To kick off Q3, the US Dollar was already weak... post the open we've had a few dampeners hit the tape that have exacerbated today's US Dollar weakness:

- China asked to discuss a "new global reserve currency" at the G8 (in Italy)

- Fed President Evans (Chicago) made a comment about the Fed's discussion about an "exit strategy" not involving a timeline

On the first point, we've been saying this all week and I'll say it again - the Chinese are selling US Treasuries, period. They aren't going to give the USA a real time memo while they are doing it either. Chinese Central Bank Chief Zhou's comments earlier in the week were misinterpreted by the manic media. He said there would be "no sudden change" to policy. No rational investor signals to the world that they are acting "suddenly" with their largest position. To be clear, the Chinese have stopped buying US Treasuries and are selling, gradually - not "suddenly".

On the second point, the Fed's credibility on inflation forecasting is negative. They missed the meltup in 2008 commodity inflation, and now they're hoping they don't see its birth as a result of the most politicized credit creation in the history of America. Hope is not a long term investment process. See my note earlier today titled "Reflation morphing into inflation" for the most current data point we have US Dollar based prices paid.

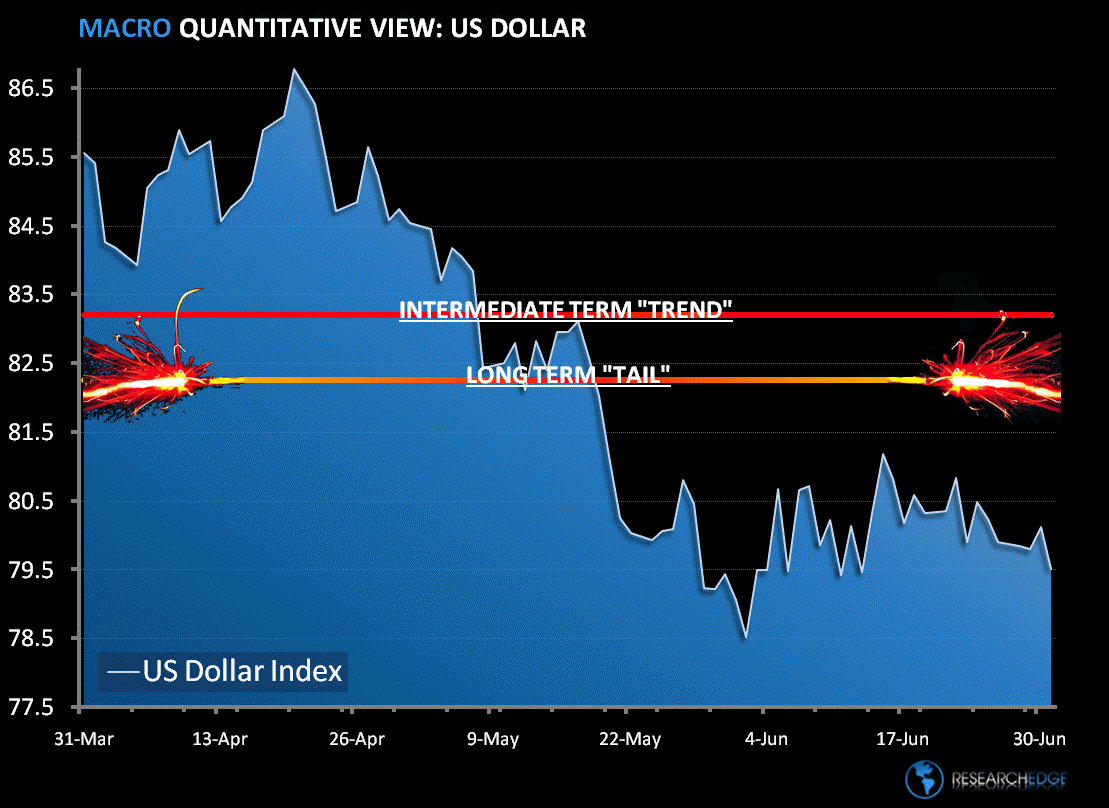

Finally, and most importantly, there's the marked-to-market price reality of the US Dollar (charted below). The red line with fuses burning is our government Burning The Buck. Long term TAIL resistance is now at $82.26 on the US Dollar Index, and as the USD trades below that line, we're going to be importing real inflation starting in Q4.

If you want a solution to this currency crisis, raise rates from these ridiculously low "emergency" rates that are currently compromising America's credibility.

KM

Keith R. McCullough

Chief Executive Officer