This note was originally published at 8am on December 18, 2013 for Hedgeye subscribers.

“It will be said that we don’t propose to establish Kings.”

-Benjamin Franklin

“But there is a natural inclination in mankind to Kingly Government. It sometimes relieves them from the Aristocratic domination. They had rather have one tyrant than five hundred.” –Benjamin Franklin (The Liberty Amendments, pg 25)

I just love that quote. And how appropriate for a fresh winter’s morning when our central planning overlords are going to speak down to us from upon high. It’s Federal Reserve day, baby! Just like your Founding Fathers planned it.

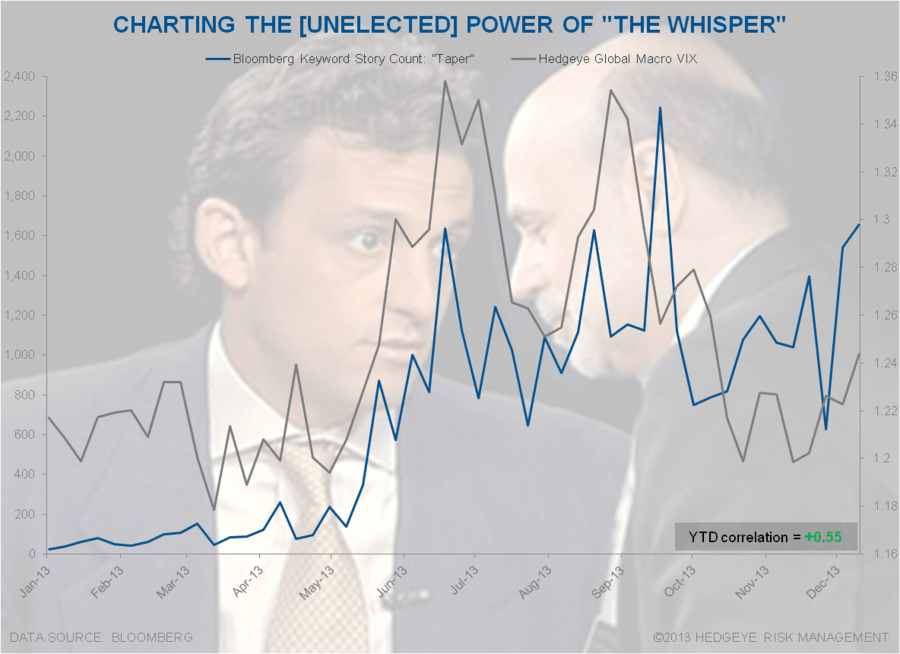

On tapering, our Kingly Government’s leaky-peaky-media-access-group seems a little confused as of late. Between the WSJ’s Hilsenrath and CNBC’s Liesman flip flopping on what the Fed is going to do today, at a bare minimum it makes for great TV, on mute.

Back to the Global Macro Grind…

Did King Bernanke cut these poor peons off? What is up with that by the way? Forcing these dudes to think for themselves during the holiday season is just mean.

In all seriousness, trying to front-run the Fed without inside information isn’t easy. Reading the tea leaves on what Mr. Macro Market expects in real-time is the best we can do. If Bernanke tapers today, he’ll certainly shock me. But that’s not new.

What is new is US equity market volatility. What’s driving an intermediate-term TREND breakout in front-month stock market volatility (VIX) above our 14.91 signaling line is very simple – monetary policy confusion.

And in markets (which trade on expectations, not academic theories), confusion breeds contempt. If you follow the bouncing ball of expectations:

1. MONETARY POLICY: what the Fed should have done in SEP (taper) wasn’t done, so confusion rules

2. CURRENCIES: confusion drives Global FX volatility; most markets are keying off what the US Dollar does

3. EQUITIES: since spoos like no-taper (but worry that there should be a taper) they whip around (on no volume)

One of our biggest subscribers (he runs $18B in equity assets) nailed it in an email to me yesterday. Effectively, he thinks he knows what to do, but he’s not sure – and he definitely doesn’t like the process of discovery:

“I need to take the pulse of the patient everyday and I would really like to take the pulse without a pacemaker attached!”

#Pacemakers. That’s what the Fed should get us Canadian catholic boys for Christmas – we can attach them to a Demark dongle on our Bloomberg machines and any time Hilsy or Liesman whispers another flip to their flopping Fed leaks, we get a little jolt.

In other news…

Economic data in the United Kingdom continues to improve at an accelerating rate. On the heels of a #StrongPound, strengthening purchasing power, and falling consumer prices, the UK unemployment rate just dropped to 7.4% from 7.6%.

This, of course, has the former Keynesian kings of the Bank of England all squirreled up.

After all, they cannot allow the only thing that perpetuates economic recoveries for sustainable periods of time (#StrongCurrency) to threaten their un-elected political power.

Or is that “threatening the recovery”?

I couldn’t make this up if I tried, but after one of the best British runs of positive (think rate of change) economic data since the early Thatcher years (oh did she #timespank those British Keynesian boys publicly!), this is the headline in Europe this morning:

“BOE WARNS FURTHER POUND APPRECIATION THREATENS THE RECOVERY”

All the while, the Swiss reported an awesome confidence reading for DEC (ZEW index 39.4 vs 31.6 in NOV) after the Germans did yesterday (Germany’s ZEW accelerated to 62 in DEC vs 54.6 NOV).

Damn that #StrongEuro!

How dare economic gravity take hold and the most coincident indicators of economic health (a country’s currency) perpetuate confidence amongst The People?

But there is a natural inclination amongst group-thinkers towards “certainty” in economic forecasting and policy making. It sometimes relieves people who are trying to cover their political bottoms because they don’t have to be accountable to the policies themselves.

They had rather have one central planning god than a free market.

Our immediate-term Risk Ranges are (my Top 12 Daily Macro Risk Ranges are its own product now):

VIX 14.30-17.08

USD 79.79-80.44

Pound 1.63-1.65

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer