SUMMARY: KMP’s latest acquisition is supportive of our negative view on the Kinder Morgan complex……Kinder Morgan enters Jones Act shipping – a new industry for KMP, purchased from private equity, at a time of record dayrates. Shipping is highly-cyclical, it’s likely that KMP overpaid. Even with IDR forgiveness, we believe that the deal is dilutive to KMP in every year after properly accounting for replacement CapEx (which KMP will not do). Deal is modestly accretive to KMI in 2017, but at the expense of KMP dilution. Is this the best KMP can do with a $1 billion of capital?

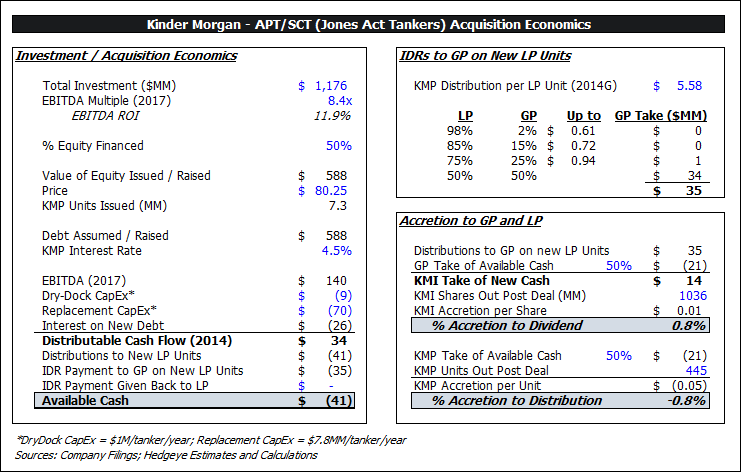

KMP enters Jones Act shipping trade with latest acquisition……On 12/23, Kinder Morgan Energy Partners (KMP) announced that it will acquire two shipping companies from Blackstone and Cerberus – American Petroleum Tankers (APT) and State Class Tankers (SCT) – for $962MM in cash plus an assumed capital expenditure obligation of $214MM, a total investment of $1,176MM. The acquired assets include five 330,000 bbl (50,000 dwt) Jones Act oil/product tankers that are currently operating, and an additional 4 tankers of the same size under construction/order. The 5 operating tankers are all new, with the oldest put into service in 2009. KMP estimates that the acquired assets will generate $55MM in EBITDA in 2014 and $140MM in EBITDA in the first full-year that all 9 ships are operating, 2017. We estimate that each new tanker costs ~$130MM, so Blackstone/Cerberus has already sunk ~$306MM into the four CST tankers under construction. Backing that unemployed capital out from the cash purchase price, we estimate simple deal economics of 11.9x 2014 EBITDA, 8.4x 2017 EBITDA, and 1.0x replacement cost. This is KMP’s first venture into shipping; the businesses will be housed in KMP’s “Terminals” segment, which is becoming somewhat of a misnomer now that KMP is sliding shipping and coal royalty businesses into the segment, similar to how KMP’s +40,000 bbl/d oil production operation is considered “CO2.”

History of APT/SCT……APT and SCT were born out of an 2006 joint venture between U.S. Shipping Partners L.P. (40%) and Blackstone/Cerberus (60%). The JV was to construct 9 new Jones Act product carriers at General Dynamic’s (GD) NASSCO shipyard for an estimated cost of $1.2 billion ($133MM/tanker), and then sell them to U.S. Shipping (100%) at specified prices. First delivery was scheduled for 2009. At the time, U.S. Shipping’s Jones Act fleet was aging and in need of replacement – the JV acted as a warehousing/financing vehicle to get this done. But the Jones Act market rolled over with the 2008 credit crisis and ensuing recession, and U.S. Shipping was unable to meet ongoing obligations, monetize assets, and finance the purchase of the new JV tankers; U.S. Shipping filed for bankruptcy protection in April 2009. U.S. Shipping released its stake in the JV in a July 2009 bankruptcy settlement, and Blackstone/Cerberus took 100% ownership of the newly-named American Petroleum Tankers (first five tankers) and State Class Tankers (next four tankers). Blackstone promptly employed Crowley Maritime Corp. (private) to manage the vessels (Crowley will continue to manage the vessels for KMP). In October 2013, after a stunning increase in Jones Act tanker rates and a red-hot MLP IPO market, Blackstone/Cerberus had an ideal exit opportunity and filed an S-1 for American Petroleum Tankers Partners L.P. Two months later, the IPO was pulled, and KMP acquired the companies.

Questionable timing for entrance into highly-cyclical biz……On 12/17/2013 Reuters reported that Exxon contracted a 337,000 bbl Jones Act tanker for a 6-month charter at a record $110,000/day. A week later, Kinder Morgan announced its entrance into Jones Act shipping with the purchase of APT and SCT. In our view, Kinder Morgan is entering a highly-cyclical industry in which it has no experience via a purchase from private equity just as popular media channels report on record-breaking profits. That strikes us as a risky investment – it’s likely that KMP overpaid.

Wide crude differentials (Brent – WTI, for example) in the US have created new arbitrage opportunities for moving crude oil from one US port to another, pulling capacity away from the traditional intra-US product routes like Gulf Coast-to-Florida and intra-West Coast. This sudden increase in demand for Jones Act vessels coupled with relatively inelastic supply (mainly due to a lack of quality US shipyards and 1-2 year lead times) has caused a spike in rates. Consequently, a tail risk that KMP is now exposed to, especially given the timing of the purchase, is a lift of the US crude oil export ban which would narrow US crude spreads; with new deliveries expected over the next few years, a narrowing of crude oil spreads would likely lead to excess capacity in the Jones Act trade. According to APT’s S-1,

“Despite these recent declines [in the number of Jones Act qualified tankers], the number of product tankers in the Jones Act fleet could begin to increase in 2015. Crowley Maritime Corporation and Aker Philadelphia Shipyard recently announced a joint venture to build four new product tankers to be delivered in 2015 and 2016, with an option to build up to four additional tankers in the future, and NASSCO has contracted with State Class Tankers to deliver the four State Class newbuild vessels in 2015 and 2016 and with Seabulk Tankers, Inc., a wholly-owned subsidiary of SEACOR Holdings Inc., to design and construct three 50,000 dwt product tankers to be delivered in 2016 and 2017, plus an option for one additional vessel.”

One shipbroker said recently that it’s the first time in 20 years that Jones Act shipping has been “clearly profitable.” We expect the industry to respond to that incentive in the way that competitive, cyclical industries do – build capacity. Interestingly, despite the current boom, Tom Crowley – Chairman, President, and CEO of Crowley Maritime Corp. (leading Jones Act shipper) – said this concerning returns on new Jones Act investment:

“The irony of this market is there are lots of people making the windfalls on investment in the energy itself. But as we look at the capital costs of building new tonnage, the investment isn’t being driven by a perceived windfall on the return. We are looking at modest returns on a three-to-five-year charter while essentially taking the risks on the long-term. We will remain subject to the state of the market as well. There are some operators with older vessels that are getting good returns, but new investment needs to be tempered because it is fully loaded with capital costs and operational risk.”

Crowley may be alluding to the fact that a 50,000 dwt newbuild Jones Act tanker (made in the USA) cost ~$130MM. But according to international shipbroker Simpson Spence & Young, a double-hull tanker of similar size (“Handymax”) constructed in Japan costs only ~$45MM! One built in South Korea or China is likely even cheaper.

KMP's economics are largely locked-in through 2015/6, when its initial 5-year time charters are up for option or renewal. But these tankers are long-lived assets (30 years), and whether or not this acquisition destroyed or created value for KMP unitholders will not be known for many years. We note, though, that KMP did not leave much room for error buying into record rates.

Of course, no replacement CapEx……The “genius” (it’s really not that smart, and it’s another obvious example of an aggressive maintenance CapEx policy, much like in KMP’s E&P operation) of this deal for Kinder Morgan is in the financial engineering on the replacement/maintenance CapEx line. A tanker requires large upfront construction CapEx but very little additional capital over a fairly-predictable useful life. After 30 years of sitting in saltwater, the hull rusts out and the tanker is scrapped and replaced with a new ship. Depreciation does a decent job of accounting for this, though it will understate the nominal cost of replacing the ship unless we have 30 years of deflation. It is common among shipping MLPs (and other MLPs with “depleting” assets) to reserve for “replacement CapEx” such that DCF is more indicative of terminal free cash flows, though KMP will not do this, as far as we understand it. APT’s S-1 listed annual replacement CapEx for 5 tankers at $11.5MM, or $2.3MM/tanker. This seems very aggressive given that it is depreciating $130MM tankers at ~$4.3MM/year (nominal salvage value of $1.5MM). If we assume 2.0% annual inflation, a $130MM ship with $1.5MM of salvage value (today’s dollars) will cost $233MM to replace (net of the inflated salvage value) in 30 years. Straight-lining that amount gives us annual replacement CapEx of $7.8MM/tanker. In 2017 when KMP has 9 tankers in operation, that would equate to ~$70MM of annual replacement CapEx. KMP will not include this reserve, which it can get away with for the next 25 – 30 years. Regardless, it’s another example of how KMP’s “DCF” overstates its true profitability.

Deal math: dilutive to KMP, barely accretive to KMI……With the allocation of replacement CapEx as described above, the deal is dilutive to KMP in all years out to 2017, and is 0.8% accretive to KMI in 2017. If we (inappropriately) set replacement CapEx to $0 (as KMP will do), the deal is only 0.6% accretive to KMP’s guided 2014 distribution of $5.58/unit and 2.8% accretive to KMI’s guided 2014 dividend of $1.72/share, in 2017.

Another way to analyze the deal economics (irrespective of KMP's distribution)......The investment will generate $34MM of recurring FCF in 2017. Given the 50/50 IDR split, we give $17MM to KMI and $17MM to KMP. We estimate that the KMP equity investment will be $547MM (50% equity financing net of $41MM of aggregate IDR forgiveness), giving KMP a 3.1% ROE in 2017.

Kevin Kaiser

Managing Director