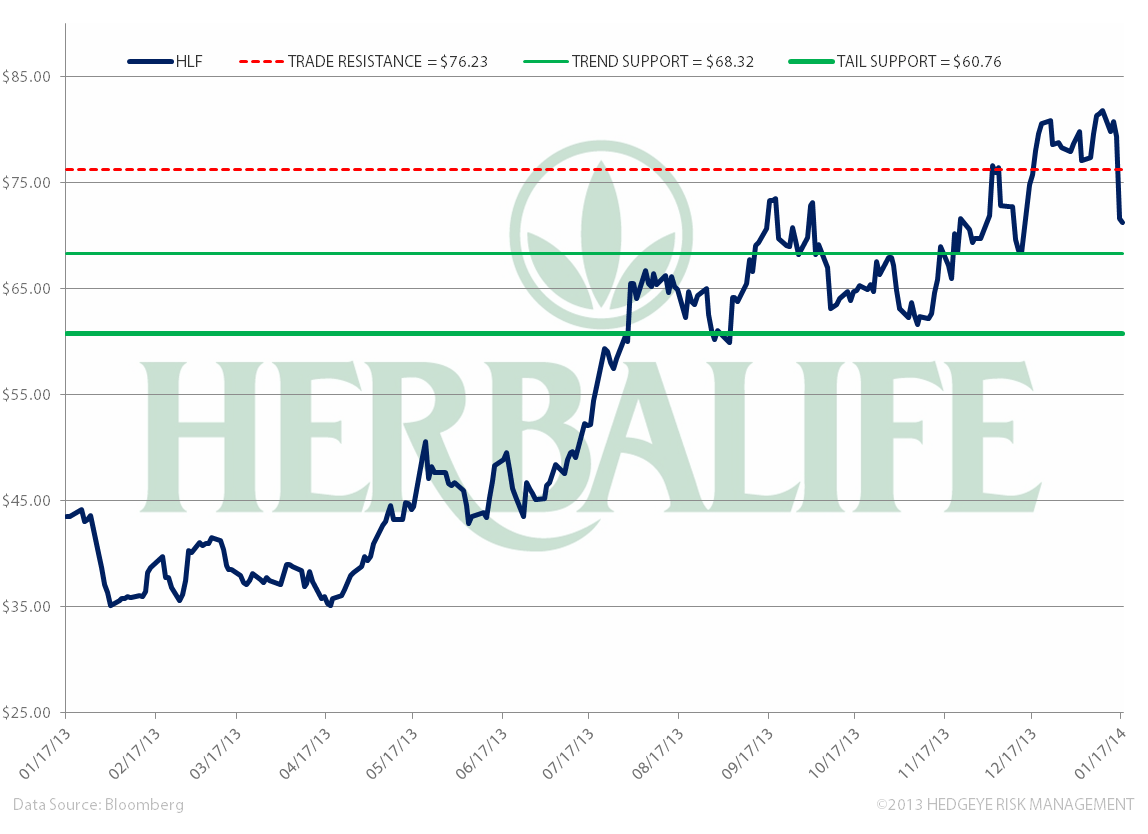

Take-away: We’re buying the dip in HLF as we think that the news about Chinese officials investigating Nu Skin is a separate issue from HLF, despite both businesses sharing risk on pyramid scheme claims.

What’s going on with NUS and HLF?

- Chinese regulators yesterday said they’d investigate accusations from The People’s Daily, the Communist Party’s main propaganda organ, which called Nu Skin, a skin-care and nutritional products company, a pyramid scheme.

- Nu Skin (NUS) is trading down -45% since 1/14 (looks like someone had some inside info ahead of the announcement). NUS earns ~ 31% of its revenues from mainland China.

- Herbalife (HLF) is getting hit on pass-through fears that it could be the next target of an investigation (either abroad and/or in the U.S.). HLF has ~ 11% net sales from China, according to Q3 2013 results.

- As background, the debate around the business practices of HLF took flight late in 2012 when Bill Ackman of Pershing Square Capital presented a 334 page PowerPoint at the Ira Sohn conference (on 12/20/2012) calling HLF a pyramid scheme, and announcing that his fund would take a short position in HLF with a $0 price target.

- Rival activists, including Carl Icahn and Dan Loeb (and others), were quick to take the other side of Ackman’s short bet.

- Since Ackman’s presentation the stock has soared as high as 212%. As of December 2013, Ackman has lost as much as $500M in the position.

- If you’re unaware of the intense animosity and scorn that these rival activists have for Ackman, see Vanity Fair’s April 2013 article The Big Short War.

Today we added HLF as a buy in our Real-Time Alerts

- Today, it was announced that Ackman plans to claim in a public presentation next month that HLF operates illegally in China.

- Yesterday’s Nu Skin news along with Ackman’s announcement today have sent HLF down -12% in the past two days.

- We view Ackman’s decision to claim HLF operates illegally in China as an effort to talk up his book.

- We think this position is supported by a number of factors:

- As we’ve stated before in our research, we do not know whether HLF is or is not a pyramid scheme. A Federal agency (SEC, FDA, FTC, or IRS) would have to make this determination (not a money manager) and we’ve yet to see any interest in an agency to open Pandora’s Box on the questionable business practices and accounting of multi-level-marketing companies.

- In his original presentation Ackman was unable to convince investors that HLF is a pyramid scheme (based on the stock’s move). He’s now trying to augment his claim, but now the target is China, a country steeped in opacity’s vine when it comes to transparency. Remember, Ackman wasn’t able to equivocally show how the pyramid scheme worked in the U.S., with the aid of geographic proximity and the ability to communicate in his mother tongue.

- We cannot underscore more how vehemently the rival activists want to bury Ackman on this position – even if they believe HLF is a pyramid scheme. We expect this rival camp to continue to drive the debate, and the stock.

- The company has also done all it can to insulate itself and protect the stock price, from hiring the high profile David Boies of the law firm Boies, Schiller & Flexner LLP to issuing aggressive stock buybacks and dividend raises.

- Finally, HLF has a lot less skin in the game in China compared to NUS, as we note above. While there’s the risk that a decision in one country can tumble weed into other regions, our investment approach with HLF is simply to take advantage of the stock that is oversold on fear.

Matthew Hedrick

Associate