Better Data Equals More Upward Pressure on Rates

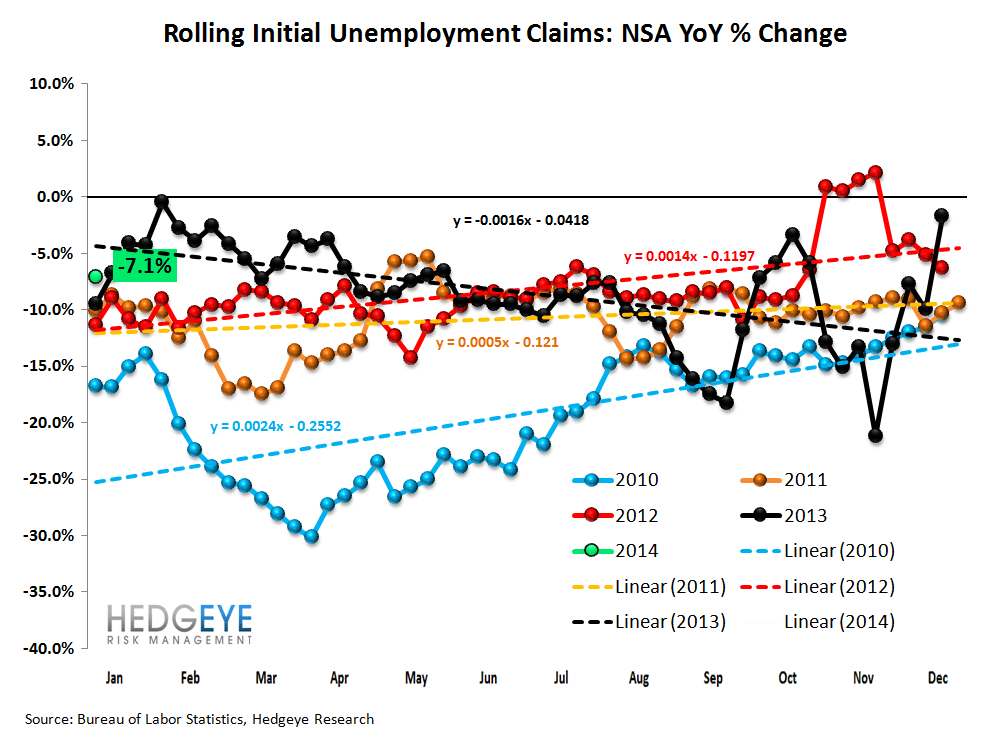

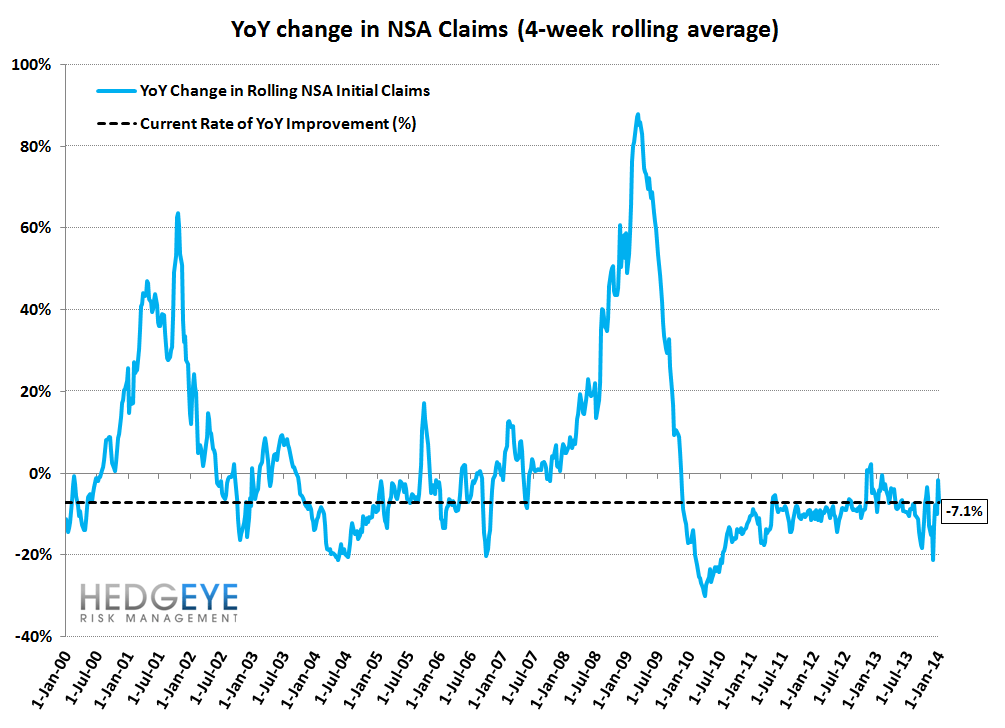

This most recent week brings to three the number of "clean" data weeks that have no been strung together. Our ability to contextualize what's happening in the labor market, as a result, is improving. In the last three weeks we've seen a strong and accelerating rate of year-over-year improvement in the non-seasonally adjusted initial jobless claims data. This most recent week was better by 12.9% y/y while the two preceding weeks were stronger by 8% apiece, on average.

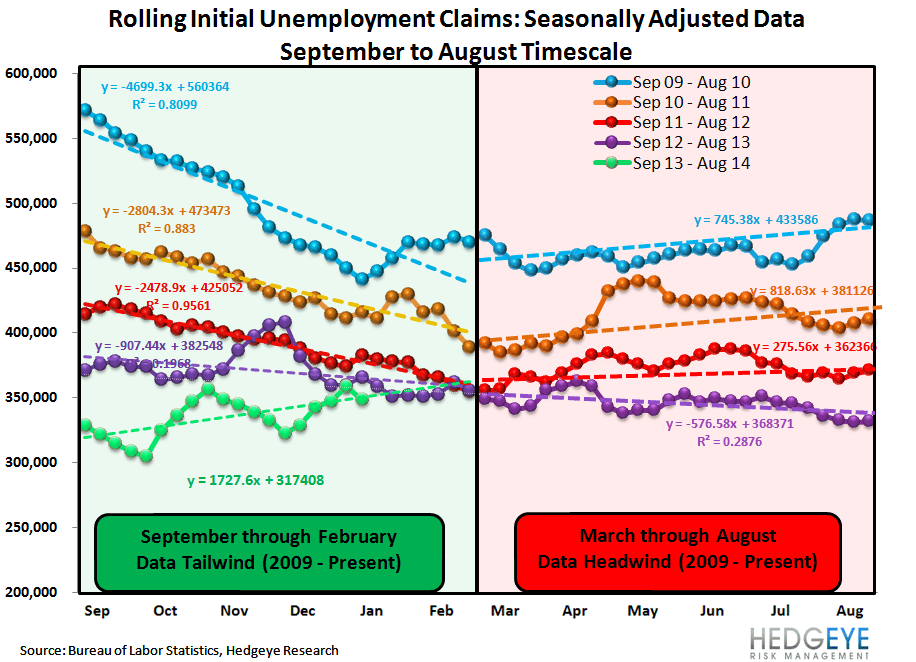

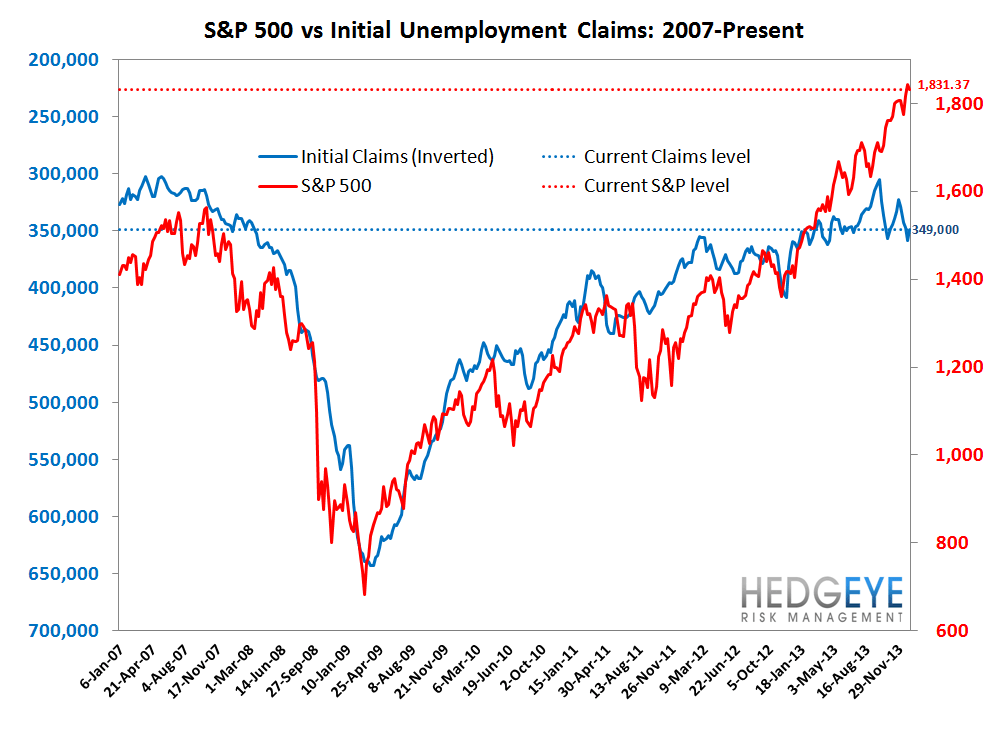

As we've been saying for some time now, the upward trajectory in the labor market will continue to exert upward pressure on the long end of the yield curve, which will help banks and hurt housing volume-sensitive stocks. We see no reason to expect this trend to change in the coming few months. In fact, the trend in the SA data should continue to accelerate as legacy seasonality distortions continue to ramp us a tailwind through the February/March timeframe.

The Numbers

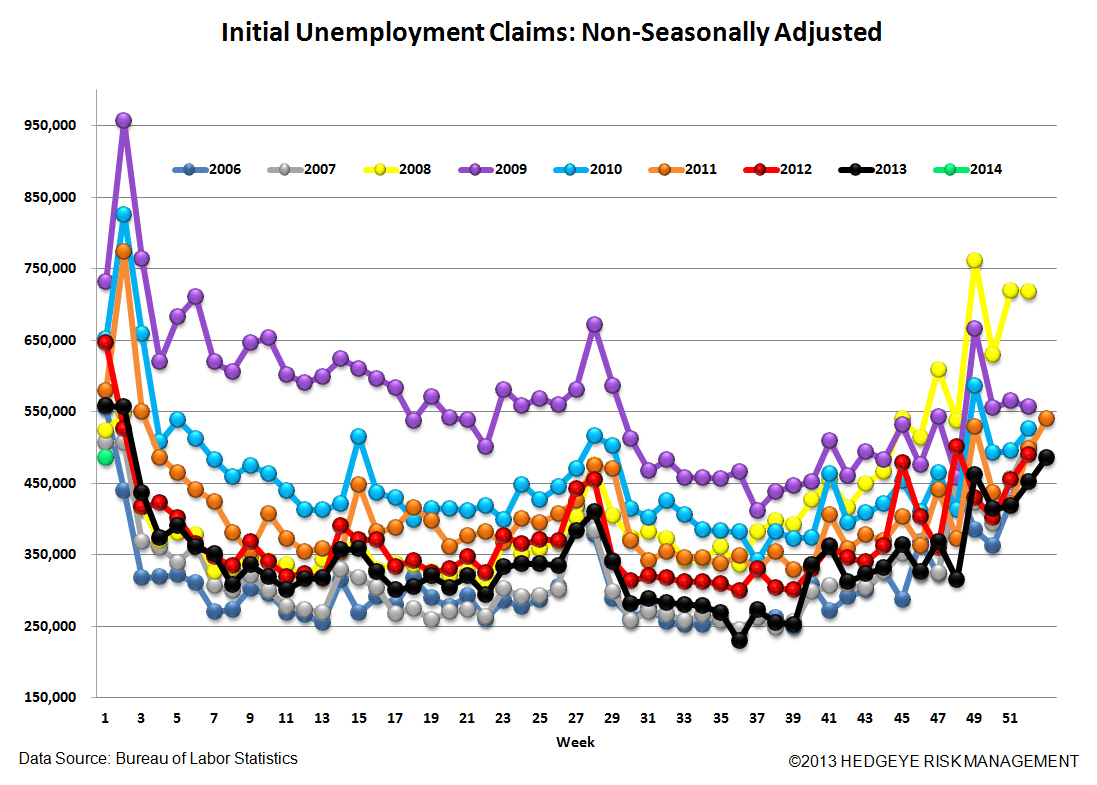

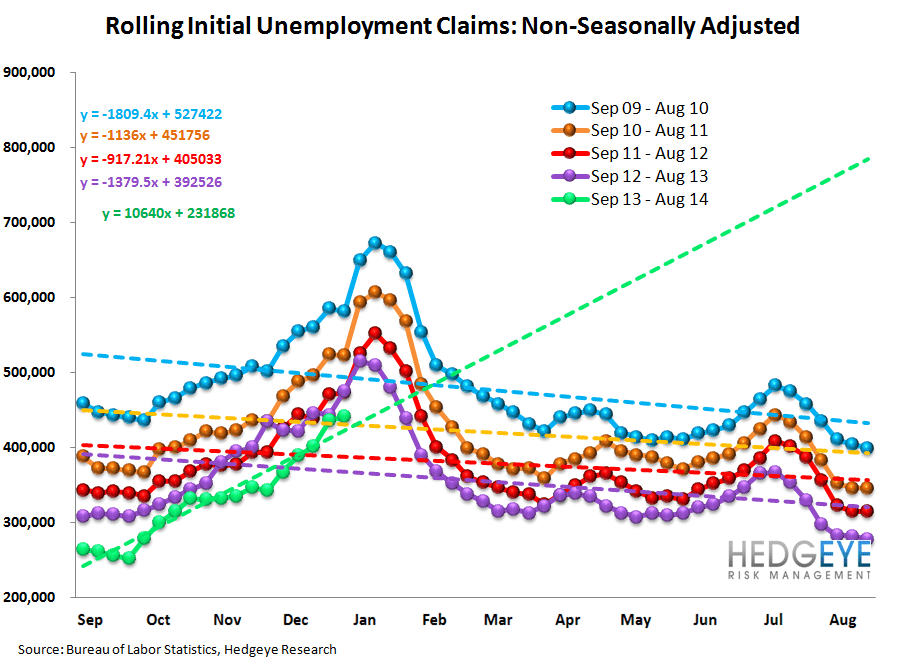

Prior to revision, initial jobless claims fell 9k to 330k from 339k WoW, as the prior week's number was revised up by 6k to 345k.

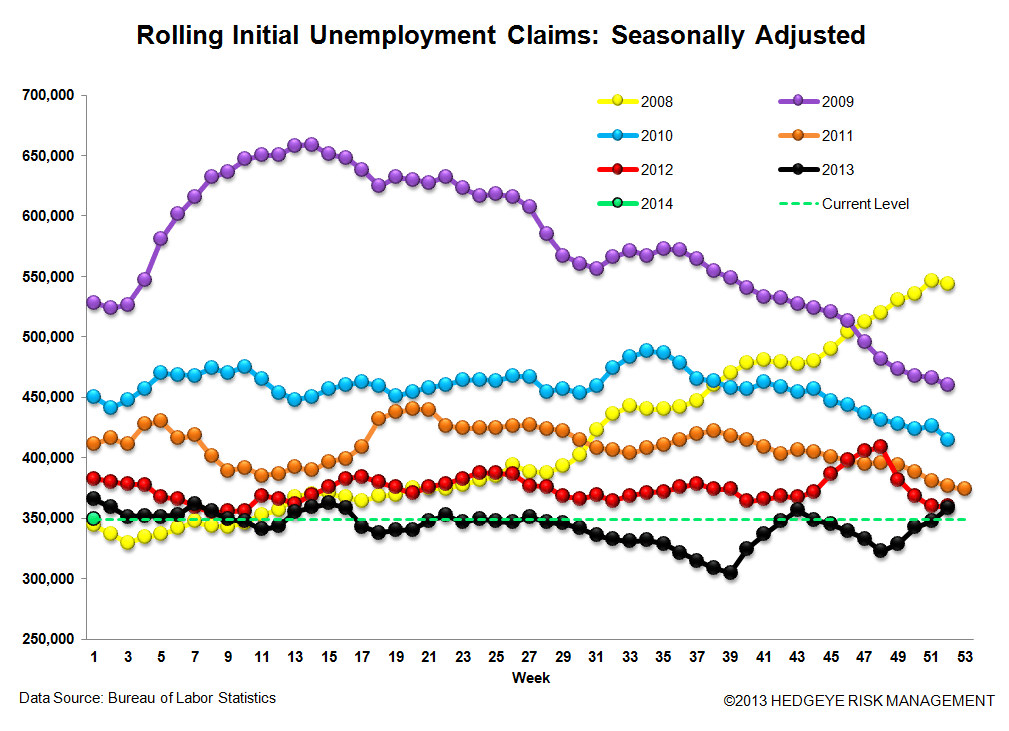

The headline (unrevised) number shows claims were lower by 15k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -9.75k WoW to 349k.

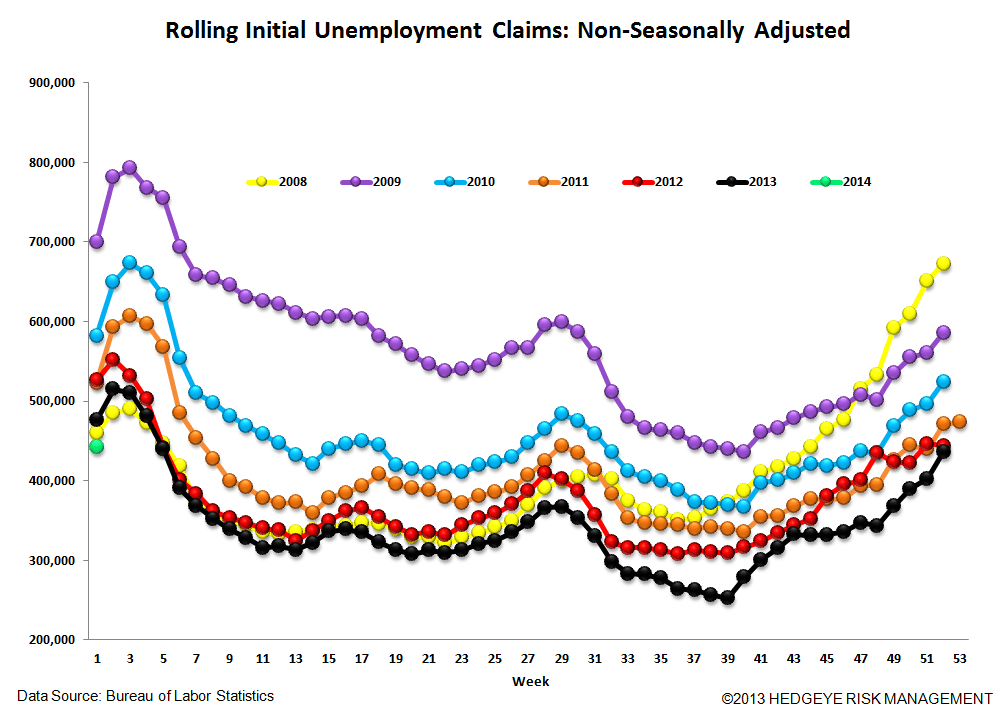

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -7.1% lower YoY, which is a sequential improvement versus the previous week's YoY change of -1.7%

Yield Spreads

The 2-10 spread fell -9 basis points WoW to 256 bps. 1Q14TD, the 2-10 spread is averaging 257 bps, which is higher by 17 bps relative to 4Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT