This note was originally published at 8am on December 23, 2013 for Hedgeye subscribers.

“The mass of the American people are most emphatically not in the deplorable condition of which you speak.”

-Theodore Roosevelt

That’s what a 28-yr old Teddy Roosevelt said to a fear-mongering-class-warfare-guy when he ran for mayor of New York City in 1886. In one of the first debates of his career, he went on to pummel the parasitic politician with positivity and resolve:

“… the states-men and patriots of today are no more responsible for some people being poorer than they are for some people being shorter… if you had any conception of the true American spirit you would know we do not have “classes” at all on this side of the water…” (The Bully Pulpit, pg 126-127)

While a lot of people spent a lot of time whining about the #EOW (end of the world), government spending cuts, and #RatesRising in 2013, many of us went on doing what American Doers do – grow. Relative to where consensus was, this country hasn’t seen a growth surprise to the upside like this in a long-time. I’d like to thank all of you who grew your businesses for contributing to that.

Back to the Global Macro Grind…

As 2013 comes to an end, the year’s growth score-card will be reported on a lag. Mr. Macro Market obviously didn’t miss making this call in real-time however. What a run US GDP growth went on into the highs of Q313. #Boom!

At +4.12% GDP growth in Q3, the 1st takeaway shouldn’t be someone who missed it whining about “inventories” (newsflash: businesses build inventories as growth in demand accelerates – it’s called a cycle); it should be that GDP of +4.12% was actually understated!

The US GDP Deflator (subtracts from nominal growth to get you real-inflation-adjusted GDP growth) for Q313 was overstated at +2% (that compares with the MIT billion prices project of +1.7% and the CRB Commodities Index which was tracking -6-7% year-over-year). Which means nominal US GDP growth was over +6% in Q3 and the real print could have been 4.5-5%!

Hooowah!

The US stock market didn’t miss this. Neither did the Bond market (#RatesRising), nor Gold (crashing -29% YTD). The people who really missed this were actually the politicians. Who, like in 1886, were busy trying to tell stories about the economy they need you to believe rather than the one you had.

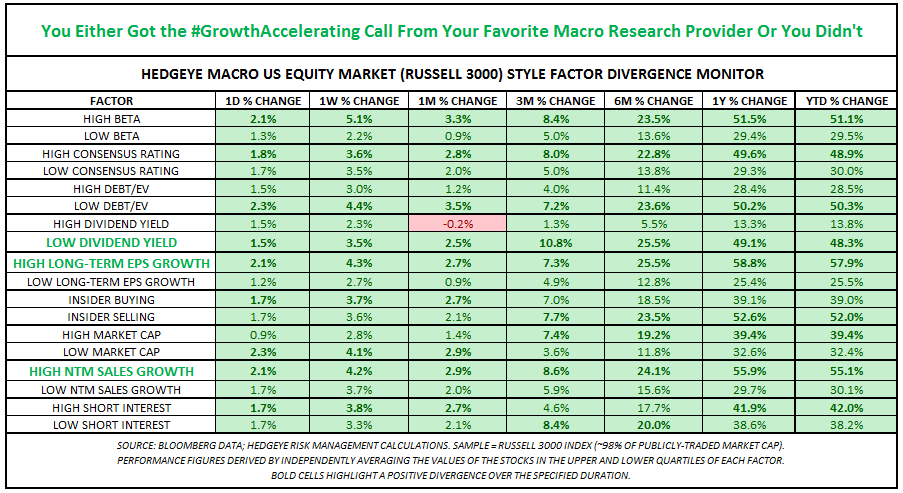

When we write about “growth” we’re talking about investment “style factors.” Here’s how the market prices those YTD:

- LOW YIELD STOCKS (i.e. growth stocks) = +44.2% YTD (vs slow-growth High Dividend Yield stocks +16.8%)

- TOP 25% EPS GROWTH STOCKS (by S&P quartile) = +40.4% YTD

- HIGH BETA STOCKS = +37.6% YTD

In other words, being long these GROWTH styles even beat the high flying US stock market indices:

- SP500 = +27.5% YTD

- Russell2000 = +35.0% YTD

- Nasdaq = +35.9% YTD

And obviously the major US Equities indices smoked being long things like:

- Fear (VIX) = -23.5% YTD

- Gold and Silver = -29.1% and -36.5% YTD

- Utilities (XLU) = +8.3% YTD

Utilities, MLPs, REITs got crushed relative to any domestic growth and/or cyclical sector of the US Stock market too:

- Consumer Discretionary (XLY) = +38.4% YTD

- Healthcare (XLV) = +37.7% YTD

- Industrials (XLI) = +35.3% YTD

And sure, some might quibble with Healthcare being called a US domestic “growth” sector, but that’s what we’ve called it since making it one of our favorite sectors in our Q113 Global Macro Themes, so they can quibble away.

Quibbling and whining might win people on your respective teams a few arguments, but these kinds of players (and class warfare dudes) don’t help you win championships. Those with open, objective, and flexible minds do.

The hardest thing to do in this business is having the humility to embrace that Mr. Macro Market might know something you don’t know. And clearly, whether by +4.12% GDP growth (old news now) and/or growth style factor performance in the marketplace, as the great behavioral philosopher Notorious B.I.G wrote, “if you don’t know, now you know.”

Our immediate-term Global Macro Risk Ranges are now:

SPX 1793-1826

VIX 13.01-14.91

Gold 1184-1229

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer