This note was originally published January 14, 2014 at 11:25 in Healthcare

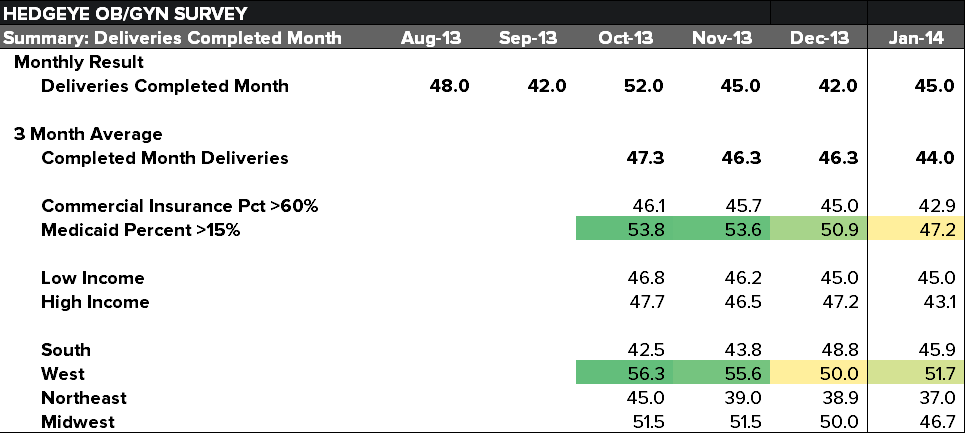

SELLING MD: After a 21% return ,we're closing our long position in MD. We've been running a survey of OB/GYNs for several months. The survey asks specifically about deliveries and pregnancy in the prior month and the outlook for the current month, and both are weak in Q413. Delivery trends registered a reading of 45.0 in the most recent completed month and 44.0 for the trailing 3 months. A reading below 50 suggests contraction.

TOUGHEST COMPARE IN 6 YEARS: Birth comparisons are the toughest they've been in 6 years in Q413, with Q412 registering +1.6% growth. As a result, and because maternity (still) drives same store results, we believe same store volume will be down substantially more than guidance of "essentially flat" for Q413.

PARITY & DEALS: While the catalysts of pricing parity and acquisitions remain, our current view is that weaker sequential same store volume will offset any positive updates on deals or parity payments. As a reminder, MD missed their 2013 deal guidance, but calmed concerns by filing a universal shelf implying bigger deals in the future. Since then, only 1 deal has been announced and was too small to require financial disclosures.

SENTIMENT: From a factor perspective, the decline in the short interest has largely played out and is clearly no longer the positive catalyst it had been. Additionally, sellside ratings continue to fall, and based on history, does not set up well for forward returns either.

Editor's note: This was written by Tom Tobin, Healthcare Sector Head at Hedgeye Risk Management. Click here to learn more about becoming a Hedgeye subscriber.