Investment Company Institute Mutual Fund Data and ETF Money Flow:

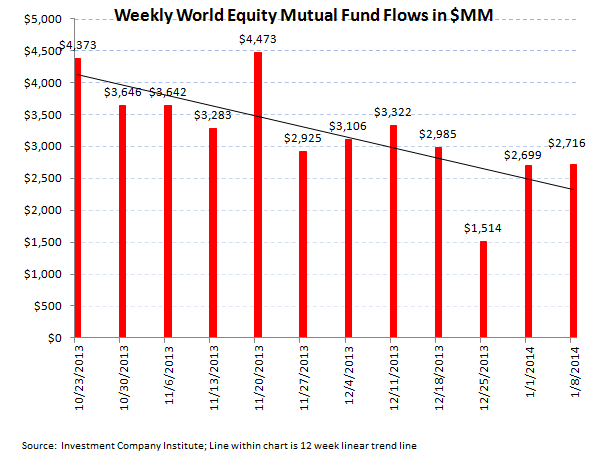

Total equity mutual funds experienced moderate outflows for the first week of 2014 with $646 million flowing out of stock funds for the week ending January 8th. Within the total equity fund result, domestic equity mutual funds lost $3.3 billion, the biggest outflow in a month, with international equity funds posting a $2.7 billion inflow. This weekly loss of $646 million now serves as the running 2014 average and compares to the solid equity inflows experienced in 2013 which put up a $3.0 billion inflow per week.

Fixed income mutual funds broke their dour stretch of 14 consecutive weeks of outflow with the first net subscription last week in three and a half months. In the week ending January 8th, total fixed income mutual funds produced a $2.6 billion inflow which broke out into a $2.9 billion inflow into taxable bonds and a $347 million outflow in tax-free bonds. This week's $2.6 billion inflow now serves as the 2014 weekly average which is an improvement for now against the 2013 weekly average in fixed income of a $1.5 billion outflow.

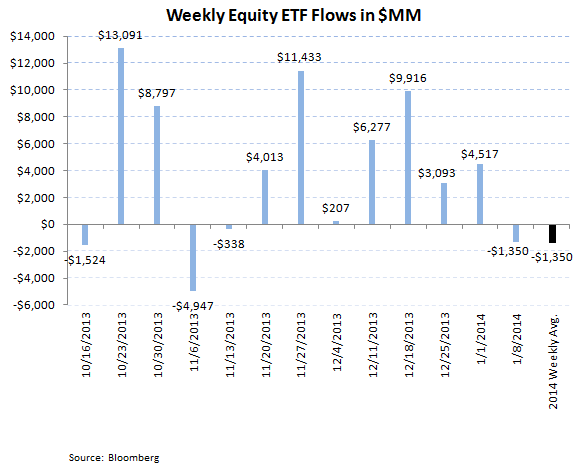

ETFs experienced mixed trends but essentially followed the direction of mutual funds with an outflow in passive equity funds and an inflow into bond ETFs. Stock ETFs lost $1.3 billion for the 5 day period ending January 8th with bond ETFs experiencing a $778 million inflow.

The net of total equity mutual fund and ETF trends against total bond mutual fund and ETF flows totaled a negative $5.4 billion spread for the week ($1.9 billion of total equity outflows versus $3.4 billion in fixed income inflows - negative numbers imply inflows for bonds). This result was the best week for total fixed income in 17 weeks and compared to the 52 week average of a $7.3 billion spread (positive spread to equities) but was well off of the 52 week high of $30.9 billion (positive spread to equities) and the smallest equity/debt weekly spread of -$9.2 billion (negative numbers imply a net inflow into bonds for the week).

We estimate that the strong return for stocks to end 2013 and the negative return for bonds to end last year may be resulting in an institutional re-balance to start 2014. In a hypothetical 60/40 portfolio of stocks/bonds, the returns in the broader averages of 30% in the S&P 500 and a negative 2% for the Barclay's Aggregate Index would mean an institutional portfolio would need to sell 6% of its stock holdings and buy 6% more in bonds, which may account for the year-to-date start in the asset classes (bonds outperforming stocks to start '14) with then mutual fund and ETF flows chasing this performance.

<chart11>

For the week ending January 8th, the Investment Company Institute reported moderate equity outflows from mutual funds with $646 million flowing out of total stock funds. The breakout between domestic and world stock funds separated to a $3.3 billion outflow from domestic stock funds and a $2.7 billion inflow into international or world stock funds. These results for the most recent 5 day period now serve as the year-to-date average for 2014 being they are the first week of the New Year and compare to the 2013 results of a $451 million average weekly inflow into domestic funds and a $2.6 weekly subscription into international or world funds for a total of a $3.0 billion weekly inflow average for last year.

On the fixed income side, bond funds broke their streak of 14 consecutive weeks of outflow for the 5 day period ended January 8th, with inflows into bond products for the first time in over 3 months. The aggregate of taxable and tax-free bond funds booked a $2.6 billion inflow, the first net weekly inflow since the $1.7 billion that came into bond fund the week ending September 25th. Taxable bonds carried the load with a $2.9 billion inflow, which was net against another outflow in municipal or tax-free bonds of $347 million. Intermediate term trends in fixed income are still negative with taxable bonds having had outflows in 27 of the past 33 weeks and municipal bonds having had 33 consecutive weeks of outflow.

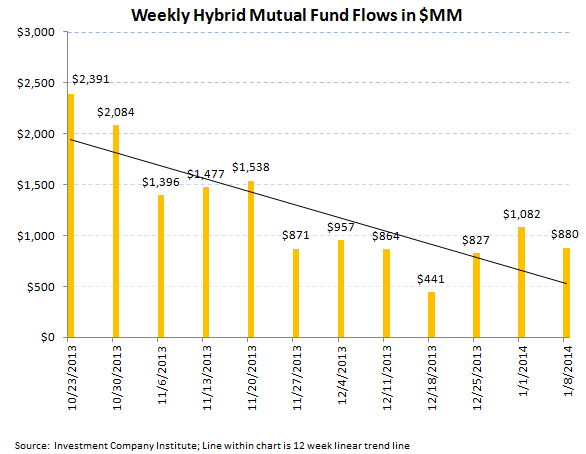

Hybrid mutual funds, products which combine both equity and fixed income allocations, continue to be the most stable category within the ICI survey with another $880 million inflow in the most recent 5 day period, although the past 6 weeks have been below the recent 52 week average for 2013 of $1.5 billion per week. Hybrid funds have had inflow in 31 of the past 33 weeks.

Passive Products:

Exchange traded funds had mixed trends within the same 5 day period ending January 8th but essentially followed the asset allocation flows within mutual funds last week. Equity ETFs posted a weak $1.3 billion outflow in the most recent 5 day period, breaking a streak of 7 consecutive weeks of positive equity ETF flow. The 2014 weekly average for stock ETFs is now this recent $1.5 billion outflow, which compares to last year's $3.4 billion weekly average inflow.

Bond ETFs experienced moderate inflows for the 5 day period ending January 8th with a $778 million subscription, an improvement from the week prior which lost $224 million and now also an improvement from the new annual comparison of a $234 million weekly inflow for 2013. Bond ETF trends have been perfectly mixed over the past 10 weeks, with 5 weeks of inflow and 5 weeks of outflow.

Net Results:

The net of total equity mutual fund and ETF trends against total bond mutual fund and ETF flows totaled a negative $5.4 billion spread for the week which favors fixed income ($1.9 billion of total equity outflows versus $3.4 billion in fixed income inflows - negative numbers imply inflows for bonds). This result was the best week for fixed income in 17 weeks and compared to the 52 week moving average of a $7.3 billion spread (positive spread to equities) but was well off of the 52 week high of $30.9 billion (positive spread to equities) and the smallest equity/debt weekly spread of -$9.2 billion (negative numbers imply a net inflow into bonds for the week).

We estimate that the strong return for stocks to end 2013 and the negative return for bonds to end last year may be resulting in an institutional re-balance to start 2014. In a hypothetical 60/40 portfolio of stocks/bonds, the returns of the broader averages of 30% in the S&P 500 and a negative 2% for the Barclay's Aggregate Index would mean an institutional portfolio would need to sell 6% of its stock holdings and buy 6% more in bonds which may account for the year-to-date start in the asset classes (bonds outperforming stocks to start '14) with then mutual fund and ETF flows chasing this performance.

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA