The year has kicked off with big news this week that Suntory is buying BEAM for $16B. Not to mention Constellation Brands (STZ) up on a rope – already +15% YTD on strong earnings results.

We would like to take a moment to briefly reiterate that we are sticking with two of our highest conviction Consumer Staples investment ideas from last quarter (originally published on 11/29/13).

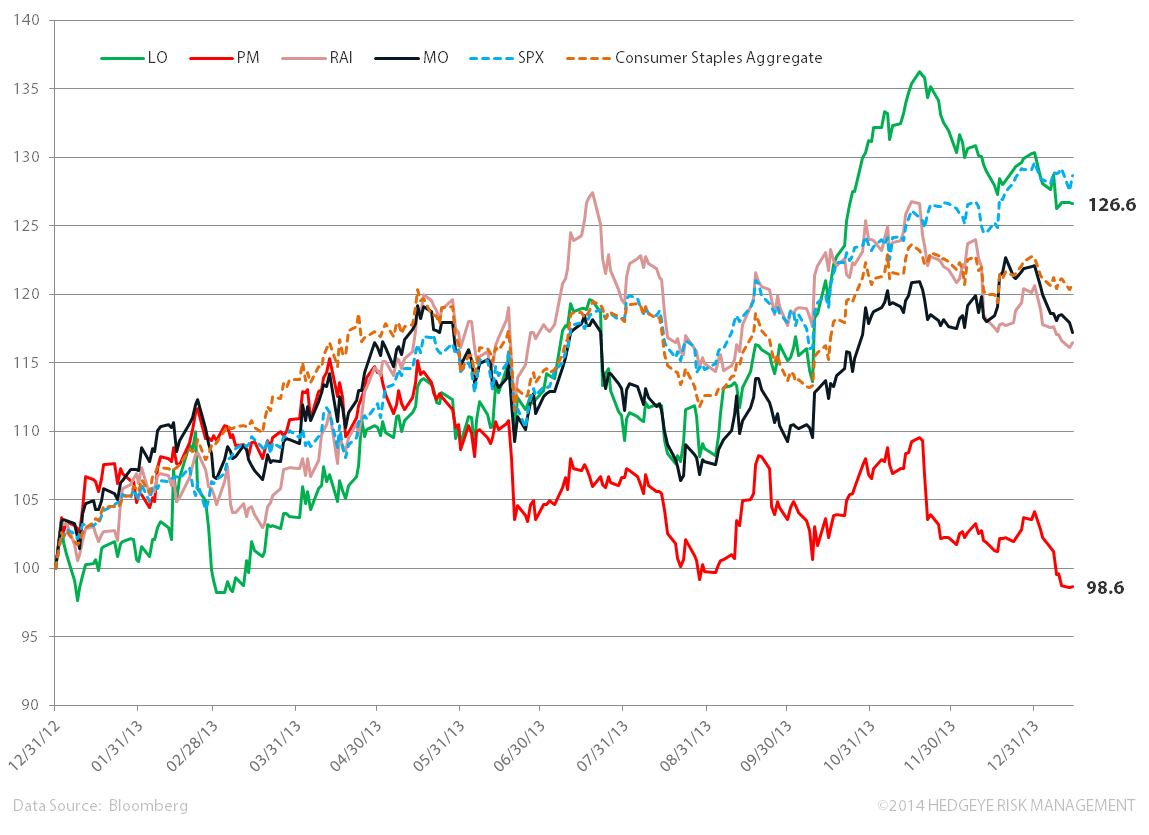

Long Lorillard (LO) and Short Philip Morris (PM).

From a sector perspective and based on our quantitative levels, Consumer Staples is trading bearish TRADE and bullish TREND. This implies a favorable outlook over the intermediate term, based on the current price level. XLP was up 23% in 2013, and as the chart shows, has traded largely sideways over much of the past 2 months.

We think valuation is still stretched for the group at 18.9x, or 2 standard deviations above the 5 year historical average. But we remain committed to bringing you alpha-generating investment ideas on the long and short sides this year.

Lorillard (LO) – we are staying long with the dominant player in menthol. The stock was up 32% last year and its FY 2014 P/E of 13.8x trades at a slight discount to its peers average of 14.3x. We believe its advantaged portfolio and growth strategy should continue to drive the stock higher this quarter.

Some key points:

- Outperformance based on an advantaged cigarette portfolio and leading share in the e-cig category.

- Continued strong demand for its full-flavored offerings and dominant share of menthol (~85% of its portfolio). Both are contributing to volume outperformance versus the industry (in the last quarter LO’s vol. +3.5% versus industry’s avg. -4%).

- Growth in menthol supported by positive demographic shifts to the menthol category:

- According to 2012 data from the National Survey on Drug Use and Health (NSDUH), over the last decade, the number of adult African-American menthol smokers has increased at a 2% CAGR, and at a 7% CAGR for Hispanics. As of 2012, this equates to 84% of African-American smokers smoke menthol; the figure for primary menthol smokers among Hispanics is 47%.

- Over the last decade, the adult African-American smoking population has increased at a 0.4% CAGR, whereas the adult Hispanic smoking population has increased at a 0.3% CAGR. We expect these trends to continue which should support the outperformance of LO’s menthol portfolio.

- We’re bullish on Lorillard’s rollout of “Newport Gold” – a non-menthol compliment to “Red.”

- We expect the FDA to punt on banning menthol cigarettes over the intermediate term given the lack of definitive and recognized studies that menthol is more harmful than non-menthol cigarettes. We also believe that the EU Parliament’s decision to ban menthol does not provide a useful guide to FDA policy given the sheer market size difference (Menthol = 31% of the U.S. cigarette market vs. 1-2% in Europe).

- E-cigs: Lorillard was the first Big Tobacco company to market with the acquisition of “Blu” branded e-cigs in April 2012 for $135MM.

- Despite only representing 4.9% of the portfolio, in Q3 Blu saw strong sales growth of 11% quarter-over-quarter (+350% year-over-year) to $63MM.

- LO CEO Murray Kessler’s e-cig strategy appears to forgo short-term profits for long term gains: he sold e-cigs at break-even in the quarter and was able to boost Blu’s market share to 49% from 40% in the previous quarter. We expect similar trends as LO attempts to capture brand loyalty. Over time, we do think that e-cigs can be margin-enhancing to the combined cigarette category.

- The company became an international e-cig dealer through its purchase of UK-based SKYCIG in October 2013 for £30MM in cash, plus an additional £30MM to be paid in 2016 based on the achievement of certain financial benchmarks.

- SKYCIG is a three year old company with ~ 300,000 users in the UK (there exists around ~ 10MM smokers in the country) that also happens to have nearly identical branding to Blu.

- LO is comfortably trading above our intermediate term quantitative TREND level of support of $48.12.

Philip Morris (PM) – The company continues to be plagued by a series of material headwinds.

To wit: a weak macro environment, challenging FX, excise tax hikes, and volume declines in key geographies. These ought to challenge earnings while the top line is running against a more difficult comp in Q4 and Q1.

Some key points:

- FX: in NOV 2013 the company updated its guidance which reflected a $0.40 2014 EPS FX headwind -- we think this estimate undershoots the weakness in its basket of currencies, in particular those of the emerging market. As an example, over the past 3 month against the USD the Indonesian Rupiah is down -10.8%, the Turkish Lira is down -10.1% and the Yen is down -6.6%!

- Volume: we expect volume to be impacted by a combination of continued weakness in the macro of core geographies (including the EU that the company expects to be down -7% to -8% in 2014) and an increase in excise taxes in key profit centers. France has been a negative outlier and we continue to believe that the tax policy of President Francois Hollande will impair consumer confidence. We expect Philip Morris has taken much of its pricing and will struggle to stem volume declines.

- Excise tax: into year-end Turkey announced a tax increase that should equate to hike in retail prices of 6-9%. This in on top of recent hikes in key geographies like Russia (volume impact est. -9% to -11%) and the Philippines (volume impact could be larger than Russia), which should also encourage an uptick in illicit trade.

- Push to Non-Combustible: we applaud the company’s push in Q4 2013 to accelerate its offerings of non-combustible harm-reduction products, however the initiatives come at a hefty price that we believe will influence the stock on downside over the near-term:

- The company announced plans in late NOV to accelerate the launch of a non-combustible harm-reduction product to mid-2014 versus previous guidance of 2016/7 at an incremental price tag of $100MM (note: it’s unclear on the form of this product – but suggestive of a category under the e-cig umbrella)

- In December the company announced that it is acquiring a 20% interest in Russian Megapolis Group for $750M. Longer-term, we believe this is positive for the company (Russia is the world’s second largest market behind China and Megapolis handles 70% of Russia’s cigarette volumes through its distribution agreements).

- The company announced in late DEC a strategic partnership with Altria (MO) in which MO will make its e-cigs (currently under the MarkTen brand in the U.S.) exclusively available to PM for sale outside the U.S. Conversely, PM will make available two of its harm-reduction products exclusively available to MO for sale in the U.S. We see this as a win for both parties, especially for MO given PM’s geographic sales stretch and to catch up to LO’s e-cig lead in the U.S. market.

- The company announced last Friday that it will invest up to €500MM in a reduced-risk product manufacturing facility in Italy, to be operation in 2016 with capacity of 30B units.

- Taken together, we see 2014 setting up to be a year of investment and 1H results to drag in concert with this investment and the continuation of broader headwinds of FX, excise hikes, and a challenged macro, alongside more difficult top line comparisons for Q4 and Q1.

- Quantitatively, PM is trading below our intermediate term TREND line of resistance, implying a bearish intermediate term set-up from its current price level.

Matthew Hedrick

Associate