SUMMARY

Forecasting Folly: If you’ve followed us for any period of time, the fact that we don’t pretend to have an edge on the monthly NFP figure is not a surprise.

The BLS and ADP figures are certainly co-integrated on a multi-month basis and the trend in the initial claims and other higher frequency employment data can offer some probability weighted, directional insight and some fertile fodder for the tea leafers, but predictive value on a month to month basis is notoriously poor.

It’s not the number itself, but the markets reaction to it that drives our subsequent allocations.

Summary Take: In short, +74K was a disappointment vs. prevailing expectations and an outlier verses the balance of higher frequency labor market data. We wouldn't dismiss today's data outright, but we wouldn't materially shift our positioning on a single, outlier print.

With 273K people out of work due to bad weather (vs. an average of 166K over the prior 5 December’s) weather is being held out as the biggest distortive factor. With our retail and restaurant analysts (who rarely cite weather as a discrete swing factor) citing weather as a drag on traffic also, we'll assume the unusually inclement weather likely did, indeed, have some impact on construction and transports/trade employment and drag on hours worked.

Strategy: The unsurprising price response to today’s data is down dollar/down bonds as “no-taper” expectations get priced in at the margin. We outlined how to play a breakdown in the dollar in our 1Q14 macro themes call yesterday (REPLAY) – While we'll monitor the dollar weakness closely, in regards to the more immediate term and today’s employment data specifically, we’ll take the other side of overbought/oversold moves in today’s price action.

In the context of the broader labor market data, where the preponderance of evidence remains positive with ADP, initial claims, ISM mfg and ISM services all reflecting moderate, ongoing improvement, the BLS data sits as a single negative outlier.

Unless we see confirming fundamental evidence alongside a shift in risk management signals (across SPX, VIX, DXY, 10Y Treasury), we’re unlikely to pivot on our generally positive view of the domestic labor market because of today’s data in isolation – particularly given the positive revision, the weather caveat and the ongoing, significant seasonal distortion.

Keith shorted BOND (etf) and long-term treasuries (TLT) in real-time alerts on this morning’s weakness in yields.

DECEMBER EMPLOYMENT REVIEW: Below we review, in detail, this morning’s employment data from the BLS, highlight some potential issues impacting the January release and take a summary look at trends in the distribution of employment.

- Household Survey Employment (CPS): Employment as measured by the Household Survey increased +143K on the back of last month’s reported +958K increase. The household survey is notabably volatile but, similar to the ADP data, is consistent with the NFP figures on a multi-month moving average basis.

- Unemployment rate: Declined to 6.7% from 7.0% as total unemployed dropped -490K and total employed increased +143K

- Labor Force Participation: Dropped another 19bps sequentially to 62.79 from 62.98 as the total labor force dropped -347K MoM (the net of -490K unemployed plus +143K increase in employment) and civilian population increased +178K

- Weekly Hours: Down small to 34.4 vs. 34.5 prior (likely impacted by weather)

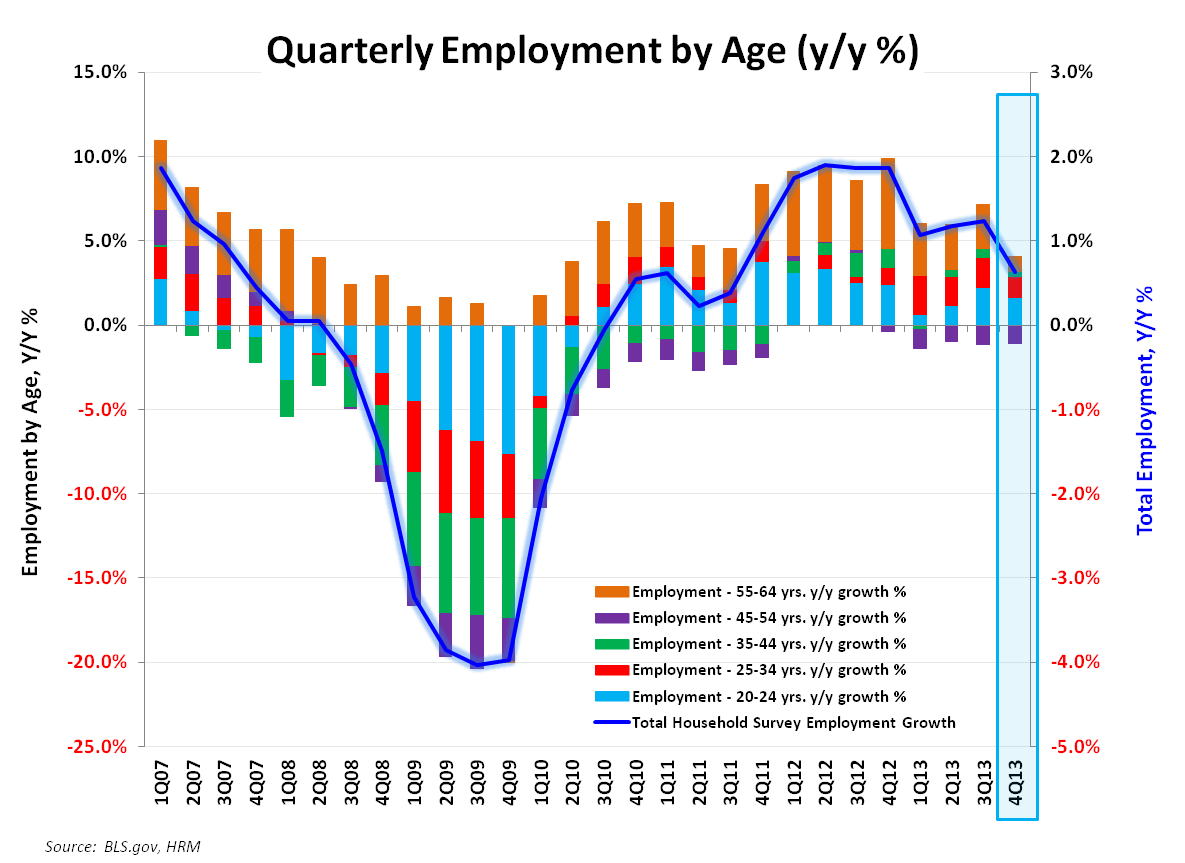

- Employment by Age: each age cohort across the 20-44 Year old demographics accelerated sequentially while employment growth for 45-64 year olds decelerated in December.

- Government Employment: State & local gov’t employment growth holding positive for a six consecutive month while Federal payroll growth held flat at -2.8% YoY to close the year.

- Ave Hourly Earnings: Earnings slowed 20bps sequentially to 1.8% YoY. Not a growth number particularly supportive of accelerating consumption

- Revision: the establishment report showed a net positive two month revision of +38K with the October estimate unchanged and November revised to 241K from 203K last month, Household Survey revised to +958K from +818K last month

- Part-time Employment: Part-time employment dropped 89K MoM, down -1.0% YoY. The Trend in part-time employment remains one of decline.

- Industry Level Notables: Construction employment (weather impacted) was the worst, dropping 16K MoM and ending a 6mo streak of positive gains. Notably, healthcare shed jobs for only the 2nd month in the last 10 years in December

EMPLOYMENT DISTRIBUTION: PRE-RECESSION vs. NOW

Below is a quick comparative study of the distribution of employment by industry in the peri-recession period. As can be seen, at the broader Industry level, the shifts have not been particularly outsized.

The prevailing bearish narrative that the post-recession economic edifice is structurally weaker and the employment recovery has been largely illusory because we’ve only added low wage and part-time jobs seems to be overstated.

Part-time employment is in retreat, Temp employment is increasing, construction and manufacturing jobs are currently seeing some positive momentum, and mining and energy employment (which generally pay comparatively higher wages) continue to gain in share, to name some positive dynamics.

Yes, participation is declining (in excess of that implied by demographics) and long-term and structural unemployment will remain TREND issues, but the great, job-quality-deterioration-narrative appears somewhat fallacious.

POTENTIAL JANUARY IMPACTS:

Unemployment Insurance: The loss of EU unemployment benefits for some 1.3M individuals at the close of the year has been well advertised. If jobless benefits aren’t renewed by congress and the bulk of those individuals move from unemployed to out of the labor force the LFPR will decline and the Unemployment Rate will benefit. The largest impacts, should this occur, are likely to be observed over the first couple months.

Annual Benchmark Revision: the Census Bureau applies an annual population control adjustment to the Civilian Non-institutional Population alongside the January release every year. Historically, the magnitude of the January adjustment has ranged from tens to hundreds of thousands or even millions of individuals. An outsized revision to the January 2014 data could shift the unemployment variable dynamics from their current trend

Christian B. Drake

Associate

@HedgeyeUSA