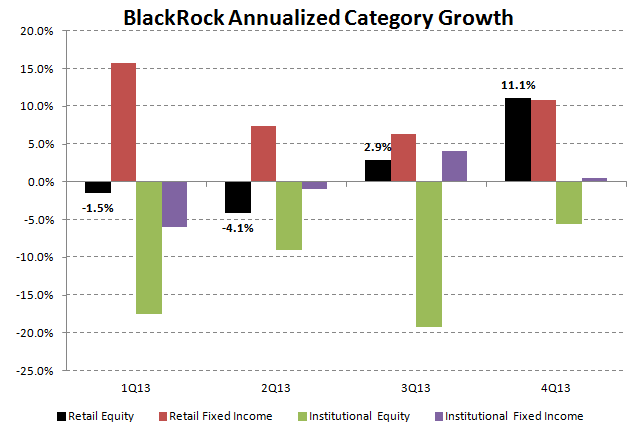

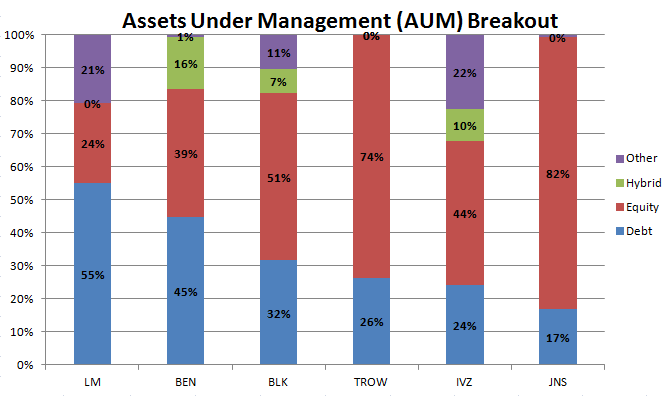

We relay that our ongoing call of a retail investor allocation into equities and out of fixed income started as of mid-year 2013 and is continuing. As crystallised in the recent BlackRock fourth quarter earnings report, BLK's category asset flows showed the strongest growth in retail equities with weaker comparative trends in fixed income. We think that the retail story relayed by BlackRock is a trend that can continue into 2014 as mutual fund flow driven by retail investors is a performance chasing exercise with still better return prospects in equities over fixed income. With this theme in mind, we continue to recommend T Rowe Price (TROW) on the long side with allocations of 82% of its assets-under-management in equities and 80% of the firm's AUM in retail. The separate story relayed from BlackRock is an institutional reallocation on the margin out of equities and into fixed income continues to be a function of two dynamics in our view. Firstly with the strong returns of 2013, a 60/40 institutional portfolio of stocks/bonds would have to shift by 6% in order to maintain that weighting (6% of the stock portfolio would have to be sold and reallocated into 6% more bonds which may explain the asset returns to start 2014). In addition, our recent pension fund survey highlighted that liability driven investing and "derisking" within the $16 trillion pension fund market are the highest priorities which generally decreases the demand for equities and increases the demand for bonds institutionally (see our report on this issue). This emerging trend on the institutional side of the market also benefits the Alternative asset managers who stand to get new market share from this reallocation.

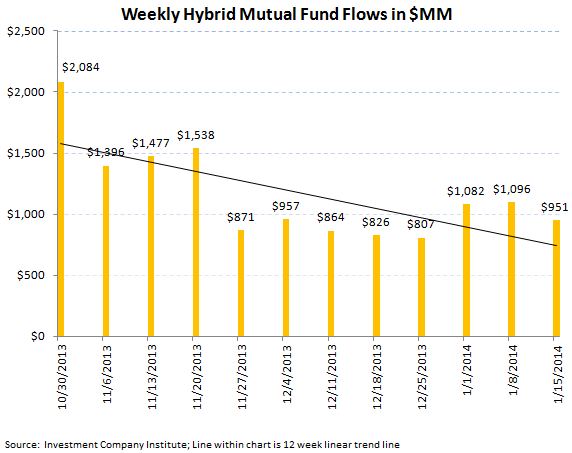

Most Recent 12 Week Flow in Millions by Mutual Fund Product:

Most Recent 12 Week Flow Within Equity and Fixed Income Exchange Traded Funds:

Net Results:

The net of total equity mutual fund and ETF trends against total bond mutual fund and ETF flows totaled a positive $7.9 billion spread for the week ($8.7 billion of total equity inflows versus the $770 million inflow within in fixed income; positive numbers imply inflows for stocks). The 52 week rolling average spread has been $7.3 billion (positive spread to equities), with a 52 week high of $30.9 billion (positive spread to equities) and a 52 week low of equity/debt weekly spread of -$9.2 billion (negative numbers imply a net inflow into bonds for the week).

Key Asset Management Thought:

We relay that our ongoing call of a retail investor allocation into equities and out of fixed income started as of mid-year 2013 and is continuing. As crystallised in the recent BlackRock fourth quarter earnings report, BLK's category asset flows showed the strongest growth in retail equities with weaker comparative trends in fixed income. We think that the retail story relayed by BlackRock is a trend that can continue into 2014 as mutual fund flow driven by retail investors is a performance chasing exercise with still better return prospects in equities over fixed income. With this theme in mind, we continue to recommend T Rowe Price (TROW) on the long side with allocations of 82% of its assets-under-management in equities and 80% of the firm's AUM in retail. The separate story relayed from BlackRock is an institutional reallocation on the margin out of equities and into fixed income continues to be a function of two dynamics in our view. Firstly with the strong returns of 2013, a 60/40 institutional portfolio of stocks/bonds would have to shift by 6% in order to maintain that weighting (6% of the stock portfolio would have to be sold and reallocated into 6% more bonds which may explain the asset returns to start 2014). In addition, our recent pension fund survey highlighted that liability driven investing and "derisking" within the $16 trillion pension fund market are the highest priorities which generally decreases the demand for equities and increases the demand for bonds institutionally (see our report on this issue). This emerging trend on the institutional side of the market also benefits the Alternative asset managers who stand to get new market share from this reallocation.

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA