Summary

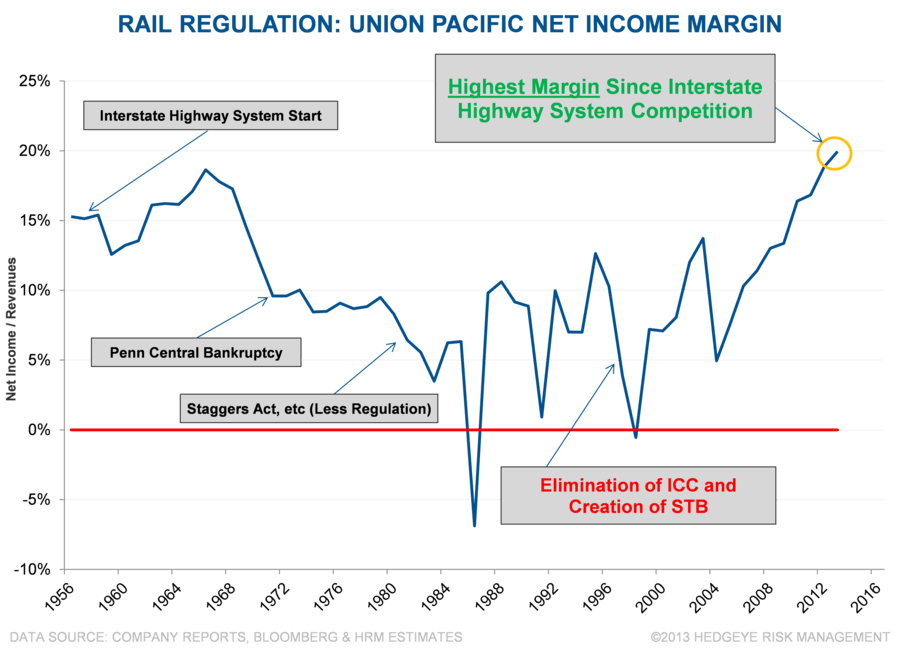

The history of railroad profitability is dominated by regulation and government intervention. Railroads have been regulated because, like utilities, they possess some characteristics of a natural monopoly. With current railroad profitability generally higher than at the start of the Interstate Highway System, will regulators gradually step back in? If hints emerge that the regulatory pendulum might swing back against railroads, it could prove negative for railroad share prices. If not, the favorable industry structure of the railroad industry may allow the continued high levels of profitability investors now expect.

RELATED TICKERS

UNP, NSC, CSX, KSU, BRK, CN CN, CP CN, GWR

KEY QUESTIONS

- What is the current posture of the STB and how does it differ from the former ICC’s?

- Can you discuss 'paper barriers' and other sources of anticompetitive concerns and whether they are viewed as relevant by regulators and lawmakers?

- How do Congress, the Obama Administration and the STB view the railroad industry and its resurgent profitability? How profitable can railroads get without more scrutiny?

- Are customers unhappy that cost reductions and efficiency improvements are not fully reflected in rates, similar to an actual utility?

- What form might additional regulation take and when might it come, if at all? What proposed legislation should investors currently focus on? Is it a matter of time before legislation passes?

- Will the expansion of the Panama Canal impact the industry and how do industry participants and regulators view the project?

- Who are the key players in Congress and in regulatory bodies and what are their agendas?

- Do recent railroad accidents increase scrutiny? Will increased oversight or additional costs emerge?

- Is there hope for high speed passenger rail in the U.S. and what does the future hold for Amtrak?

Please feel free to send question for Linda in advance of the call.

ABOUT LINDA J. MORGAN

Linda Morgan has 35 years of in-depth regulatory and legislative experience in the transportation industry, with a practice focusing on a variety of railroad and other regulatory and commercial transportation matters and associated legislative and policy issues.

Ms. Morgan's past experience includes acting as the Chairman, during President Clinton's Administration, of the former Interstate Commerce Commission (ICC), which became the Surface Transportation Board (STB) in 1996. During her 8 years as agency Chairman, she presided over numerous transportation regulatory proceedings, including rail rate and service matters and railroad merger cases of unprecedented national scope and complexity. In 1999, the Senate confirmed Ms. Morgan for a second term, and in 2001, President Bush asked for her continued service as Chairman until he designated a new Chairman in December 2002.

Prior to joining the ICC, Ms. Morgan served for 15 years as counsel with the Senate Committee on Commerce, Science, & Transportation, including seven years as General Counsel. During this period, Ms. Morgan was responsible for much of the legislation that established the framework for today's transportation system, including surface transportation policy that she later was in charge of implementing as Chairman of the ICC and the STB.

More background on Linda Morgan here: http://www.nossaman.com/lmorgan