If there is any company on the planet that can consistently find a way to disappoint more than JCP, we’d love to see it. Everyone is saying the same thing this morning, so we’ll try not to be repetitive. On one hand, the fact that the company came out and reaffirmed guidance is positive. It’ll be the only department store this quarter to have positive comps and margins. But on the flip side, do you think that they could have given us a number or two? It’s not much to ask. After all, almost every sales update that they have ever issued included numbers. We don’t think sales updates are critical for a retailer, but it’s kind of like a dividend – once you start, you can’t stop – and you certainly can’t give less information over time (unless you want to destroy equity value). This thing is down, obviously, and it deserves to be. JCP holders should be irate. We are.

There are 2 key questions we need to ask ourselves. 1) What are they hiding, 2) does this change the thesis we outlined in our Long Summary last night (The Search for Doubles and Triples), and 3) What does this mean for expectations and sentiment?

1) Hiding? Our sense is that they’re not hiding much of anything. They’re hoping. Sales growth absolutely tapered since the 10% comp issued around Black Friday. We all know that. If we assume that management’s “positive comps” translates into 3% for the quarter (below consensus of 6%) then the 2-year comp is an atrocious below -30% level as opposed to simply being ‘really bad’ in the -20s (which people expected. We think that the vagueness is driven by one factor alone – the possibility of making up for a weak December in the month of January. Hope. That means that JCP kicks up the promotional engine. If we were another department store, we wouldn’t want to compete with a promotional JCP – given that its’ Gross Margin is already sitting so far below its peers. But our obvious concern is that JCP will pick comp in Jan over margin. We understand it needs to rebuild customer loyalty (traffic/comp), but at some point it’s going to have to start making money on the revenue. Last we checked, cash is pretty important.

2) Does this change our thesis? Well… it certainly doesn’t change the fact that this one is last in our Long queue. One thing that could change our thesis is if the company is taking it on the chin with Gross Margin, and still is not seeing any sales acceleration. Gross Margin is the last offensive weapon JCP has. If it shoots and consistently misses the target, then it definitely impacts our call. But for now, we think that even with a 3% comp and 30% GM, liquidity is definitely not an issue this quarter. Importantly, even if we are to cut our comp assumptions in half next year, liquidity is still not a problem. Finally, if the recovery stalls here, there’s one thing you can bank on – Ullman being shown the door. Yes, the Board backed him publicly, but what are they going to say to all the employees (the primary audience of all those management-related messages we selfishly think are directed towards us) “Hey everybody, your boss is probably going to be fired really soon. Happy holidays!”. We think not.

3) Sentiment: The market is already speaking out loud on this one – something that started when someone had the inside information and started trading the stock down yesterday. In addition, when JCP reported its last quarter and issued the guidance (that it just blessed) the stock was at $8.71. Now with a reiteration of that guidance the stock is struggling to hold $7.50. That’s off 14% on a like for like basis. At the same time, sentiment is already the worst of any name in the S&P (see our sentiment monitor below which triangulates buy side, sell side, and inside transactions). There are 89mm shares short, or 30% of the float. To put that in perspective before the secondary – when liquidity was a massive concern -- there were 67mm shares short. Now it’s far more heavily shorted despite having patched up the greatest market concern. This is one thing that keeps us on the positive side.

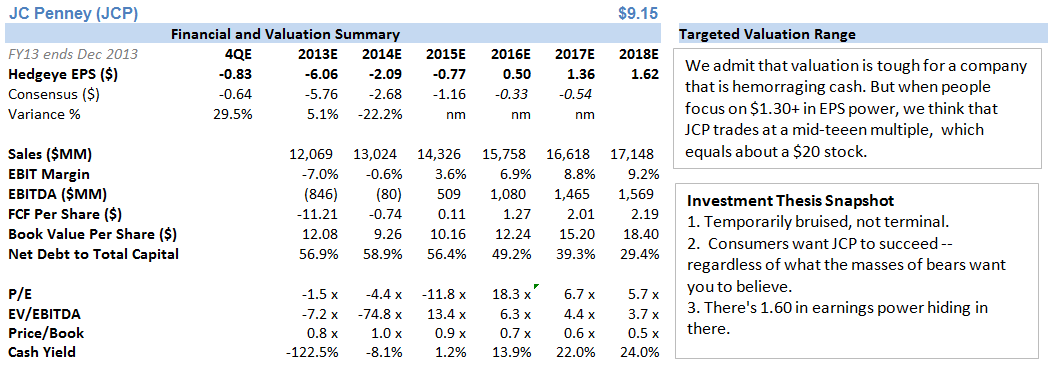

HERE'S OUR OVERVIEW ON JCP FROM LAST NIGHT'S LONG UPDATE

JC PENNEY (JCP) (#5 Out of 5 Ideas)

Not a day passes where I don't consider punting this one from the list of longs. Truth be told, it was much more fun being short Ackman at $42. But then I put back on my analytical cap, and come back to the fundamental premise of our long call. And that is that this company can be saved from its' widely accepted death. Our survey work suggests that consumers actually want JCP to succeed, even if Wall Street does not. To be clear, we're not talking about JCP returning to the mediocre retailer it once was. Today it is a horrendous retailer, and we simply think that it can upgrade to being a 'slightly better than bad' retailer. This is best measured by sales productivity. Today Kohl's is operating at $210/ft. JCP's prior peak is close to $190. Current day JCP is cruising along at a whopping $100/ft. We're not suggesting that it could get to $190/ft --- or even $150/ft. But based on everything we learned from consumers we think the JCP can revisit the $140 mark. That's still below Sears, by the way. That, combined with a mid/high single digit EBIT margin gets us to around $1.50 in earnings power. Now…unlike the other quality companies featured in this note, with JCP we've got to deal with another 2-years of cash burn. Two points of good news; 1) it has the cash, unlike earlier this year, and 2) the consensus has the company burning cash in perpetuity. That's simply not realistic -- unless our consumer research all of a sudden turns out to be flat out wrong.

So how do we value a name like this? We're uncomfortable using earnings given the debt burden. But a 8x EBITDA multiple -- which we think is fair for a company that is rebounding like JCP should and is de-levering, gets us to around $16-$17 in 2-years. Definitely the highest-risk double we have on the sheet, but it's one that we're sticking with -- until the research gives us reason not to.