Editor's note: This is an unlocked excerpt from Hedgeye's Financials team.

Two Clean Weeks

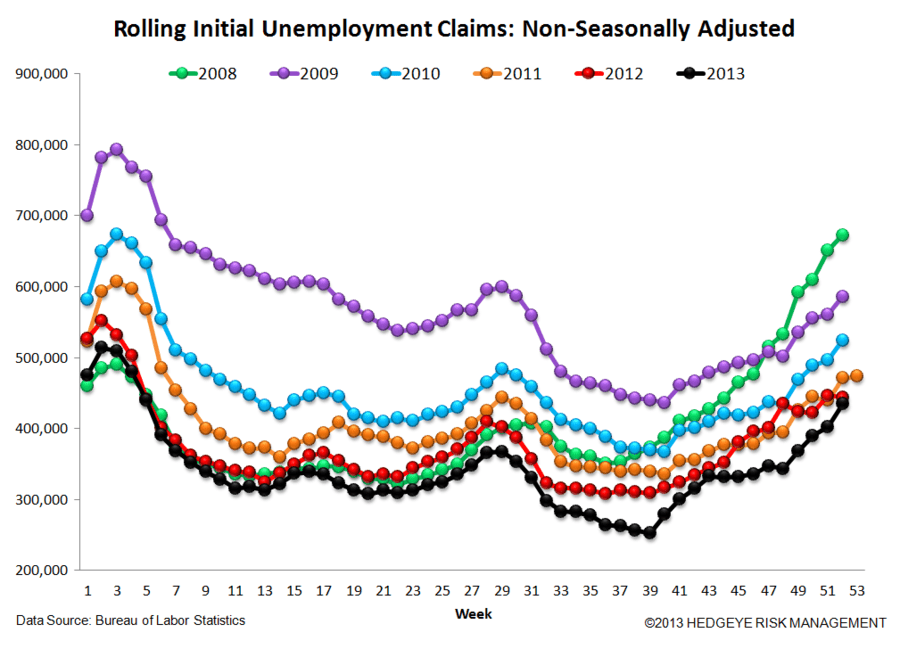

The last two weeks have finally provided a glimpse of normalcy in the labor market. The most recent week of data showed a 9.5% year-over-year improvement in initial claims, while the week prior showed an 8.2% year-over-year (y/y) improvement. The three months preceding that have been riddled with distortions, adjustments and comp issues making them all but unusable. Fortunately, the clean data at year-end reveals a continuation of trend for the labor market: strength. While we would no longer argue that the rate of change y/y is still accelerating, a high single digit rate of y/y improvement at this stage of the recovery is still quite strong.

As we've been arguing for some time now, the strengthening labor data is exerting upward pressure at the long end of the yield curve. Based on this, we continue to expect banks to have a macro tailwind into 1Q14 and builders to have a headwind.

The Data

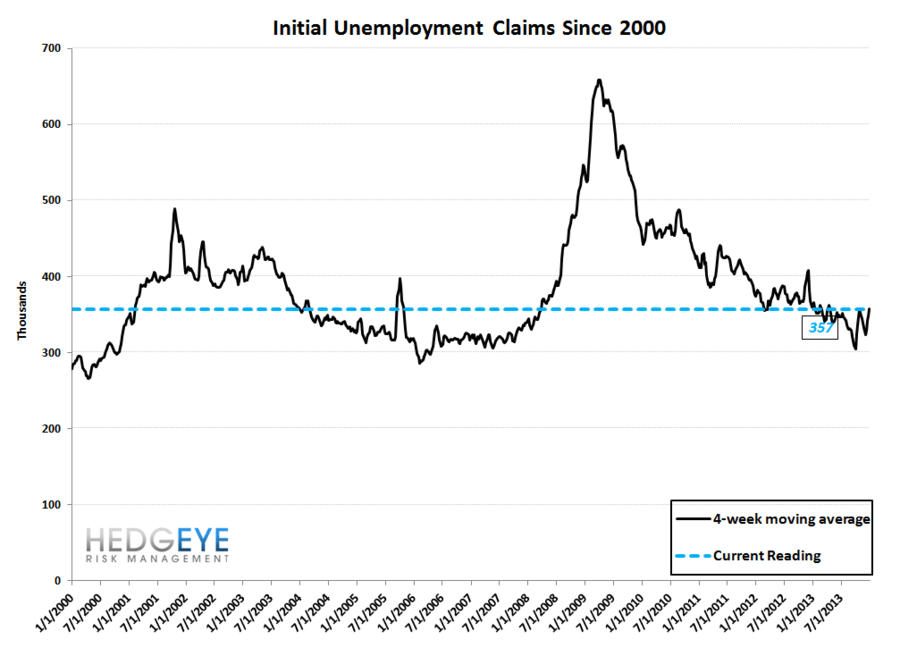

Prior to revision, initial jobless claims fell 1k to 339k from 338k week-over-week (WoW), as the prior week's number was revised up by 3k to 341k.

The headline (unrevised) number shows claims were lower by 2k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 9.75k WoW to 357.25k.

The 4-week rolling average of NSA claims, which we generally consider a more accurate representation of the underlying labor market trend, was -2.2% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -10.0%. However, as mentioned above, the distortions that have been present in the data up until just recently have rendered this 4-week rolling average slightly less valuable. We expect that in a few weeks it will again become the most important data point we track on the strength of the labor market.