We are pleased to highlight three market research notes below from Hedgeye analysts which shed light on current market dynamics, as well as two deep dives into two stocks which have received considerable investor attention recently. In addition, this week's Macro Note by Hedgeye Managing Director Moshe Silver offers a distilled look back over the past year and what we might anticipate in 2014. Finally, at the conclusion of this week's Investing Ideas, we offer a replay of our analysts' latest takes on their respective high-conviction stock ideas.

Please click on the titles below to unlock the institutional research notes.

Worst Bond Outflow in Over 3 Months

The Hedgeye Financials team highlights the ramifications of the latest ICI Fund Flow Survey which showed the worst bond market outflow since August. Fixed income mutual funds continued persistent outflows with $8.1B withdrawn from bond funds last week, while the combination of equity ETFs and funds had strong inflow. At the peak of Bernanke's Bond Bubble in 2012, average weekly flows were +$5.8B average inflow per week. Last week's -$8.1B outflow from bonds takes the year-to-date weekly average outflow to -$1.4B per week. Unsurprisingly, the yield on the 10-Year Treasury finished the week north of 3%.

Darden Restaurants (DRI): A Half-Baked Plan

The writing has been on the wall for quite some time that DRI needs to make significant changes to the operating structure of the company. We didn’t believe its CEO would pull the trigger this quarter. In fact, we didn’t think he would ever do it. We were wrong. However, the plan stops well short of what really needs to be done.

Caterpillar (CAT): Party Likes It's 1979?

If you are long CAT looking for a long-term bottom, history suggests that 2017 or later might be a better time to check back. Commodity prices have stalled, we think, for the foreseeable future, and the resources capital equipment cycle has turned down. If you are long CAT shares for a trade based on seasonality, a restructuring plan or 4Q results, it might work but we would be careful not to overstay. If history rhymes, long-term holders will not be able to wait the down-cycle out.

Macro Highlights (and Lowlights) of 2013

January – Hedgeye ushered in the new year with our Q1 Macro Themes call. Our Big Three themes for the start of the year were

#GrowthStabilizing,

#HousingsHammer, and

#QuadrillYen.

A strengthening dollar, combined with improving labor market trends, signaled that Bernanke’s target – 6% unemployment – could be within reach. At the same time, Financials sector head Josh Steiner said the housing market could “go parabolic” – which, in fact, it proceeded to do in the following months.

On the other side of the globe, Japan’s “Abenomics” opened the floodgate on the Yen, sending Japan’s equities markets up, up, and away in their own version of Bernank-o-mania. With central bankers across the globe rushing to burn their currencies at the stake, it was going to be one heck of a year.

February

Financials sector head Josh Steiner reported that home prices were hitting levels not seen since 2004-2006 (before the financial crisis – we offer this clarification as a service for Wall Street professionals and Washington policy makers, who can’t remember that far back.) Housing sector stock prices had yet to catch up to Steiner’s “parabolic” call, meaning there remained room for growth – and profits.

Like Washington policy makers, Wall Street analysts look at broad housing market statistics, where the distressed segment exerts a powerful drag on growth figures. If you measure the wrong thing, you come to the wrong conclusion. We leave it to our readers to decide whether this is worse when it happens on Wall Street, or in Washington, where measuring the wrong things leads to disastrous policy decisions. Steiner said the effect of the distressed segment had largely been flushed out of the sector, but stock prices were still waiting for investors to wake up and smell the housing recovery coffee.

March

We got to brag a little, as two of our Q1 Macro Themes played out well on schedule. Before the quarter drew to a close, the rest of the investing world started catching up to #HousingsHammer and #GrowthStabilizing.

March also saw three key data points:

Sequester Madness – The Sequester forced fiscal responsibility on Congress, something no one in Washington had the guts to push for.

Jobs – Speaking of Measuring The Wrong Thing, the government and most of Wall Street follow seasonally adjusted employment / unemployment data. And note that em-ployment data and un-employment data do not measure the same thing to begin with. Financial sector head Josh Steiner tracks Non-Seasonally Adjusted (NSA) numbers – the raw data is a more accurate representation of actual strength in the labor market. By March, unemployment continued trending lower at an accelerating rate, signaling growing strength in the labor markets. Meanwhile the government’s Seasonally Adjust figures were lining up to make year-over-year comparisons look far worse than the actual employment picture. From this you make economic policy?!

Commodities – Gold started the year around $1,700 and was trending down by March. (By Christmas it was around $1,200.) In March oil was trending lower too. Off a national average high price of $3.74 a gallon, gas prices made a series of lower highs and averaged around $3.26 by Christmas. It is estimated that a one-cent decline in the price of gasoline literally “pumps” one billion dollars into the US economy. Nearly half a dollar decline from the year’s high – that’s what we call a tax cut!

April

Hedgeye’s Q2 2013 Macro Themes call featured:

#StrongDollar,

#GrowthAccelerating, and

#EmeregingOutflows.

The Dollar continued reversing a generational slide, giving us the opportunity to rag on the gold bugs. Hedgeye had bragging rights, having been bearish on the yellow metal for over a year.

Growth showed up in a number of key sectors, including declining unemployment and strength in the housing market. Health Care sector head Tom Tobin produced a proprietary survey indicating the US could be on the verge of a statistically significant upturn in the birth rate, reversing a forty-year decline and leading to a boost in new household formation. This looked potentially long-term massive for anything consumer related.

Meanwhile, global economies were weakening. In particular, the BRICs were BROKEN, and even “stable” countries like Turkey were feeling a frisson of unrest (fast forward to Christmas week if you want to see how that call played out.) The US, for all the uncertainty in its markets, remained the safe haven.

This was particularly damaging for gold, which had become so popular that it lost its “Haven Asset” status. Haven Assets don’t behave like other assets. In Wall Street jargon, they are “uncorrelated.” Investors afraid of the stock and bond markets traditionally fled to the shelter of gold and silver. In the past decade, so many investors bought so much gold – and so much more was sucked directly into the stock market in the form of various gold ETFs – that the “Haven Asset” now trades like a stock. Not only is gold no longer a Haven Asset, it’s not clear what it is.

May

This was the May the earth stood still, as Washington tweaked America’s economic calculations.

US Macro analyst Christian Drake unpacked the Bureau of Labor Statistics’ switch to “Chained CPI” calculation for consumer inflation. “Chaining” assumes consumers rationally substitute goods in response to rising prices. If beef prices rise, Chained CPI assumes consumers will buy chicken, soy, and canned tuna fish. The trade-off between a fixed amount of money and an equivalent caloric and protein intake is economically efficient, and the transition takes place smoothly and predictably within an identified population group and provides an acceptable substitute.

That’s if you believe human beings are Rational, Efficient Decision Makers (classical economic theory). But maybe you believe human beings make decisions based on partial information, driven by fear and by the desire to avoid pain in the moment, without reflecting on future consequences (the way real people actually operate). The AARP wrote that the effect would be, not a shift from filet mignon to chicken Kiev, but to tins of cat food.

Chained CPI also tends to report slightly lower inflation than current measures, meaning cost of living adjustments for retirees could decline each year by about $3 for every $1000. Three dollars makes a difference if that $1000 is all you have to live on. After a few years, the cat food scenario looks frighteningly believable.

Meanwhile, the Bureau of Economic Analysis was “essentially rewriting economic history,” in the words of national accounts manager Brent Moulton. It was not reported whether he said that with a sense of shock, or of pride. The BEA, just added some new components to the measure of GDP – the value of goods and services produced in the US – which now includes R&D expenditures, and motion pictures, books and recordings, as well as certain “long-lasting” television programs.

This revision was estimated to add around half a trillion dollars to the US economy – the equivalent of Belgium, as the Financial Times wonderingly wrote. The BEA said they would restate the national accounts going back to 1929. It was not clear whether this meant that, in retrospect, the Great Depression never actually happened.

Said Drake, “any metric in which GDP is the denominator (Debt/GDP, etc) goes down” which has policy implications. With the stroke of a No. 2 pencil the nation got oodles richer, magically mitigating the impact of excess debt.

June

So why didn’t things get better? By June, legendary investor Bill Gross of PIMCO said the global central bank mania couldn’t last and told investors to get out. Out of bonds, out of stocks. Out of everything.

Fed chairman Bernanke murmured that it may be time to consider letting a little air out of the balloon, and all hell broke loose across the financial markets as people contemplated having to get out of their bond portfolios – including PIMCO’s own $300 billion.

Acting in its role as lender of last resort, the Fed’s balance sheet had grown. The Fed’s own website reported “Total assets of the Federal Reserve have increased significantly from $869 billion on August 8, 2001, to well over $2 trillion.” That was June. Today the number stands at $4 trillion.

Market volatility went on a tear, with pundits expecting the turbulence to run into Q1 of 2014 in the face of Fed uncertainty.

Across the financial media, the shrieking heads were jabbering that “risk is on!” To which Hedgeye CEO McCullough responded “Risk is always on.”

Hedgeye remained firmly bullish on US economic growth. This is not the same as being bullish on the stock market – it’s easy to miss the distinction with the indexes at all-time highs. The Fear Factor is so overpowering that people lose sight of the longer term. Highs are made in the markets when Greed overpowers Fear. When Fear is in the ascendant, markets make lows.

And when the Market Manipulator of Last Resort enters the game, the most predictable effect is to increase volatility by accelerating economic cycles and trying to stave off the inevitable effect of interest rate moves on prices. In other words, Bernanke’s interventions mess with Time, and the Force of Gravity. We wonder what Einstein would say…?

Responding to Fed Chairman Bernanke’s calm professorial demeanor as he sought to assuage the global financial community, PIMCO’s Gross observed “Perhaps financial markets and real economic growth are more at risk than your calm demeanor would convey.”

Touche, Mr. Gross – for all the good it did you.

July

Hedgeye’s Q3 2013 Macro Themes call featured:

#RatesRising,

#DebtDeflation, and

#AsianContagion

The dollar continued to strengthen, while US housing, employment and consumption all surprised to the upside. The slope of the line was definitely confirming Hedgeye’s #GrowthAccelerating theme. On top of this, interest rates were on the rise, making the dreaded Fed taper look like an ineffectual policy tool.

Interest rates were starting to reverse a long, slow decline that had prevailed for over a generation. Imperceptible as individual data points, the slope of the line was definitely moving higher. Like the Queen Mary, interest rates were turning ponderously, almost imperceptibly. But the trend was, in fact, reversing course.

Keith went out on a Macro limb and said we are not likely to see the 2012 lows on ten-year bond yields – not soon, and maybe not ever. (As we head into 2014, the ten-year Treasury yield traded over 3%, a two-year high.) Longer-term historical rates average over 6%; that’s over four full percentage points for rates to reflate as the 40-year bonds bubble pops without entering the historical Danger Zone for inflation. As we come into year-end, Hedgeye still expects the bond bubble to continue to melt, and Financials sector analyst Jonathan Casteleyn reports the generational rotation out of bond funds and into equities marches on apace.

August

Hedgeye announced: “Fed Chairman Bernanke will begin the process of tapering the Fed’s $85 billion a month bond buying program next month. Or he won’t.”

In the event, we were right.

Director of Research Daryl Jones wrote “there is rarely One Thing that dominates, but the seismic shift in interest rates will certainly be one of the most critical factors over the coming quarters and years.” Hedgeye’s #RatesRising theme and our #DebtDeflation call were working their way through a major supply / demand imbalance in the investment markets. The world was sitting atop a historically wide divergence between investments in stocks (about 1/3 of global investment dollars) versus bonds (the rest). The ratio was further skewed by the attractiveness of the US equities markets – which is where everyone still wants to be.

Playing that equities market, particularly in times of uncertainty created by government policy meddling, requires a risk management process. Rather than deal with the moment-to-moment nature of the market, traders had adopted a simplified model called “Risk On / Risk Off.” As we wrote, it was so simple that even a major news network anchor can understand it.

Risk is “On” when investors are bullish on the direction of the market and want to go along for the ride. They trade instruments that are correlated to broad market averages, such as call options on the SPY (S&P 500 index). This would be a “Risk On” trade, where the buyer expects to sell the option for a profit, after the market rises. In the global currencies markets, the concept applies to more volatile currencies. When Risk is “Off” in the global markets, investors move to more staid currencies, notably the US dollar, the Swiss franc and the Japanese yen. They used to flee to Haven Assets like Gold and commodities – but those havens aren’t so safe any more.

Sounds simple: you like the prospects of the overall market, get your Risk On. Don’t like it? Get Risk Off – like going to 100% cash, perhaps the ultimate Risk Off trade.

The problem with this binary model is, not only does it not work all the time, it may not really work ever. Or: it generally works right up to the moment when you really need it to work. And when it fails, it fails big time. As Hedgeye CEO Keith McCullough observes, “risk is always on.”

As Jones pointed out, by June the bond market looked set to deliver a painful second blow to a large number of investors, for all their risk management tools. (June, unanticipated and painful, was the “one” of the “one-two punch.”) To give you an idea of just how fast extremes are reached in the financial markets, bond volatility had doubled in the second quarter alone and was reaching two-year highs. Hedgeye senior Financials sector analyst Jonathan Casteleyn reviewed current bond duration measures and found that a one-percent rise in interest rates in mid-August would result in a nearly 9% drop in the price of the 10-year Treasury bond – a world of hurt for fixed income investors.

September

It was Back To School for Hedgeye as we had to take our #AsianContagion theme into the shop for a tune-up.

Senior Macro analyst and China watcher Darius Dale said significant new political news developments indicated “we should not be short China right now.” We admit that we had to change course on China – as Keynes famously said, “When the facts change, I change my mind.” Of course, the lift in the Chinese markets brought out a sudden emergence of China bulls – or perhaps better put, an emergence of sudden China bulls. Nothing like a short-term market reversal to have people switching hats and sneering “I told you so!”

Amidst market spikes and cash inflows, Dale called the political news “the only positive data point that actually matters” as the Politburo signaled meaningful financial reform measures with global implications. Dale wrote that the Politburo announcement signals a take-the-Chinese-bull-by-the-horns approach that could wrench the economy to its feet. “Unlike Western politicians,” noted Dale, “the Chinese do not speak very often. And when they do, they invariably carry through on what they say they’re going to do.”

October

Just when we were getting used to Congress doing nothing at all, they decided to Do Nothing in a really big way. By Doing Nothing about the nation’s debt issuance, the brought the US, if not to the brink of actual default, at least to a place where the fetid hot breath of the specter of default burned in our nostrils and caught nauseously in our throats. Hedgeye’s McCullough renewed his call to hold Washington nincompoops of all political stripes to account for the rank fear-mongering that is the order of the day across the spectrum. But Fed-Fed jaw-jaw notwithstanding, the growth style factors in Hedgeye’s Macro model barely corrected. Measured year-to-date, growth stock were up over 32%; the top 25% EPS growth companies in the S&P 500 were up 28%; the top sales revenues growth stocks were up 27%, and high short interest stocks, high beta stocks, and the small cap group were all up over 25%.

Clearly, the Fear Mongers still had work to do. Testifying before Congress, Treasury Secretary Jack Lew, used the words “default,” “catastrophic,” “very dangerous,” and the “real risk of a financial crisis and recession that could echo the events of 2008 or worse,” all within the space of about three minutes.

But wait a minute, said McCullough: politicians don’t tell us when there’s a crisis in the markets. The markets tell us when there’s a crisis in the markets. And as of mid-October, market risk indicators were not signaling a crisis.

Spreads on the US CDS widened a bit, but were nowhere near what market wags call the “Lehman Line” and, in fact, remained low compared to the past few years. The real risk associated with the October 17th “Drop Dead” date turned out to be reputational. No one, it seems, understood this better than Florida congressman Alan Grayson who angered House Speaker pro tem by reading into the record a national survey that found Congress was less popular than hemorrhoids, toenail fungus, and dog poop.

You can’t make this stuff up.

November

The Federal Reserve turns one hundred years old next month and looks set to mark its anniversary by delivering much, much more of the same. Congress rants about the politicization of the Fed, but it’s equally clear that Washington has abdicated its responsibilities, leaving a void that permits – nay, forces – the Fed to take control. Legislators and presidents alike have been happy to hand off the hot potato of economic policy to unelected academics, freeing themselves to get back to the basic business of sucking up to powerful constituents, while in turn encouraging wealthy lobbyists to suck up to them.

November brought two articles by recent Fed insiders. In Foreign Affairs magazine, Alan Greenspan explained “Why I Didn’t See the Crisis Coming.” Though he recognized that human decision making is driven by irrational factors, Greenspan said “For decades, most economists, including me, had concluded that irrational factors could not fit into any reliable method of forecasting.” Translation: The world’s most powerful central banker knew that he was missing a huge body of data that impacts economic decision making, but didn’t incorporate it in his calculations because (a) it’s really hard to measure, and (b) no one else measures it anyway.

In retrospect, Mr. Greenspan believes that “people, especially during periods of severe economic stress, act in ways that are more predictable than economists have traditionally understood.” In other words: “If I had it to do over again, I would do things really differently.” This is actually to Greenspan’s credit. King Solomon the Wise had it right: most people never learn from their mistakes. Much good may Greenspan’s after-the-fact enlightenment do us now…

More widely read was a Wall Street Journal Opinion piece by Andrew Huszar, the executive at the New York Fed who was placed in charge of the “a wild attempt to buy $1.25 trillion in mortgage bonds in 12 months.”

In December, Huszar joined Hedgeye’s McCullough in an exclusive and extended Hedgeye TV dialogue. Spoiler alert: both Huszar and McCullough predict that Bernanke will not taper before year end. Even smart people can be wrong on an individual data point.

That’s why we follow trends: one data point does not a long-term trend shift make, and there will be plenty of time to determine the effects of reduced bond buying by the Fed – assuming, that is, it stays reduced.

December

All right, so he did taper. If you call that a “taper.”

“I was dead wrong on the no-taper call yesterday,” wrote McCullough on the Morning After. Still, as we wind down 2013, McCullough’s Real-Time Alerts virtual positions are ending the year positioned right, overwhelmingly long the surging market. “Where I was brought up,” wrote Keith, “being right for the wrong reasons is called luck.”

The mini-Taper doesn’t change our fundamental process. Our Macro process basically takes us back to where we were positioned from December 2012 through September of this year: Long Growth (Equities) and Short Gold, Bonds, and Equities that look like Bonds, such as MLPs, Utilities, and other high-dividend payers.

The Taper points – or perhaps cries “uncle!” – to an environment of rising interest rates and indicates that the Dollar is not likely to go down in flames. This mix is bad for Gold, and bad for Bonds. Hedgeye’s Macro work indicates fund flows out of Gold and out of fixed income – and into US growth stocks – should dominate well into the new year, especially if there’s any follow-through in Fed hawkishness.

We thank our subscribers for a great year. We thank our Twitter followers for your follows, your praise – and for your criticism. You may not realize it, but we really do go home at the end of every long day and try to figure out how we got so many things wrong. We like to think that’s the mechanism that helps us get so many things right.

Wishing you a happy holiday season and a prosperous 2014.

Onward and upward!

- By Moshe Silver

Moshe is a Hedgeye Managing Director and author of the Hedgeye e-book Fixing A Broken Wall Street

Investing Ideas Updates

Editor's note: We are giving our sector heads the holiday off. Here's a replay of their latest takes on their respective high-conviction stock ideas from 12/20.

CCL – We are happy to report that it was a wonderful week for Carnival shareholders. The stock surged 8%.

We have increased our 2014 FY EPS from $1.65 to a likely Street high $1.90 on the back of significant cost cutting. Not surprisingly, our net yield (constant-currency) projection declines from +1.4% to +0.3%, due to continued Caribbean uncertainty and adverse FX impact.

Lower yield guidance was expected but the cost outlook was indeed a pleasant and major surprise. The management reorganization paid dividends much sooner than expected. Already, new management is driving cost synergies and efficiencies in the fuel, operations, and procurement areas under new CEO Arnold Donald.

FXB – Being bullish on the British Pound versus the US Dollar remains one of Hedgeye’s favored macro themes in Q4. The position is supported over the intermediate term TREND by prudent management of interest rate policy from Mark Carney at the BOE (oriented towards hiking rather than cutting as conditions improve) and the Bank maintaining its existing asset purchase program (QE).

Meanwhile, data out this week confirms the underlying performance of the economy which we believe will translate to currency strength: Q3 Final GDP was revised up to 1.9% Y/Y vs an initial estimate of 1.5%; CPI dropped to 2.1% Nov. Y/Y vs 2.2% Oct. (reducing the consumption tax); and Retail Sales were up 2% in Nov. Y/Y vs 1.8% Oct. Over the immediate term TRADE we expect the USD to strengthen on Bernanke’s “unexpected” decision to taper this week, and an above-consensus Q3 U.S. GDP print, however over the medium term we expect the uber dove Yellen to issue weak USD policy.

FDX – FedEx reported its fiscal second quarter results, missing expectations because of a late start to the Christmas shopping season. Management raised full year guidance, showing confidence that it will recoup that volume in FY3Q. Critically, FedEx Express generated solid YoY margin expansion, a likely reason the shares have remained strong following the report. We continue to see upside for FDX shares as the company shows investors the profit potential of the Express segment.

We added FDX to Investing Ideas on 3/29/13. Our thesis centered on the potential for the Express division to be made significantly more profitable. At the time, FedEx Express was 'free' in our valuation, presenting an attractive risk/reward. After a 45% rally in FDX shares since then (compared to 16% for the S&P 500), we still think FedEx Express has some additional value to be recognized by the market. Importantly, we now have some evidence that they are making progress - albeit slow.

GHL – Greenhill & Company announced a good sized advisory mandate during the week, winning a $2 billion mandate to advise AT&T in the sale of its wireless assets in the state of Connecticut. This was the largest advisory win for GHL since October. The company also put up two other additional mandate wins during the most recent 5 day period for a total of 3 new deals won this week, the most active week of new deal mandates for the firm since September.

GHL shares are Senior Financials sector analyst Jonathan Casteleyn’s favorite way to invest in a cyclical uptick in the mergers and acquisition market (M&A) which has been dormant for the past 3 years. Says Casteleyn, “M&A activity has historically benefited in an environment with higher interest rates – which may have started with the Fed now starting to back off of the fixed income curve – as corporations focus less on dividends and buybacks, and more on strategic M&A activity to reward shareholders.”

HCA – Holy $#&*@! Admissions stink! Or so says Citi's Hospital analyst quoting a recent survey of hospitals. Apparently volumes are the "weakest ever." Not to poo-poo Citi's survey, but there are a few things to consider before flushing HCA. Q412 has some very difficult comparisons for volumes including the one of the "worst ever" flu seasons and the only quarter of the last 6 years to see a positive year over year change in maternity volume. Both of these cases come with extremely low margins, and possibly negative margins in some cases. We recently did an analysis of what is an important driver of hospital profitability, names US Orthopedic surgery, the largest revenue driver for hospitals, a trend that looks likely to continue accelerating.

MD – MD finally got around to making another acquisition today. While they won't meet their guidance for deal flow with the deal in Q413, we continue to expect more deal announced in the coming weeks, offering some catch up in revenues in the next few quarters.

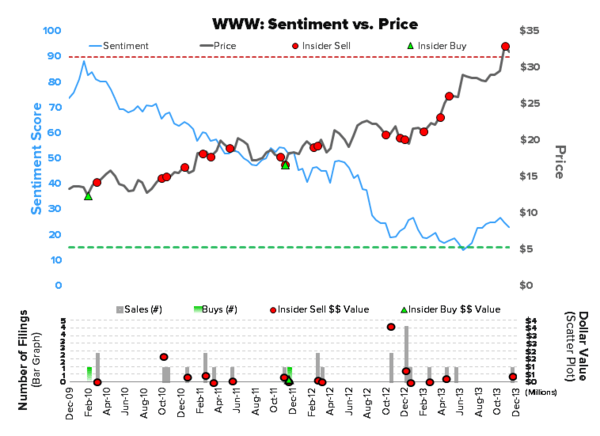

RH and WWW

Below we take a detailed look at sentiment for our two retail investing ideas. The primary tool we use is our Hedgeye Sentiment Monitor. What it does is uses a quantitative scale to combine Sell-Side Ratings, Buy Side Short Interest, and Insider Trading activity. We pretty much catch all angles.

We use this tool in two different ways; 1) First, we look at directional changes in sentiment for each stock. 2) Second, we analyze the absolute level for each security. A reading above 90 has statistically proven to signal that the market is overly bearish on a name, and that it’s often advantageous to go the other way. Conversely, a reading below 10 suggests that the market is overly bearish, at which time it is usually prudent to go long.

RH – For Restoration Hardware, even though we only have only 14 months worth of data, we see that the sentiment reading is near its all-time low. No doubt the recent management shake-up contributed, but even before then, people were finding every reason they could to be bearish. We continue to view RH as the name in retail with the greatest upside. Currently at $67, we thing that RH will touch $200 over 3-years.

WWW – With Wolverine World Wide, the sentiment chart is much more clear cut. Simply put, everyone hates it! Sentiment has been drifting lower and lower, and occasionally touches the 10x mark (that’s when people are way too bearish – no Buy ratings, high short interest). While not the same expected percent gain as RH, we’re still looking for WWW to go from $32 to $55. Not half bad.

TROW – T. Rowe Price shares had a strong week with the Fed’s tapering and acknowledgement of an incrementally improving U.S. economy. Senior Financials sector analyst Jonathan Casteleyn says “with the U.S. central bank now signaling that it will be adding less liquidity to fixed income markets, which could eventually lead to short term interest rates rising over time, it is valuable to understand that equities have drastically outperformed bonds in past rate raising cycles.” (See chart below). As the country’s leading equity asset management firm, Casteleyn says TROW shares will start to discount this potential forward opportunity for equities versus bonds in the United States with the new Fed signaling of smaller subsidies for fixed income. This positively disposes TROW shares for a good start to 2014. Separately, Casteleyn spoke to TROW management this week and says “all our checks for a solid 4th quarter earnings print are in line in late January.”