Following the 4Q13 earnings call we wrote that SBUX was firing on all cylinders and, in fact, they were. However, as we published in a note on 12/18, we believe SBUX is beginning to lose some momentum and could struggle in the first half of fiscal 2014. But before we get into that, we will briefly highlight why we continue to like the long-term prospects of the company.

LONG-TERM BULL CASE

The bull case for Starbucks is clear: a strong commodity tailwind, high-single digit same-store sales, expanding margins, an international white space growth opportunity, a recovery in the EMEA segment, and expansion into new segments of the global food and beverage industry are all long-term bullish factors moving forward.

For the most part, these levers are still in place and the secular opportunity for the company remains attractive. Having learned from past experience, we believe management is well prepared to take advantage of this. To this point, management has made some significant investments in order to capture these opportunities. The chart below illustrates this point and shows that Starbucks’ return on incremental invested capital has recovered from the lows of 2012. For these reasons, we remain bullish on a long-term basis.

SHORT-TERM BEAR CASE

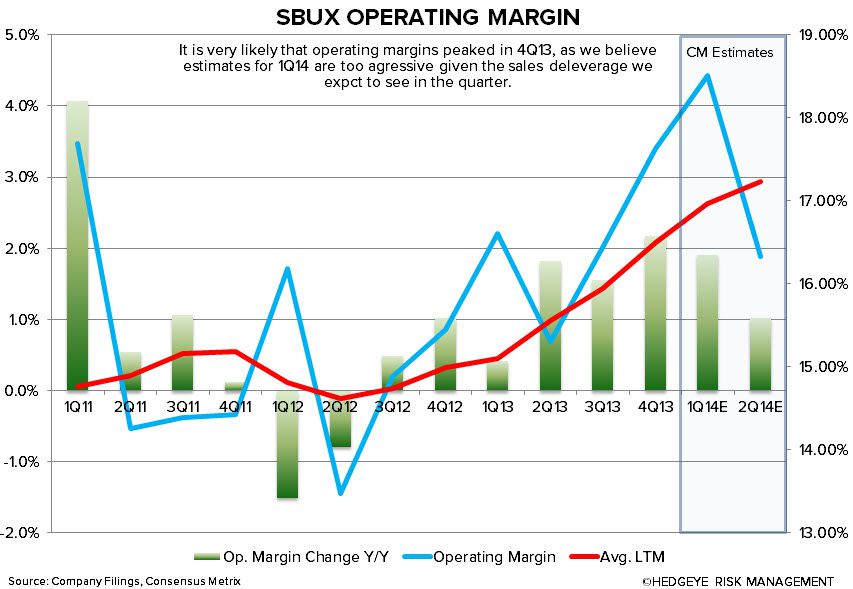

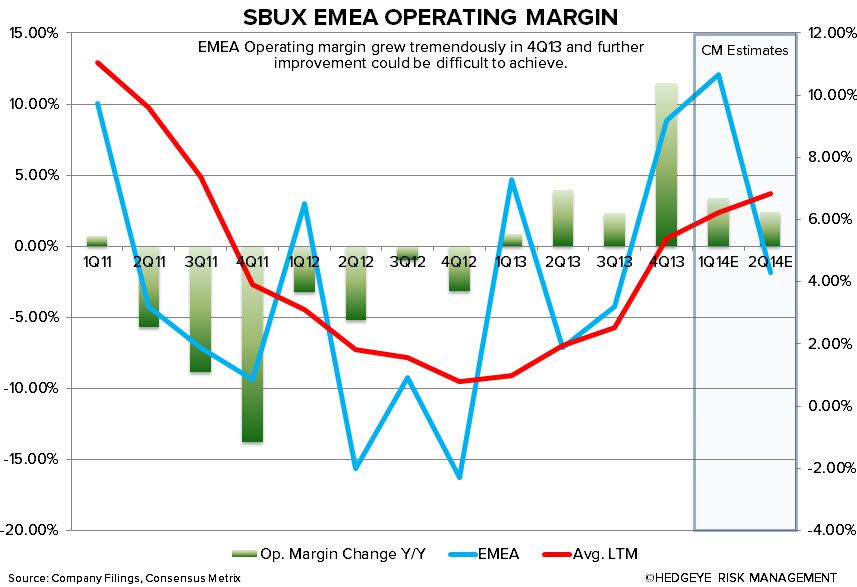

As we’ve written before, one of the only negatives we found in an otherwise all-star 4Q13 was management’s clear attempt to reign in expectations for FY14 (especially expectations for same-store sales in the Americas). While we initially viewed this as management’s attempt to simply bring estimates back down to earth, it appears they may have done so for a reason.

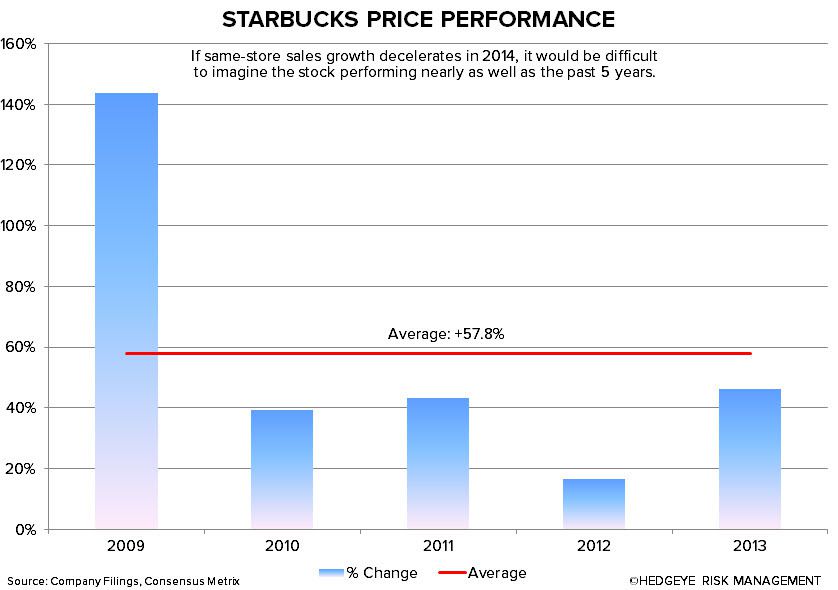

Our recent store visits in the Northeast suggest that the holiday season has not been as robust as anticipated. If this is the case, we believe the trickle-down effect on slowing same-store sales are not yet fully reflected in the current share price. With revenue growth decelerating, valuation close to a 3-year high and the likelihood that earnings will be revised down over the coming months, we see some short-term downside in the stock.

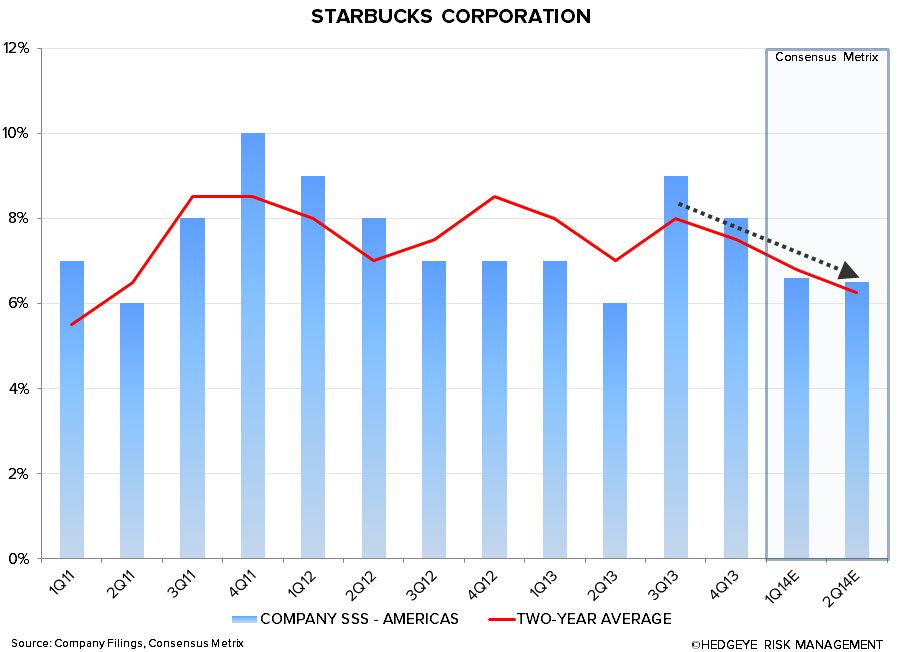

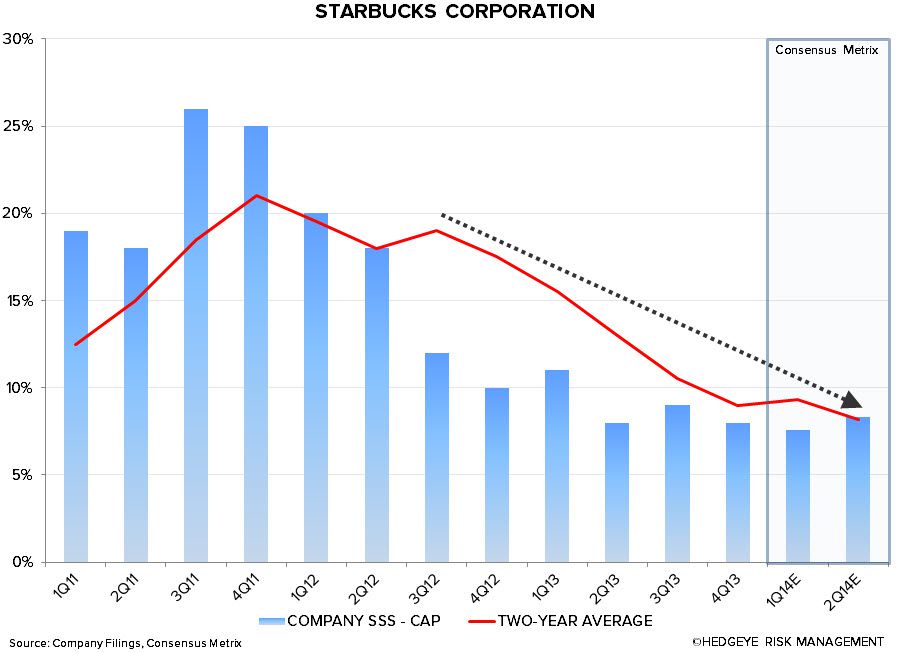

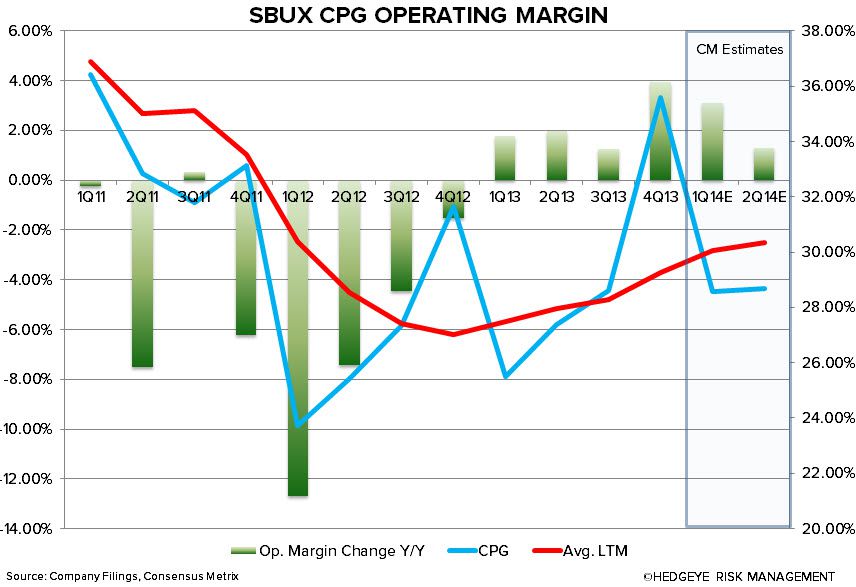

Below, we visually run through the short-term bear case from a fundamental and sentiment perspective in a series of annotated charts.

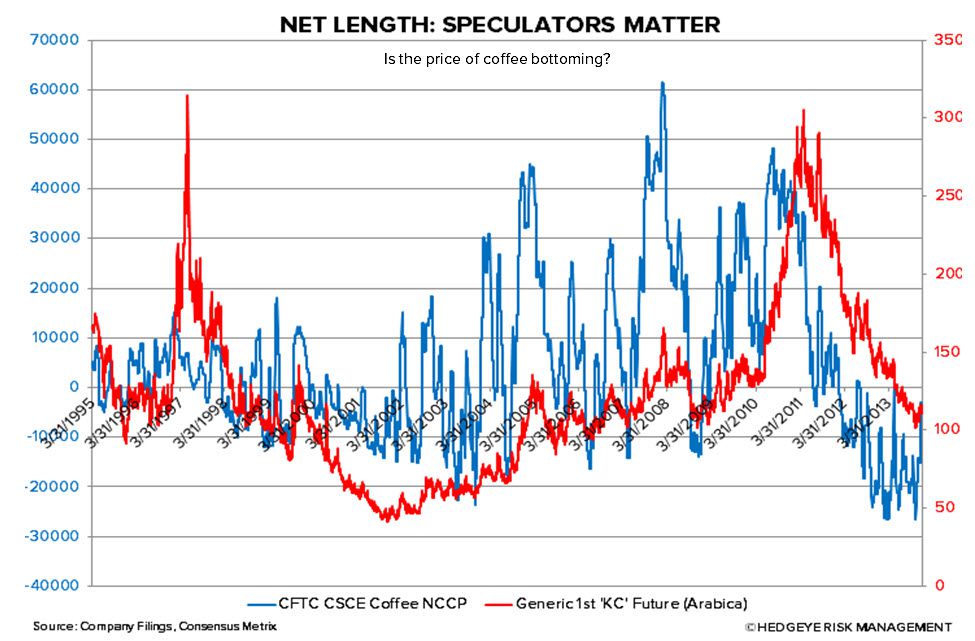

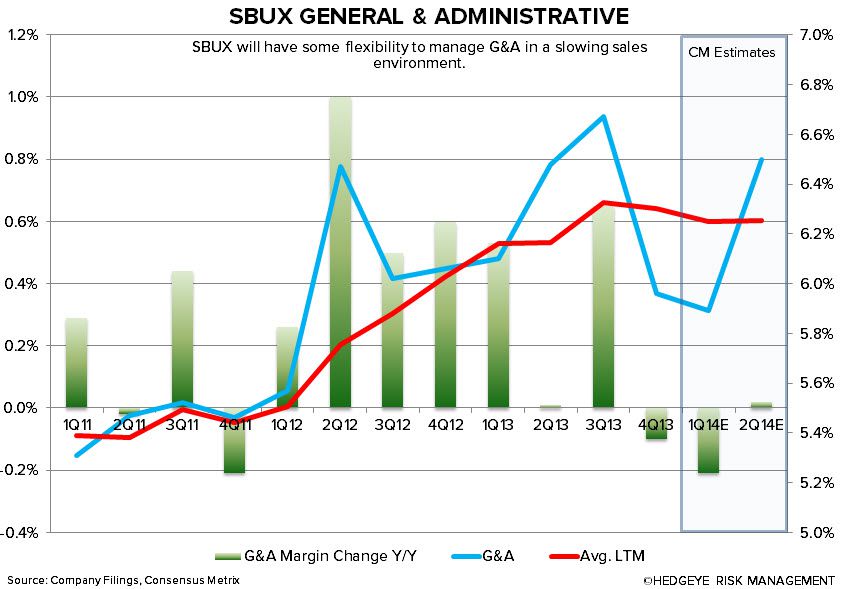

FUNDAMENTALS

SENTIMENT

Feel free to call with questions.

Howard Penney

Managing Director