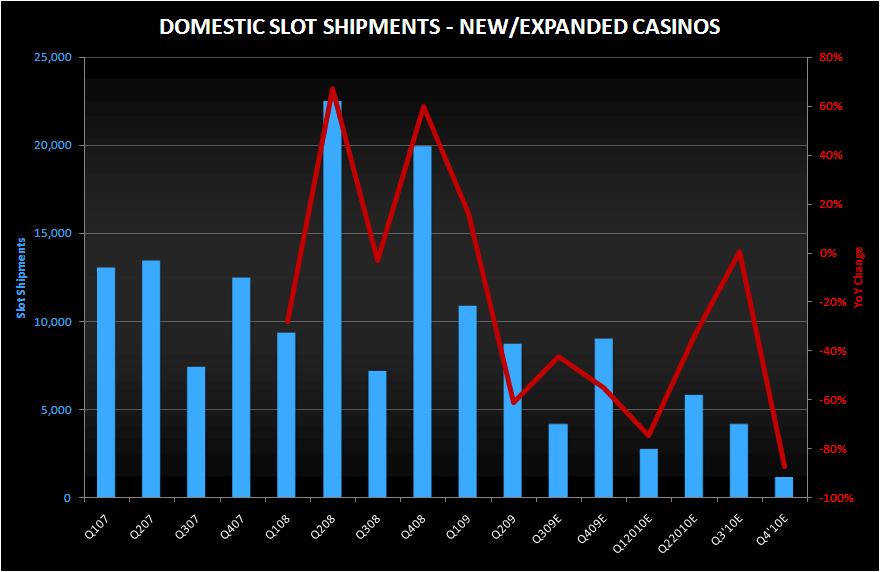

The chart below shows our forecast for slot sales into new and expanded casinos in North America. As we've been saying for awhile, the picture isn't pretty. Fortunately, replacement demand is poised to bounce off the bottom as casino operator balance sheets have improved dramatically in the past few months. See our 05/15/09 post "IGT: MGM, CREDIT MARKETS, AND REPLACEMENT DEMAND". Anecdotally, we've already heard that certain properties are accelerating replacements.

Changes from our last new casino and expansion update are as follows:

- 2009: ~33k up from 20k (early 2010 shipments moving to late 2009)

- 2010: 14k down from 24k

- 2011: 14k - does not include possible openings of Aqueduct ( up to 4,500 slots), a Lakes (LACO) casino in OK (1,200), and potential temporary facilities in MD and KS (permanent ones won't open before 2012)

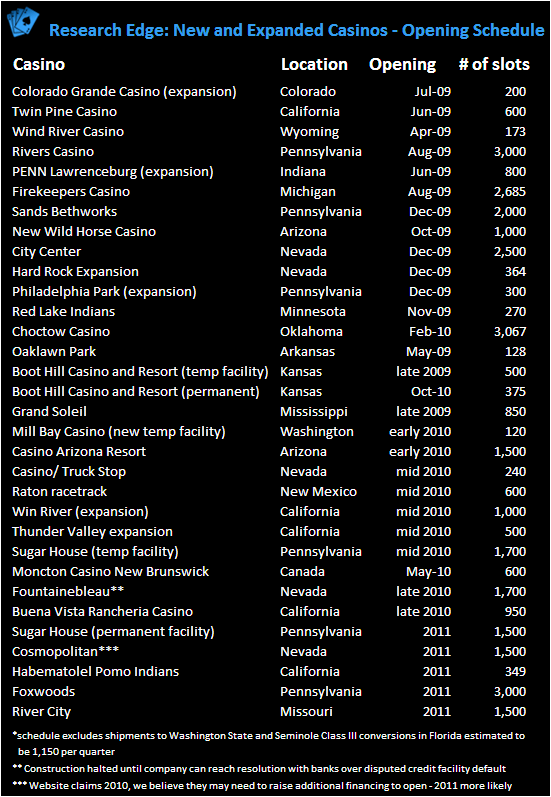

The following table lists all of the new casinos and expansions opening through 2011: