“There was certainly never a more inopportune time to launch a new business.”

-S.S. McClure

That’s what Irish born Samuel Sidney McClure said after the Panic of 1893 as he founded one of the most important investigative research companies in US history – McClure’s Magazine.

“He dreamed of creating a full time staff of writers who would be guaranteed salary and generous expense accounts. The job of staff writer was a new concept; in years to come, McClure would claim he himself almost invented it – a justifiable assertion…” (Doris Kearns Goodwin in The Bully Pulpit, pg 169)

Old School Research. That was what McClure’s Ida Tarbell, who exposed Standard Oil to America and helped force its breakup, did. Today’s stroking of government officials and storytelling execs in exchange for media access would be considered shameful back then. We started Hedgeye in 2008 to change that. Rather than fearing the system itself, opportunity knocked to change it.

Back to the Global Macro Grind…

With change comes trial and error. The first thing we needed to change was the platform of delivery. Not having the conflicts of interests embedded in a broker-dealer, investment bank, or advertising business was an easy change to make.

Changing the process, language, and pace of research communication was tougher. Technology (Google, Twitter, @HedgeyeTV, etc.) is now making this less tough. When your principles are transparency, accountability, and trust – all tech tools can do is expedite your vision.

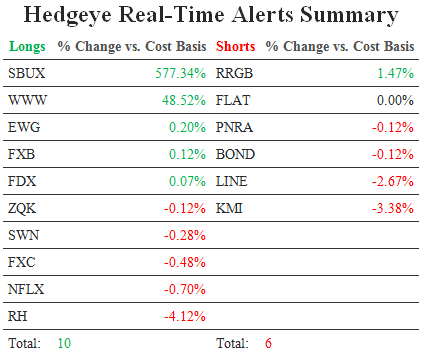

Given the circumstances (a raging bull stock market), I think our analysts have done a great job shining a flashlight on what’s really going on at big US corporations in the last year: Caterpillar (CAT), McDonald’s (MCD) and Kinder Morgan (KMI) – that something is not always good. On macro matters however, some of the best opportunities in the last year have been in revealing what’s actually improving.

Today we’ll be hosting our most popular Institutional Research event – our Q1 Global Macro Themes Conference Call. If you’re an institutional investor, please ping for access.

Our Macro Research Team does this call quarterly. There are 3 themes per call with anywhere from 45-75 slides of proprietary research and data. The idea of the call is to highlight the big themes in macro that are A) changing or B) trending.

In the case of A):

- Our models focus on rate of change (2nd derivative, slope of the line)

- The 3 Big Macs (macro factors) Growth, Inflation, and Policy (our GIP Model)

- Inflation is going to be the biggest change we focus on today (both locally and globally)

In the case of B):

- This happens most of the time in macro – that’s why we call them TRENDs (they trend)

- @Hedgeye TRENDs can either be cyclical or secular (sometimes both)

- On Twitter, I highjack the hash-tag on TRENDs we see developing before consensus does (#RatesRising, for example)

Today’s Hedgeye research hash-tags (Global Macro Themes for Q1) are going to be as follows:

- #InflationAccelerating

- #GrowthDivergences

- #FlowShows

#InflationAccelerating is a reversal from former Hedge Macro Themes #DeflatingTheInflation and #Bubble#3.

I know, too many hash-tags!

Bubble #3, of course, was Bernanke’s Commodity Bubble (2011-2012). You know, the one where you saw all time highs in Gold, Food, etc. – the one where the Fed would say they “see no inflation, because there is none in iPods.”

So that deflated (commodities crashed), and now The Economist has “The Perils of Deflation” on its cover as Ben Bernanke takes a “nailed it” victory lap around the weenie bins.

Inflation expectations are already rising. But you already know that – because we don’t do research on a lag. That and the #GrowthDivergences you are seeing manifest between Europe and Asia aren’t new either. With South Korea’s KOSPI -3.3% YTD versus Austria and Denmark’s stock market’s already +4.7% YTD, Mr. Macro Market gives you the research “call” every day.

From our un-conflicted and un-compromised financial media distribution platform, all we have to worry about is staying true to our principles. They will inevitably lead us to the truth. And, while there will never be an opportune time to be wrong about the truth, there will always be an opportunity to learn from our mistakes and improve our investigative research process.

Our immediate-term Risk Ranges are now:

SPX 1

DAX 9

KOSPI 1

VIX 11.91-14.45

USD 80.73-81.34

Gold 1191-1246

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer