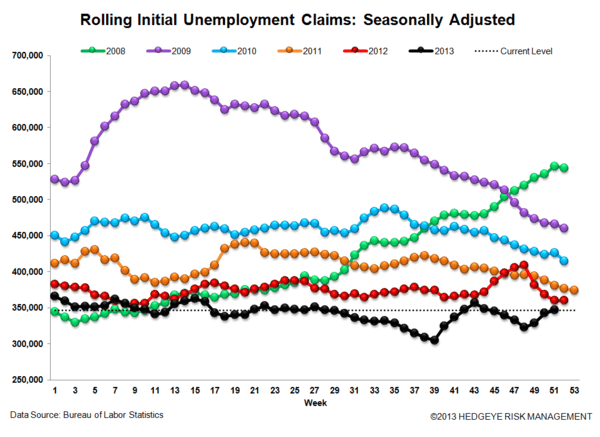

The seasonal, peri-holiday noise will remain in the initial claims data through the end of the year, but after last week’s “speed bump”, this morning’s release, which showed non-seasonally adjusted claims improving 9% YoY, reflected a return to the positive TREND rate of improvement that has characterized much of 2013.

Confidence, meanwhile, continues to recover from the government shutdown catalyzed rollover in Oct/Nov. Bloomberg’s weekly read on consumer comfort improved +2.0 to -27.4 week-over-week and continues to track back towards the August highs.

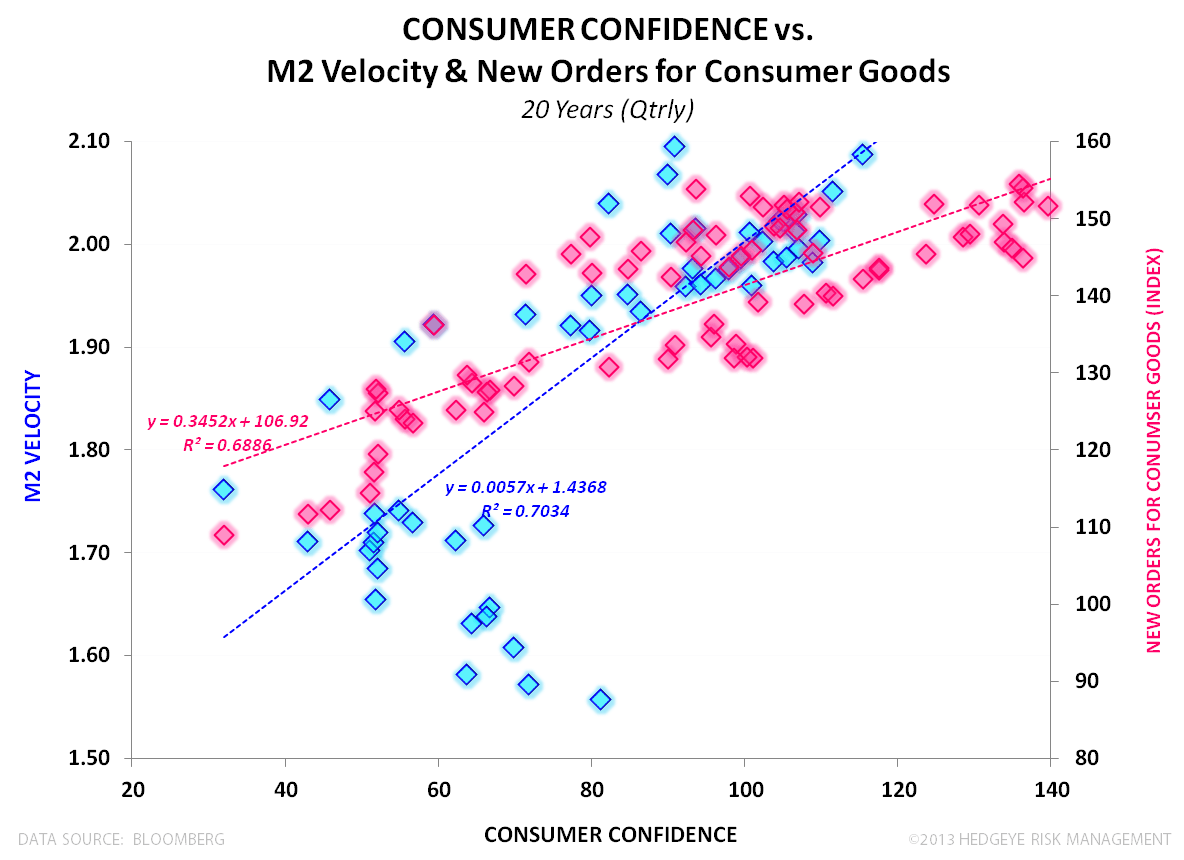

More broadly, after treading water for nearly 5 years, confidence readings across all the major survey’s have seen a legitimate breakout in 2013 alongside accelerating economic growth and ongoing improvements in the housing and labor markets.

Historically, Confidence has been a solid coincident-to-leading indicator for broader economic activity. For example, over the last 20 years, the correlations between Consumer Confidence and Velocity of M2 and New Orders for Consumer Goods are >0.82. Not a surprise for a consumer driven domestic economy, but worth a re-highlight as confidence breaks back towards pre-recession levels.

Below is the breakdown of this morning's claims data from the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

- HEDGEYE MACRO

----------------------------------------------------------------------------------------------------------------------

INITIAL CLAIMS: 2013 in Review

With all but one week of 2013 now in the books the labor data is showing a non-seasonally adjusted year-over-year improvement of 8.2% on a full-year basis. For comparison, 2012 was better by 8.1% versus 2011. This morning's data point showed a 9.0% improvement y/y while the rolling 4-wk average is better by 10.2%. By most accounts the labor data remains strong and shows ongoing improvement. Last week we had flagged a speed bump in the data, but this morning's numbers suggest that a speed bump may have been all that it was.

We continue to expect that the strengthening labor market data will exert ongoing upward pressure on long-term rates. This morning the 10-year treasury yield is at 2.99%, just one basis point away from its September 5 high. We've demonstrated how bank stocks are very positively correlated to 10-year yields while homebuilders are very negatively correlated. For more on that, see our publication from 11/22/13 entitled #Rates-Rising: A Current Look at Rate Sensitivity Across Financials.

The Data

Prior to revision, initial jobless claims fell 41k to 338k from 379k WoW, as the prior week's number was revised up by 1k to 380k.

The headline (unrevised) number shows claims were lower by 42k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 4.25k WoW to 346.75k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -10.2% lower YoY, which is a sequential improvement versus the previous week's YoY change of -7.7%

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT