THESIS SUMMARY

- EHTH Preannouncement Lays Out Best Case Scenario: Individual & Family plan (IFP) application metrics are inflated from a concentrated seasonality shift. Health Insurance demand now appears to be waning into January, suggesting the 170K in 4Q13 IFP applications may be peak the over the NTM. More importantly, it does not include existing plan cancellations.

- 2014 Consensus Estimates Appear Overly Ambitious: The headwinds to membership attrition are just as significant as the tailwinds to membership growth, and we expect Commission ARPU and EHTH’s Other revenue segment will remain challenged. We’re optimistically modeling 17% membership growth y/y (largely driven by Medicare and Ancillary), and revenue growth of 13% vs. consensus of 21%.

- Longer-term Outlook Remains Murky: Over time, more uninsured people are likely to seek plans as the individual mandate penalties increase over the next few years. However, improving website functionality on the government HIX and the employer mandate will be sources of increased competition and attrition risk.

- Sub $45 Stock?: EHTH's stock surged 20% on the 4Q13 preannoucement. After another brief surge, the stock is now trading at $55.92, which is 4.7x NTM Consensus Sales Estimates. We believe the stock could trade into the $44 range (22% downside) assuming multiple compression on 0.5x turns on our 2014 revenue estimate of $205 million. Stock could push higher near term, but we expect that will be short-lived

<chart11>

EHTH PREANNOUCEMENT LAYS OUT BEST-CASE SCENARIO

At face value, EHTH’s 4Q13 preannouncement appeared extremely bullish. Individual & Family Plan (IFP) applications increased 50% y/y (170K applications) vs. 7% growth YTD, while total Medicare product applications increased over 65% y/y. While encouraging, it also raises some red flags, particularly on the IFP side

The 50% increase is likely inflated since it measures the surge of ACA Open Enrollment against what is more seasonally-dispersed application volume for the company. Additionally, the deadline for Open Enrollment is at the end of 1Q14, so enrollment growth is likely to subside thereafter, if not decline on a y/y basis 2Q13-3Q13 if application volume has indeed been pulled forward. Our Google trackers suggest health insurance demand is already waning into 1Q14, so it’s highly possible that the 170K may be the peak in IFP applications over the NTM.

The bigger thing to consider is IFP cancellations/terminations, which generally represent the majority of all applications/membership growth. We estimate existing members represent over over 85% of all EHTH's reported IFP membership growth on a quarterly basis (1Q08-3Q13) . EHTH hasn’t provided any color on cancellations, but we suspect the cancellation rate may be higher than normal in 4Q13, which we will delve into below in more detail. In short, the surge in 4Q13 application growth may have been driven more by existing members than by new ones.

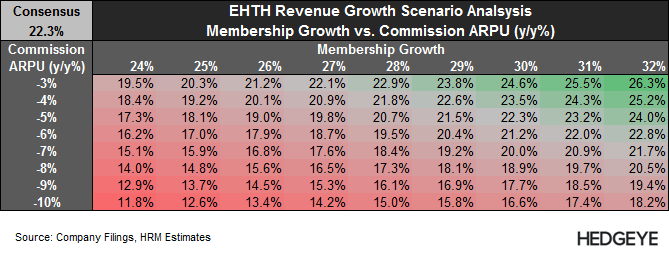

2014 CONSENSUS ESTIMATES APPEAR OVERLY AMBITIOUS

The headwinds to membership attrition are just as significant as the tailwinds to membership growth, and we expect Commission ARPU and EHTH’s Other revenue segment will remain challenged. We estimate that membership needs to grow 27%-32% y/y in order to hit consensus estimates (variance based our commission ARPU estimate range). We’re optimistically modeling 17% membership growth y/y (largely driven by Medicare and Ancillary), and revenue growth of 13% vs. consensus of 21%. In the table below, we're flexing EHTH's revenue growth by Memberhship and ARPU. In short, we believe EHTH is more likely to miss than beat 2014 consensus revenue estimates. Below we provide more detail.

Attrition Will Cap Upside: The street seems to be overly focused on the tailwinds to membership growth, but the headwinds to retention are just as significant. The three main headwinds to member retention are detailed below. In short, we suspect there may be more forces pulling existing EHTH members away from its platform than there are drawing new members in.

- Plan Terminations (ACA-Non Compliance): Starting in 2014, Individual and Family plans (IFP) must provide a certain set of Essential Health Benefits, while limiting a consumer’s out of pocket costs. The Obama Administration issued a temporary waiver on this rule for existing plans, but at both the Managed Care Organization’s (MCO) and state’s discretion. 16 states have chosen not allow the waiver, and we estimate that roughly 34% of IFP policy holders reside in those states. Not all of those plans are non-compliant, but a study from HealthPocket (EHTH competitor) suggests the overwhelming majority is (link). In fact, the Commonwealth Fund Affordable Care Act Tracking Survey (link) suggests that 22% of US IFP members received cancellation letters. We suspect this is one of the major reasons why EHTH’s 4Q13 applications accelerated so sharply.

- Newly-Eligible Medicaid Recipients: The 2014 Medicaid Expansion increases the income threshold to qualify for Medicaid to up to 138% of the FPL. Not all states have opted to expand Medicaid; in fact, we estimate that only 60% of the potential Medicaid expansion population resides in states that are expanding Medicaid. While the bulk of potentially-eligible Medicaid recipients do not have insurance, there is a sizable percentage that does; meaning that Medicaid expansion is actually a headwind to IFP retention. Using Census insurance data, we estimate that roughly 18% of IFP plans in the US are purchased by those with incomes below 138% of the FPL. We’re not suggesting that all these members will enroll in Medicaid, but the process to do so is now easier since the government HIXs help streamline the process if they are eligible. The recently released HHS January Enrollment Report (link) suggests 21% of applying members were determined eligible for Medicaid/CHIP. We suspect at least some percentage of those applicants was previously insured in the IFP market.

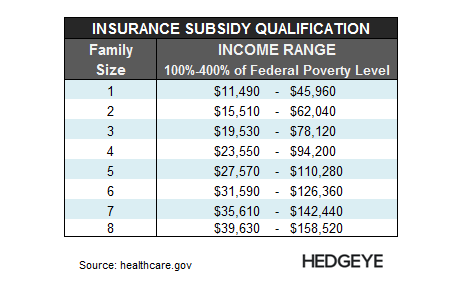

- Subsidy-Eligible Members: While CMS did grant EHTH permission to sell subsidized plans to members living in states run by FFEs, EHTH has stated that it hasn’t sold many plans to-date due to technical difficulties with interfacing with HHS.gov. More importantly, EHTH is not allowed to sell subsidized plans in any of the 14 states that are running their own HIX. So if any of EHTH’s existing members in those states wanted a subsidized plan, they were forced on to that state's HIX. We estimate that 34% of those currently insured in the US IFP market live in states running their own HIX. Regarding subsidy eligibility, we estimate that at least 40% of existing US IFP members may qualify for a subsidized plan on the HIX, but we suspect this is conservative since we are calculating subsidy qualification based on individual income. The threshold for family plans is considerably higher since it factors in household size. We estimate that family plans represent 50% of the US IFP market (31% couples/19% couples with children)

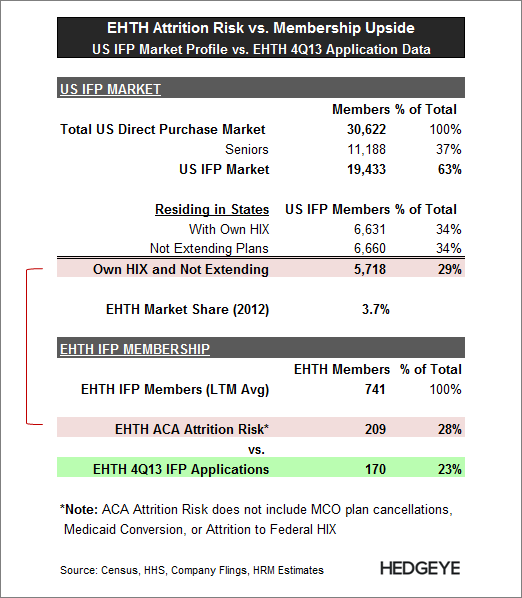

One final thought on membership attrition. There is considerable state overlap in all three of the above mentioned risks, which adds an extra level of vulnerability to EHTH member attrition. We estimate that 29% of the US IFP market lives in states that meet all three of the above criteria: Note that we haven’t discussed other attrition risks including forced plan termination by MCOs or potential attrition to the federal HIX. The Commonwealth Fund survey mentioned above suggests that roughly 20% of visitors to government HIXs already had insurance. A Mckinsey & Co survey suggests that as high as 89% of enrollees already had insurance (link). So while EHTH’s IFP applications have surged in 4Q13, member attrition has likely surged as well.

<chart7>

Commission Rates to Remain Under Pressure: There are a lot of moving parts to EHTH’s commission rates. Rates are generally higher in the first year of a plan and vary by the type of plan offered (IFP, Medicare, Ancillary).

MCOs are facing considerable legislative pressures in 2014 that are expected to increase overall costs and/or reduce premium reimbursement. We expect MCOs to push back on commission rates in 2014 as they did in 2011 with the introduction of the MLR mandate on IFP (Individual & Family plans). However EHTH has suggested that it is not expecting any material changes to commission rates in 2014. We’re approaching their outlook cautiously.

On the IFP side, we’re not sure exactly how IFP Commission ARPU will trend in 2014; there are too many moving parts in terms of plan mix. EHTH has suggested commission ARPU will be flat to slightly higher in 2014. However, it is making this assertion using a sampling of its plans against 2014 rate schedules from only 60% of its MCOs (in terms of commission revenue volumes). Additionally, it’s also basing this on current plan pricing, yet premiums have increased considerably for 2014.

On the Medicare side, EHTH states they are seeing “stable commission rates”. We’re not sure what that means exactly, but we know that Medicare reimbursement rates are going down in 2014, so unless those rates are increasing, Medicare commission ARPU will be on the decline.

But one thing is certain, as long as membership growth continues to favor considerably lower-priced Ancillary plans (Dental, Vision, Accident), with premiums that are at least 85% lower than IFP and Medicare Advantage Plans, commission ARPU will continue to decline.

LONGER-TERM OUTLOOK REMAINS MURKY

The uninsured population could be a major organic growth driver for the company. Over time, more of the uninsured population is likely to seek coverage as the individual mandate penalties increase over the next few years.

However, it’s equally as likely that functionality on the government exchanges improve over time as well. Since the bulk of the uninsured will qualify for subsidies (~70% earn less than 50K annually), EHTH will be at a competitive disadvantage vs. the government exchanges (particularly the state-based HIX). Additionally, there is only a one-year waiver on the employer mandate to provide health insurance coverage; meaning employees with existing Individual & Family plans (IFP) could get potentially cheaper coverage through their employer; serving as another source of potential attrition risk.

EHTH is planning on entering the Private HIX market, which is widely viewed as secular growth opportunity for the industry (we agree). However, this is still a nascent opportunity with more established competitors; there’s no telling how much EHTH can penetrate this market and/or how lucrative this opportunity will be.

SUB $45 STOCK?

EHTH's stock surged 20% on the 4Q13 preannoucement. After another brief surge, the stock is now trading at $55.92, which is 4.7x NTM Consensus Sales Estimates. We believe the stock could trade into the $44 range (21% downside) assuming P/S multiple compression of 0.5x turns on our 2014 revenue estimate of $201 million.

Management suggested at a recent sell-side meeting that 2014 guidance will include “caveats”, which we suspect means guidance will be issued in a wide range. If so, it could perpetuate the ACA growth narrative, potentially pushing the stock higher near-term. However, we expect the fog to clear by its 1Q13 earnings release after Open Enrollment ends and EHTH receives more monthly commission reports from its MCOs. By then, EHTH will have a better idea of how membership will trend in 2014.

Please let us know if you have any questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeHC2