This note was originally published at 8am on December 17, 2013 for Hedgeye subscribers.

“I can only say: I’m sorry America.”

-Andrew Huszar

In the opening sentence to his recent WSJ op-Ed (which the NY Times wouldn’t publish), “Confessions of a Quantitative Easer”, that’s what Andrew Huszar wrote. Since he ran the biggest Fed bond buying program in US history, that was a big apology.

I had the pleasure of hosting Andy at our new Hedgeye headquarters in Stamford, CT yesterday for our 1st segment of a series @HedgeyeTV that we’re calling Real Conversations.

The short-term headline of our conversation is that Andy doesn’t think the Fed tapers tomorrow. The longer-term implication of our conversation is that Andy thinks the Fed has been politicized, allowing “QE to become Wall Street’s new Too Big To Fail policy.” So don’t look for an actual “taper” of consequence, any time soon.

Back to the Global Macro Grind…

Not to be confused with Ben Bernanke’s take on the whole thing, Huszar left “Fed-up” because he didn’t believe in how “the central bank continues to spin QE as a tool for helping Main Street.”

Yesterday at the Federal Reserve’s 100 year birthday party (the one that no one in America cared to celebrate), Bernanke went on and on saying that the “Fed’s willingness, during its finest hours” … was to “stand up to political pressure.” Got-it.

Moving along… the entire global currency market, which has picked up some volatility as of late (JPM’s FX Volatility Index was +3.7% last wk to +8.1% YTD), awaits our central planning overlord’s decision tomorrow.

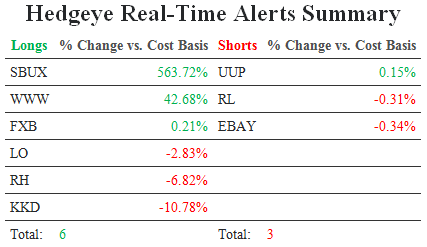

We’re short the US Dollar in our Q413 Global Macro Themes deck and we re-shorted the US Dollar (UUP) on its bounce to lower-highs last week in #RealTimeAlerts. Huszar’s take on it all simply confirmed what we were thinking.

From a risk signaling perspective, where do we stand on the FX War’s Big 3?

- US Dollar (Index) = Bearish Formation (bearish on all 3 of our core risk mgt durations – TRADE, TREND, and TAIL)

- The Euro (EUR/USD) = Bullish Formation (bullish on all 3 of our core risk management durations)

- Japanese Yen (USD/JPY) = Bearish Formation

The bearish intermediate-term TRENDs in both the US Dollar and Yen make sense as (relative to the ECB, whose balance sheet has shrunk) the Fed and BOJ have been the marginal debaucherers of their currencies as of late.

Japan has been doing this for over a year now, while the Fed re-engaged in Buck Burning with the no-taper decision in September. So that makes getting long the Yen versus the US Dollar here interesting. Warning: it’s early.

Looking at the leans in Global Macro consensus (net long or short positions in CFTC futures and options contracts), here’s where the game is currently at:

- USD = +6,730 net long contracts (versus +7,725 three months ago)

- EUR = +15,115 net long contracts (versus +39,803 three months ago)

- JPY = -129,614 net SHORT contracts (versus -90,060 three months ago)

In other words, consensus A) in US Dollar bulls isn’t as sure as it was 1yr ago (when the net long position in USD was +19,471), B) is more worried about another ECB rate cut (even though the European economic data continues to accelerate) and C) is wacky net short the Yen (now that it’s down -16% vs USD for 2013 YTD!).

So what do you do with that? Start yelling to the heavens that “it’s a bloody currency war and a race to burn everything; buy bitcoin!” Or do you buy Yen in early 2014 as consensus marks the bottom?

I’ll tell you how I used to think about stuff like this – dogmatically. I was certain that my research view was going to be right (until it would be very wrong) and had a complete disrespect for market timing.

Note to self (sponsored by Dan Och at OZM): if you disrespect Mr. Macro Market’s timing signals, he’s going to “do you” some humbling P&L exercises.

Our track record risk managing currencies is better than a moving monkey’s, primarily because we use risk controls:

- Buying a currency, I wait for an immediate-term TRADE oversold signal within a bullish TREND

- Shorting a currency, I wait for an immediate-term TRADE overbought signal within a bearish TREND

Those are the easiest calls to make. The toughest are the ones that eventually have the biggest TRENDING reversals (bearish to bullish reversals or vice versa). Buying the Yen versus the USD would be a potential example of that in early 2014. But, for me, I need to take my time and score the bottoming process (they are processes, not points).

In parallel to the quantitative signaling, what we do as a research team is try to play out scenarios and catalysts (preferably with tangible macro calendar catalysts). What if Huszar is right and the Fed’s Policy is To Big To Fail? What if the Fed doesn’t taper in DEC, then the US economic data continues to slow in JAN? What if you’re looking at no taper in 2014 and a Yellen Qe6?

If that were to play out, I’ll be really sorry for America too.

Our Financials team will be hosting a call on “Mortgage Mayhem” at 1pm today to discuss the coming January upheaval in the mortgage market from the new QM regulations. The speaker will be industry authority, Larry Platt, an attorney with the law firm of K&L Gates. If you’re an Institutional investor and would like access to the call, email sales@hedgeye.com.

Our immediate-term Global Macro Risk Ranges are now:

SPX 1765-1815

VIX 14.26-16.84

USD 79.79-80.44

EUR/USD 1.37-1.38

USD/JPY 101.72-103.84

Gold 1216-1255

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer