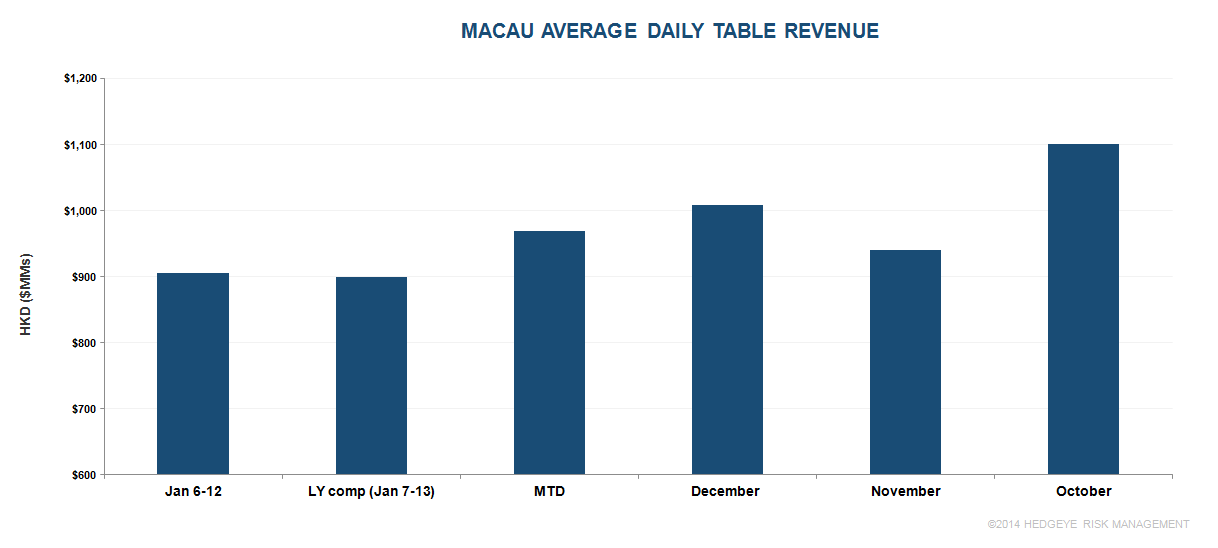

Before we get to the projections, we would like to point out one strange anomaly: the first 13 days of last year January produced exactly the same table revenue as the first 12 days as this year – HK$11,625 million. We’ve seen the Macau government use placeholders before so we would caution investors that this week’s numbers may not be reliable. Typically, placeholder weeks are followed by the volatility one would expect from a catch up month.

Assuming the numbers are real, average daily table revenues grew 1% above the comparable period last year and are up over 8% YTD. We are reducing our full month estimate from 22-28% YoY growth to 19-25% as a result of the softer week and expectation that virtually all of the incremental gaming revenue from the Chinese New Year celebration will occur in February. Our estimates for January and February growth remain above the Street consensus.

Anecdotally, we’re hearing that VIP volumes remain high, VIP hold may be a little low, and Mass traffic has slowed from week one to week two.

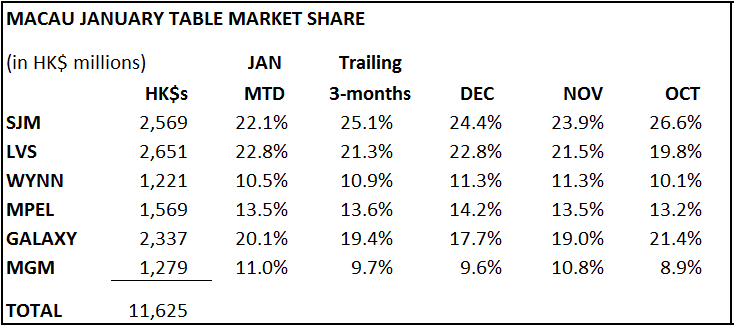

In terms of market shares, SJM is the big loser while LVS the winner this past week. Month to date, MGM has moderated but still remains above trend as does LVS and Galaxy.