TODAY’S S&P 500 SET-UP – January 6, 2014

As we look at today's setup for the S&P 500, the range is 35 points or 0.78% downside to 1817 and 1.13% upside to 1852.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.58 from 2.60

- VIX closed at 13.76 1 day percent change of -3.30%

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: ISM Non-Mfg Composite, Dec., est. 54.5 (prior 53.9)

- 10am: Factory Orders, Nov., est. 1.7% (prior -0.9%)

- 11:00am: Fed to purchase $1b-$1.5b in 2036-2043 sector

- 11:30am: U.S. to sell $28b 3-mo. bills, $26b 6-mo. bills

GOVERNMENT:

- Senate to vote on confirmation of Yellen as Fed Chairman

- Senate to consider unemployment benefit extension

- FEMA’s David Miller delivers opening remarks at National Research Council meeting on flood insurance, 10:15am

- Liz Cheney to end bid for Wyoming Senate seat, CNN, NYT report

WHAT TO WATCH:

- Yellen poised for Senate confirmation amid taper pullback

- JPMorgan’s Madoff case penalties may be announced Tues.: WSJ

- Boeing to build 777X at Seattle hub as union drops pensions

- Liberty’s Sirius deal may help finance TW Cable offer

- Men’s Wearhouse starts tender for Jos. A Bank, nominates two

- Carlyle, KKR said to be in $1.2b talks to buy Fleury

- Teva said near to naming Vigodman CEO after Levin ouster

- Intel CEO Krzanich gives preshow keynote for International CES

- JPMorgan settles Pittsburgh bank suit probing U.S. deal

- Google rolls out alliance to bring Android into car systems

- GM’s OnStar in talks w/Chinese providers for 4G car services

- Nvidia chip update narrows PC-smartphone gap to target gamers

- Ford China deliveries surge 49% in 2013, overtaking Toyota

- U.S. office rents increase in gradual market recovery: Reis

- Apple changes board bylaws in step to address diversity issue

- Bitcoin tops $1,000 again on Zynga accepting virtual currency

EARNINGS:

- Park Electrochemical (PKE) 6:30am, $0.28

- Sonic (SONC) 4:01pm, $0.13

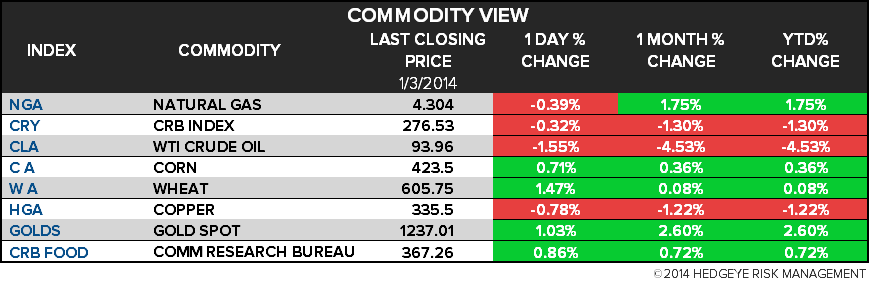

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Copper Declines Amid Concern Demand Is Poised to Slow in China

- Gold Swings Below 3-Week High as Investors Weigh Dollar, Demand

- Gold Analysts Get Most Bullish in a Year After Rout: Commodities

- Frost May Damage as Much as 15% of Florida Orange Crop, MDA Says

- Brent Rises for First Time in Five Days on U.S. Cold Snap, Iraq

- Sugar Extends Two-Week Low on Excess Supplies; Coffee Advances

- ‘Polar Pig’ Threatens Coldest U.S. Weather in Two Decades

- LME Hires Sloan from NYSE Euronext as COO, Head of Strategy

- Cotton Imports by China May Tumble to Six-Year Low, Group Says

- China Rejecting U.S. Corn as First Shipment From Ukraine Arrives

- China Smog Drives Lump Ore to Record Premium: Chart of the Day

- U.S. Winter-Wheat Plantings Rise to Six Year High, Survey Shows

- Gold’s Point-Figure Signals Further Declines: Technical Analysis

- U.S. Exporters Sell Wheat to Unknown Destination, Corn to Mexico

- Wheat Extends Rally as Cold Weather Threatens U.S. Crop Outlook

CURRENCIES

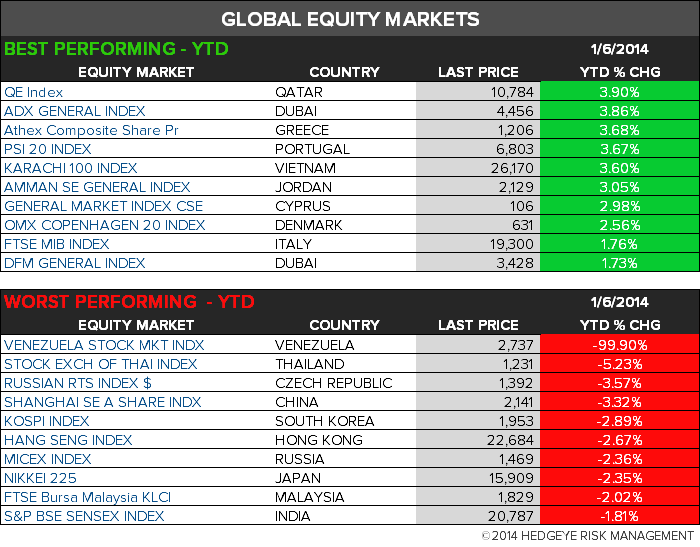

GLOBAL PERFORMANCE

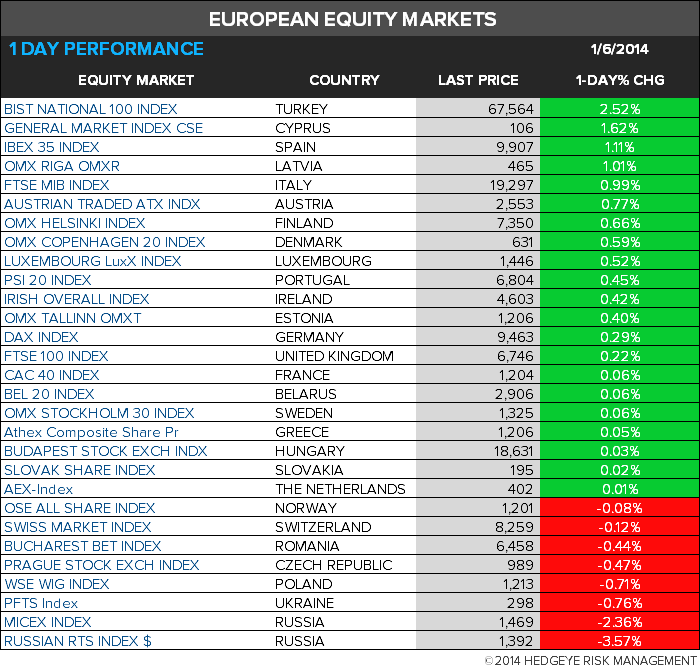

EUROPEAN MARKETS

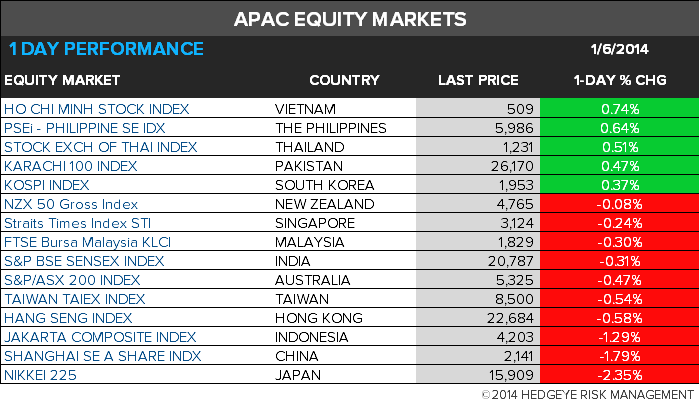

ASIAN MARKETS

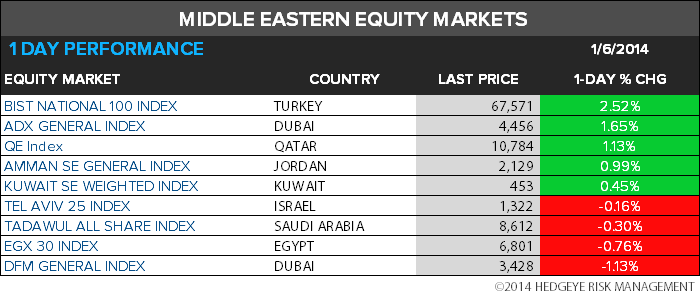

MIDDLE EAST

The Hedgeye Macro Team