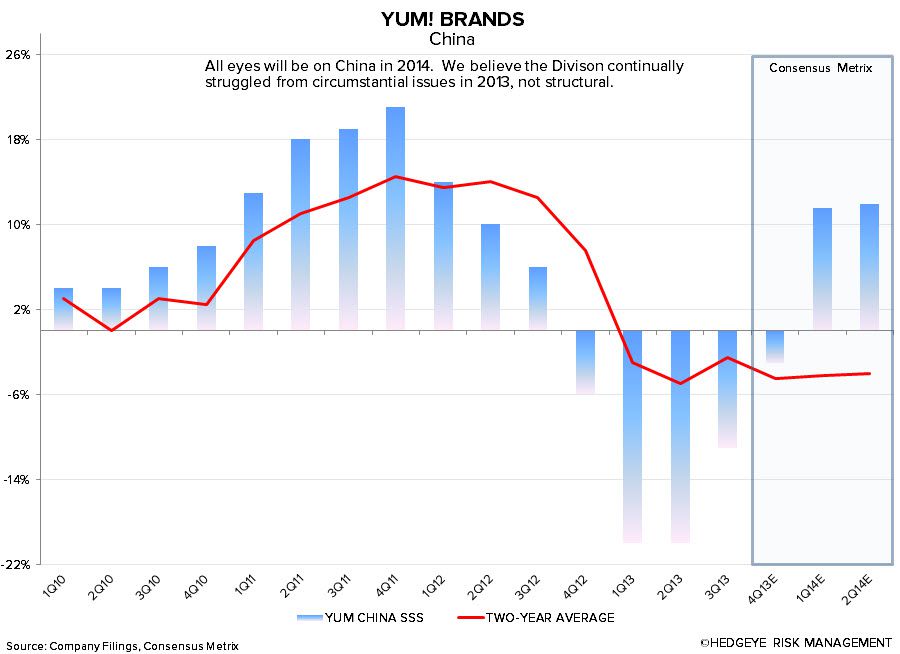

INVESTORS AREN’T SOLD ON A FULL RECOVERY IN CHINA

In light of yesterday’s downgrade, we’d like to reiterate our LONG call on YUM.

It is our belief that the vast underperformance of its China Division in 2013 was largely driven by circumstantial issues (food supplier incident and Avian Flu) rather than structural issues. In fact, we believe YUM continues to have a material opportunity to capitalize on a growing consumer class in China that is expected to double from 300mm+ in 2012 to 600mm+ by 2020. While China same-store sales could remain volatile in 2014, we believe they will accelerate meaningfully over the prior year.

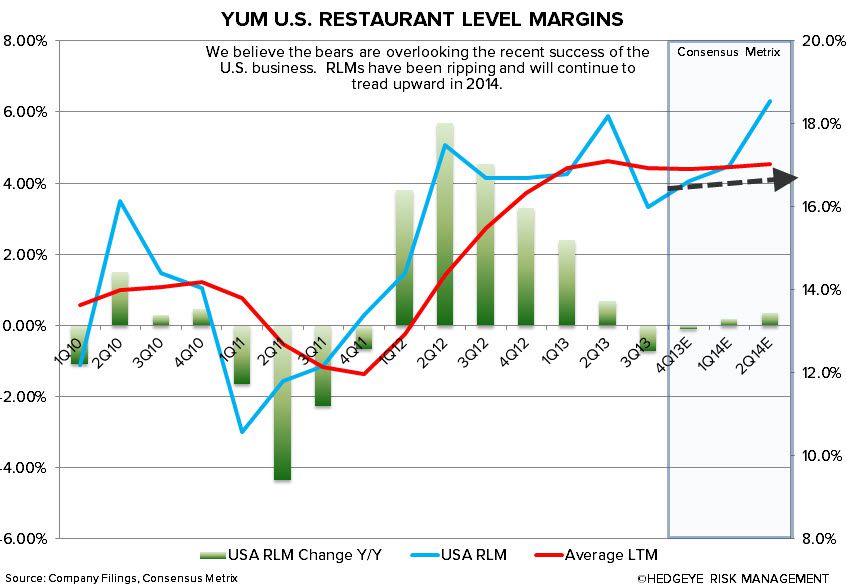

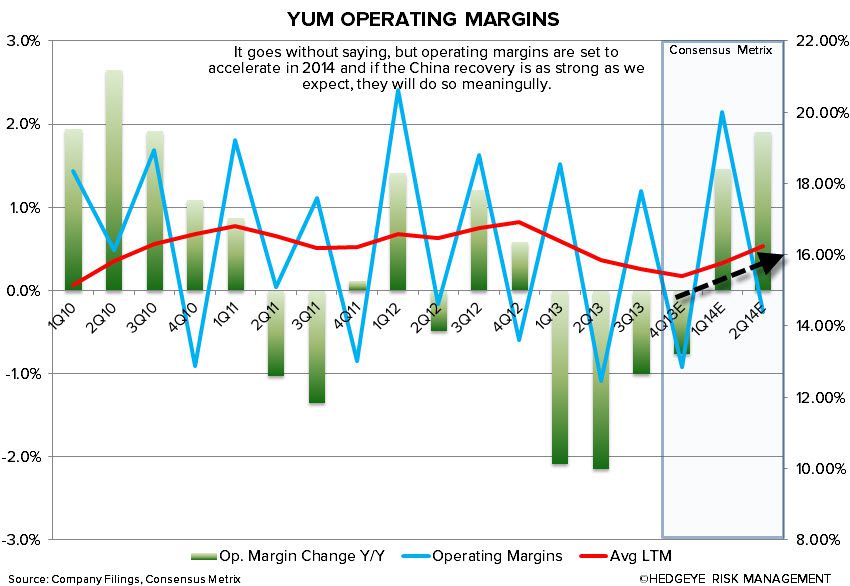

The trend in both sales and margins in China suggest that the company has made significant progress restructuring the business, setting the stage for improved profitability in 2014. We believe there is enough pessimism around a potential recovery in China (as evidenced by yesterday’s downgrade) that there is upside to estimates in 2014.

SUBSTANTIAL LONG-TERM GROWTH OPPORTUNITY

YUM is currently our favorite LONG in the big cap QSR landscape fueled by a substantial long-term growth opportunity, including a strong and growing presence in China as the country transitions from a producer to a consumer economy. We believe China same-store sales will not only benefit from easy comparisons, but will also be driven by incremental sales from menu innovation and daypart expansion in the region. In addition to China, YUM has positioned itself well for the future through considerable penetration in other developing markets.

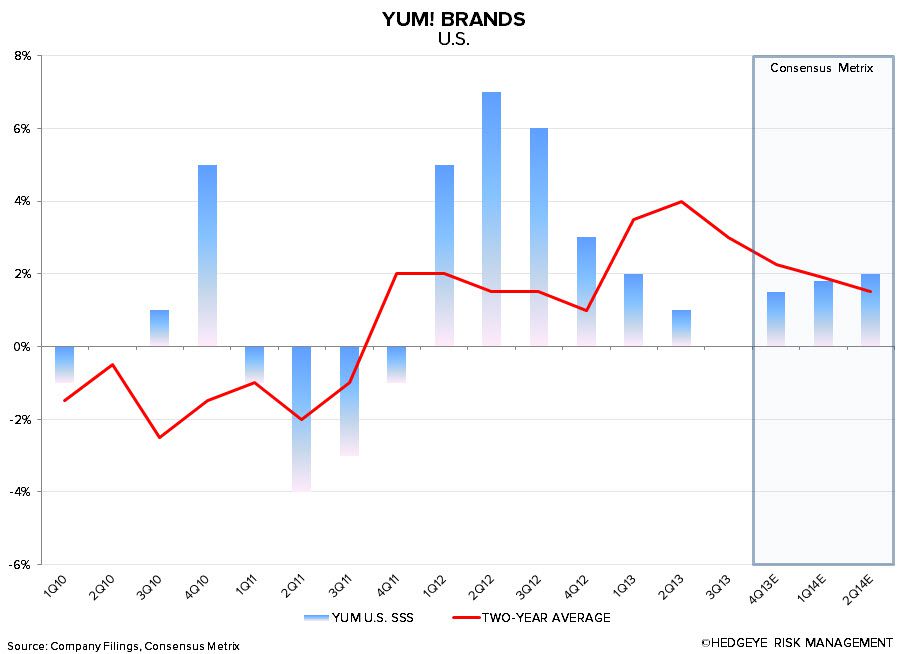

YUM has been strong in the U.S. for the past couple of years, led primarily by an innovative Taco Bell business. We believe the company has the correct drivers in place to capture additional market share and drive incremental sales at this concept. The breakfast daypart is a huge opportunity for Taco Bell and, if successful, could drive incremental gains.

WELL-POSITIONED FOR 2014

Easy same-store sales comparisons in China, improving margins across the major divisions, and a potential acceleration in domestic consumer spending could all lead to multiple expansion in 2014. Investors punished the stock on bad news for the majority of 2013 and, as such, we expect them to reward the stock on good news throughout 2014. As it stands, we see approximately 16-30% upside in the stock (depending on the trajectory of profitability in China), implying a stock price between $87 to $100 per share.

In the series of annotated charts below, we run through our bull case from a fundamental perspective. It quickly becomes clear that operating margins are set to accelerate and that a turnaround in China would have a considerable impact on the profitability and earnings of the company.

Feel free to call with questions.

Howard Penney

Managing Director