TODAY’S S&P 500 SET-UP – January 13, 2014

As we look at today's setup for the S&P 500, the range is 25 points or 0.94% downside to 1825 and 0.41% upside to 1850.

SECTOR PERFORMANCE

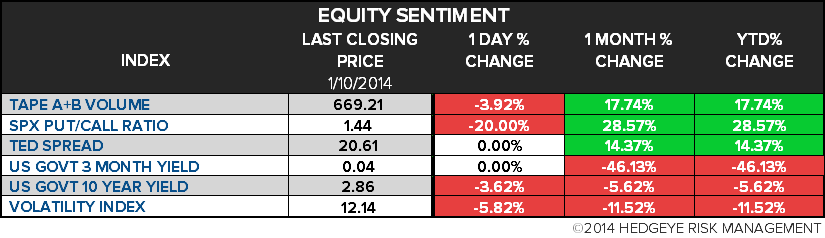

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.49 from 2.49

- VIX closed at 12.14 1 day percent change of -5.82%

MACRO DATA POINTS (Bloomberg Estimates):

- 11am: Fed to purchase $1b-$1.25b TIPS in 2018-2043 sector

- 11:30am: U.S. to sell $28b 3M bills, $26b 6M bills

- 12:40pm: Fed’s Lockhart speaks in Atlanta

- 2pm: Monthly Budget Statement, Dec. est. +$44b (pr -$135.2b)

GOVERNMENT:

- House, Senate in session

- Senate resumes consideration of unemployment insurance extension, 2pm

- Supreme Court hears arguments on whether President’s recess-appointment power may be exercised during recess that occurs within session of Senate, 10am

- Secretary of State John Kerry, Russian Foreign Minister Sergei Lavrov meet in Paris to discuss Iran’s participation in Syrian peace talks to take place Jan 22

WHAT TO WATCH:

- Fed said to probe banks over roles in forex fixing

- Amec agrees to buy Foster Wheeler for $3.2b in cash, stock

- Target’s delay in revealing breach was necessary, CEO tells CNBC

- Basel Committee makes concessions to banks on debt-limit rules

- Honeywell probed by U.S. on F-35 fighter part made in China

- UBS isn’t considering investment-bank spinoff

- Sanofi pays Alnylam $700m to add rare disease drugs

- Discovery Communications, Scripps end merger talks: WSJ

- U.S. automobile industry growth is leveling off, Toyota says

- BlackRock’s Bolton faces Italy proceeding over Saipem trade

- North American International Auto Show begins in Detroit

- JPMorgan health-care conference begins; THOR, THC present

- ICR XChange retail, consumer conference begins in Fla.

- Alcatel said to hold talks with Unify on enterprise unit sale

- Court in EnPro case sets liability obligation amt at $125m

EARNINGS:

- Limoneira (LMNR) 7am, $0.08

- Xyratex (XRTX) 8am, $0.12

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Indonesia Bans Ore Exports in Compromise Push for Metal Smelting

- China Said to Weigh Higher Food Imports in Security Shift

- Bullish Bets Fell Most in Seven Weeks Before Slump: Commodities

- Nickel Touches a Two-Week High as Indonesia Bars Ore Exports

- WTI Declines After Weekly Loss; Iran Nuclear Deal to Take Effect

- Sugar Extend Gains After Speculators Boost Bearish Bets by 19%

- Gold Trades Near One-Month High as Investors Weigh Fed Stimulus

- Corn Weekly Reversal Signals Rebound to Highest Since September

- Rebar Falls as Steelmaker Shagang Cuts Prices on Weaker Demand

- Philippines Sees Nickel Boon on Indonesia’s Ban: Southeast Asia

- Iran Oil-Export Capacity Falls 5.4% in Tanker-Tracking Signals

- American Cold Snap May Force EU Heating Oil Imports: Bear Case

- Hedge Fund Bullish Oil Wagers Drop as Fuel Supply Gains: Energy

- Wheat Rises as Egypt Purchase Indicates Demand for U.S. Supplies

CURRENCIES

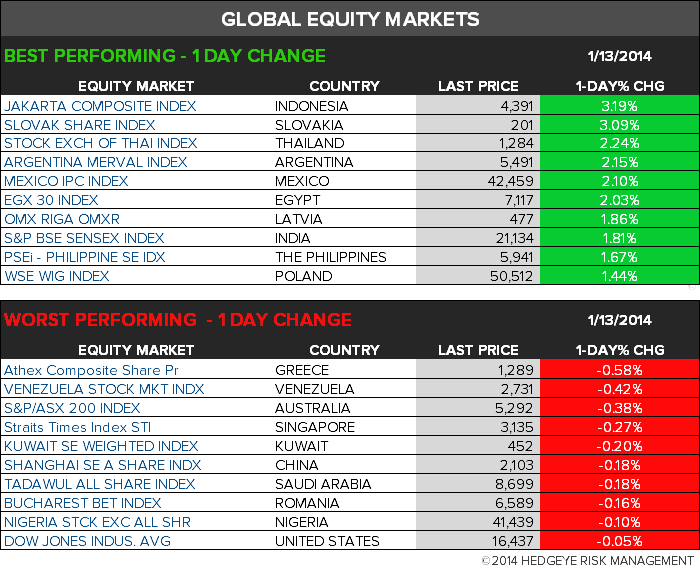

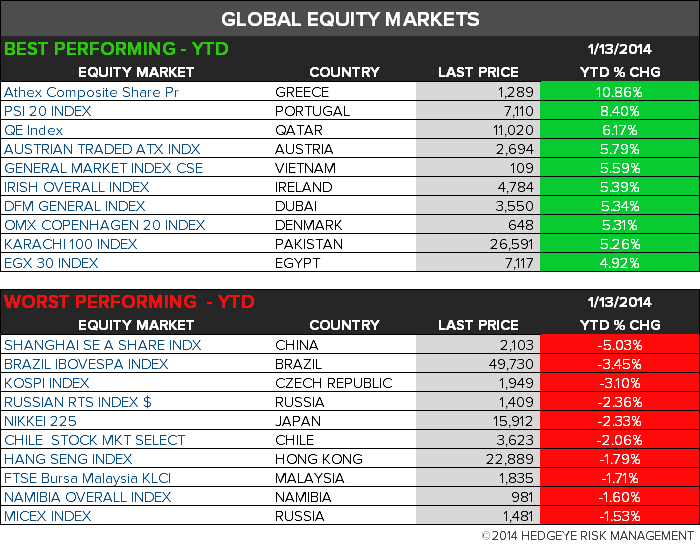

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team