In this note, we look at the largest companies by market cap in the Consumer Staples space from both a quantitative perspective and fundamental aspect where we offer one. As you will see over time, sometimes our fundamental view does not align with the quantitative setup (though not often).

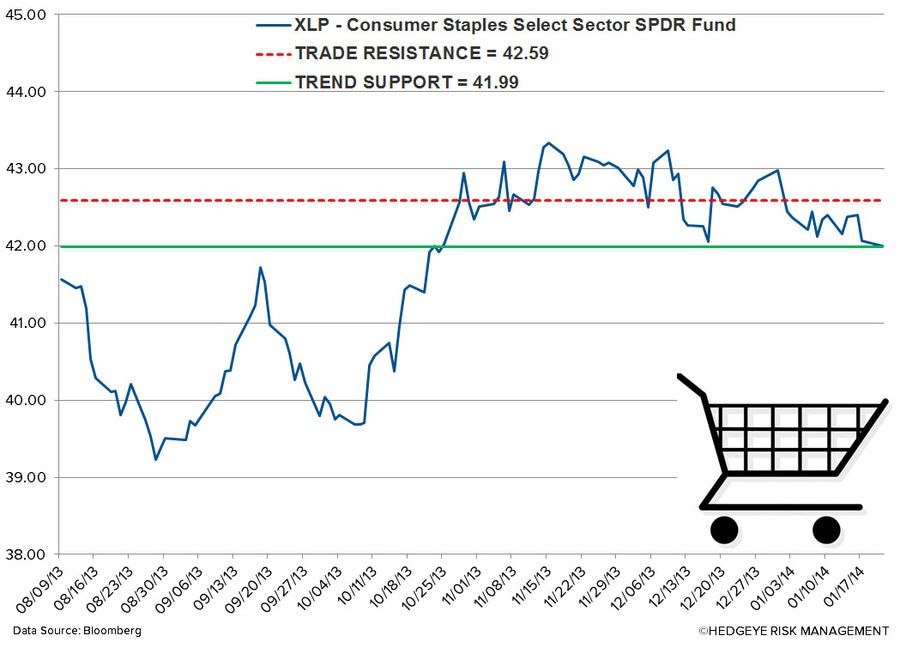

Consumer stocks are off to a tough start in 2014. From a quant setup Keith McCullough said over the weekend that “I’d short 80% of this market cap.” As you can see from the charts below, there is a bearish set up for the largest names in Consumer Staples.

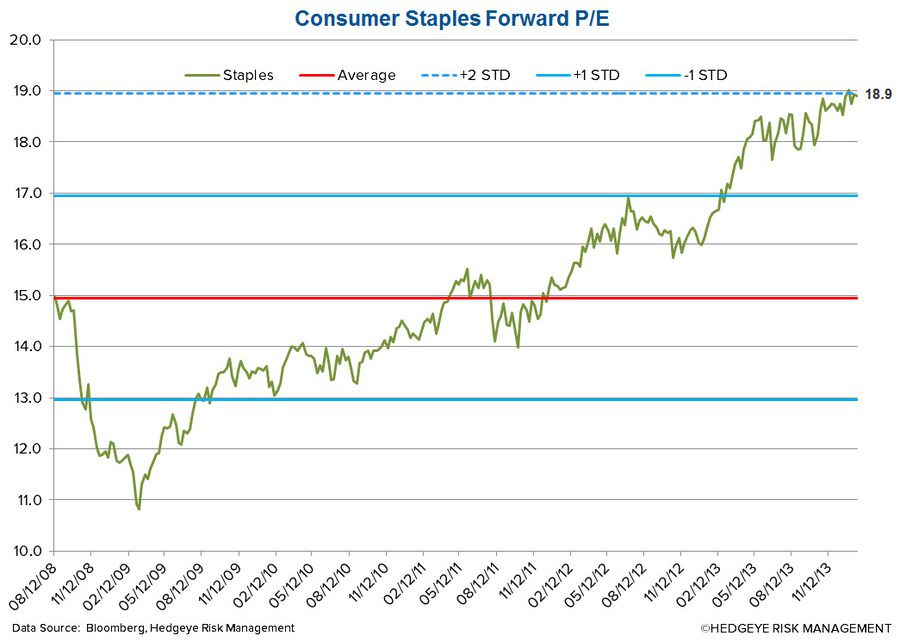

We generally believe that the group is way over-owned and loaded with premium valuations in a US consumption growth slowing world. To that end, the most recent data on Disposable income per capita is making new lows and the high frequency Bloomberg weekly consumer comfort index has not seen any real improvement over the past 6 months.

Uniliver started the current earnings season saying that “first-quarter underlying sales will rise at the low-end of 3 percent to 5 percent guidance.” The biggest issues for Uniliver is stemming from the slowdown in emerging markets, although according to the company Europe is showing few signs of improvement as consumers remain wary.

The sector received the spotlight this morning with news that Mondelez (MDLZ) appointed Nelson Peltz of Trian Partners to its board. Trian is the fourth largest shareholder of MDLZ (2.33%) and was very public in July 2013 issuing a white paper encouraging the company to merge with PepsiCo and spin off its beverage business. This announcement, which heightens animal spirits based on Peltz’s track record of restructuring companies to unlock shareholder value, follows the BEAM acquisition by Suntory last week and offer exciting merger winds from a group that otherwise has had a slow start to the new year.

We will be hearing from PG and KMB on Wednesday and next week begins the earnings deluge.

BULLISH

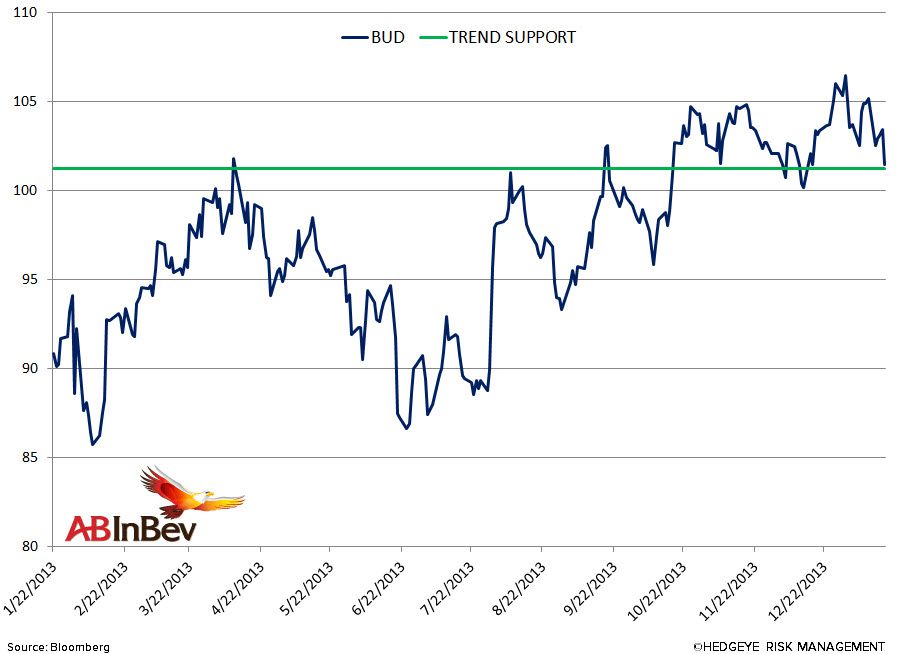

BUD – looks almost identical to DEO – big beta trade that’s starting to come undone for the group overall (XLP is bearish TRADE now, and that’s new); $101.24 is TREND support; above that bullish; below it bearish

DEO – after failing to breakout to higher-highs (vs the DEC 2013 closing highs), now the TREND line of $126 is under attack here and that is new (and bearish if it breaks)

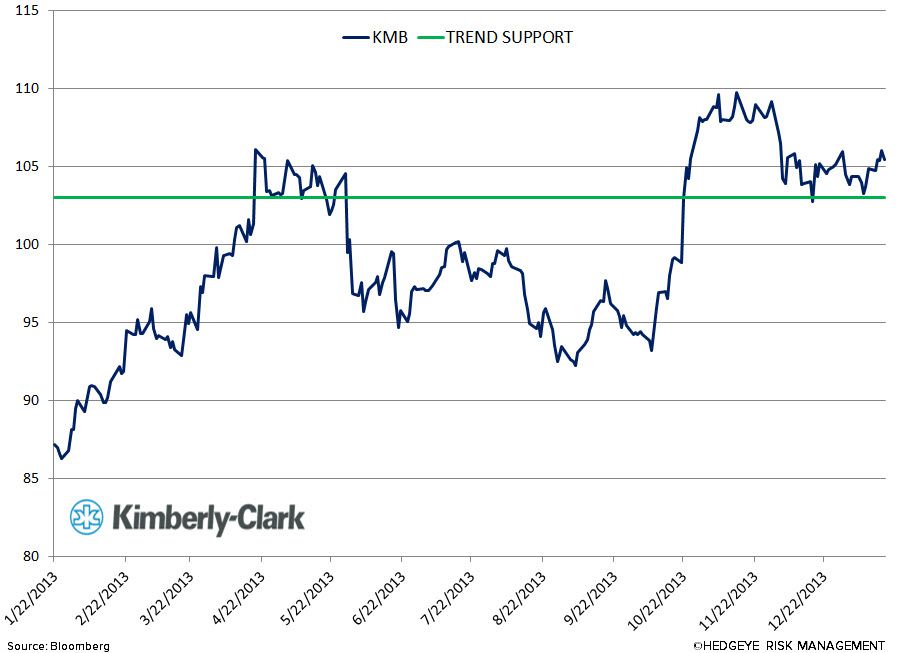

KMB – next to MDLZ its one of the few stocks on this list I’d buy if blindfolded w/ no research; part of that is that the stock was so bad that its in a classic @Hedgeye bearish to bullish reversal (might not last, but looks good as long as $103.02 TREND support holds)

MDLZ – best looking name on your roster; still in a Bullish Formation (bullish TRADE, TREND, and TAIL) with immediate-term TRADE support of 34.65 being the important line to use as a momentum stop

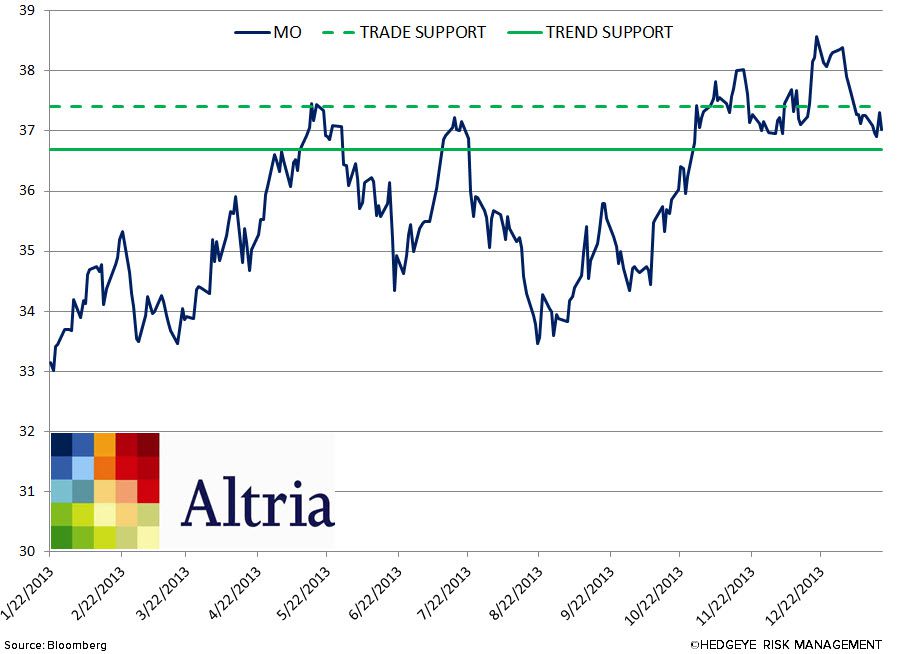

MO – doesn’t look nearly as bad as PM, so an interesting pair there, but that can change if MO’s TREND support breaks (36.69, so its close by); just broke its immediate-term TRADE line of 37.41 in 2014 too

BEARISH

GIS – if you told me to, I’d short this stock on the open tomorrow; brand new bearish TREND developing with $49.55 being TREND resistance

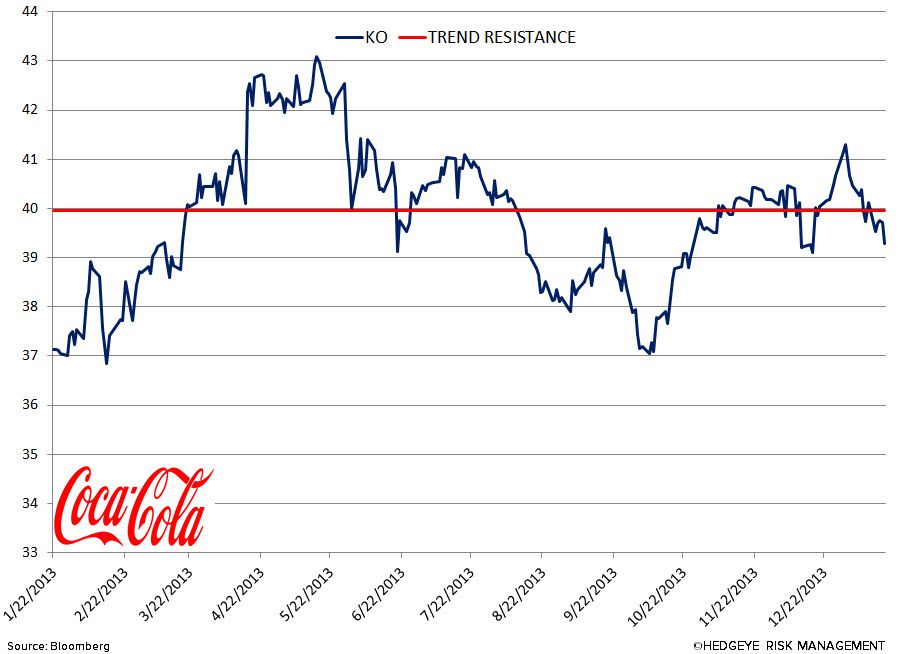

KO – just broke its TREND line too (that’s new), with TREND support of 39.96 now being resistance, if you have bearish catalysts, good chance this stock retests the OCT 2013 lows

PEP – doesn’t look as bad as KO, but pretty close – looks a lot like sector beta for XLP that just flagged bearish in the last few weeks; TREND line of $82.74 broke

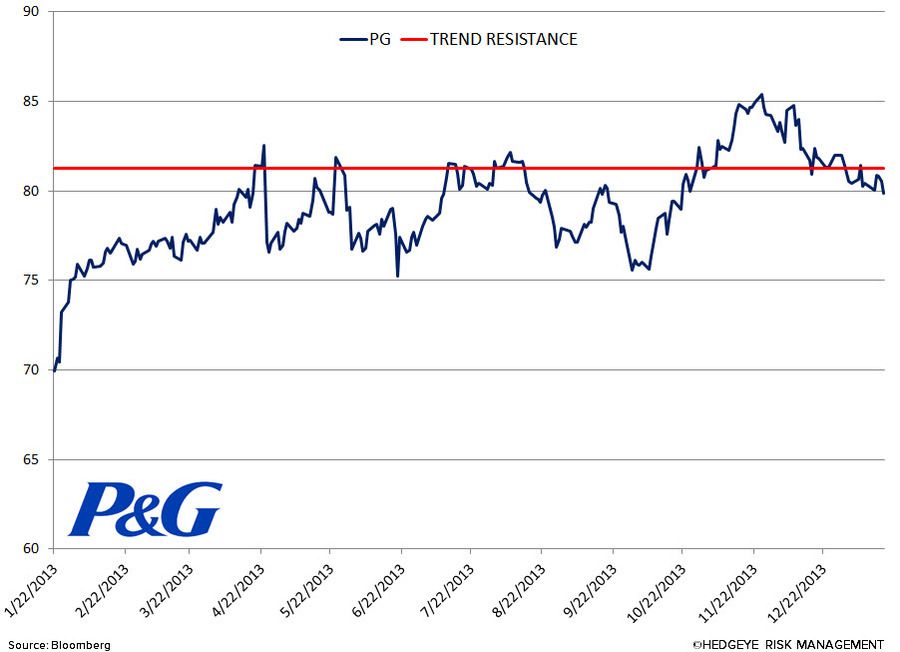

PG – looks like GIS; if you tell me to short this, I will. What was TREND support at 81.29 is now a freshly established wall of resistance; no support for this stock to $74-75

PM – continues to look horrible on both an absolute and relative basis. TAIL risk resistance remains in place overhead at 86.63; no support to the SEP 2013 closing lows.