TODAY’S S&P 500 SET-UP – December 26, 2013

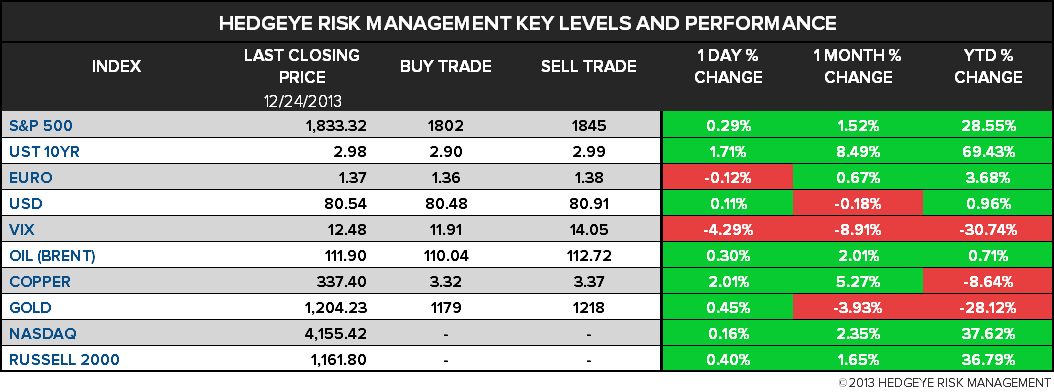

As we look at today's setup for the S&P 500, the range is 43 points or 1.71% downside to 1802 and 0.64% upside to 1845.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.58 from 2.58

- VIX closed at 12.48 1 day percent change of -4.29%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Jobless Claims, Dec. 21 (prior 379k), est. 345k

- 9:45am: Bloomberg Consumer Comfort, Dec. 22 (prior -29.4)

- 10am: Freddie Mac mortgage rate survey

GOVERNMENT:

- Senate out of session until Jan. 6; House returns Jan. 7

- President Obama, First Family on vacation in Hawaii

WHAT TO WATCH:

- UPS misses some Christmas deliveries; AMZN offers refunds

- Turkey’s Erdogan overhauls cabinet amid graft probe

- Target seen losing customer loyalty after credit-card breach

- BlackBerry founder Lazaridis walks away from possible deal

- Volcker Rule challenged in U.S. court by bank industry group

- U.S. Postal Service wins temporary 6% rate increase request

- Apollo said to win approval to lift fund limit to $17.5b

- Alibaba unit wins license to compete in China wireless mkt

- Japan banking regulator seeks authority over Tibor rate

- Softbank to raise funds for T-Mobile deal in U.S.: Nikkei

- Abe draws China ire w/ visit to Japan’s Yasukuni war shrine

- Batista cedes control of OGX oil co. in $5.8b debt deal

- NOTE: Most European, Canada equities mkts closed today

EARNINGS:

- No earnings expected

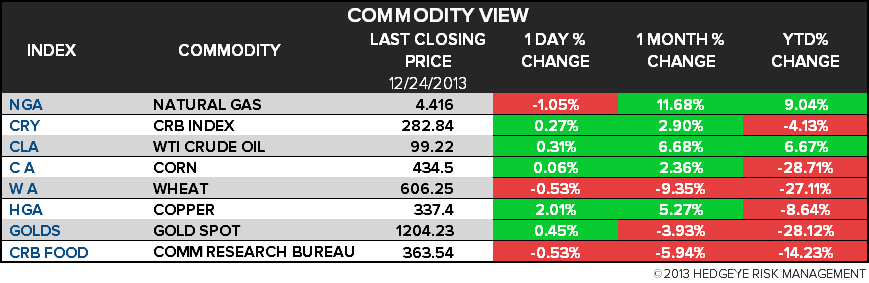

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Platinum Climbs to One-Week High as Gold Holds Above $1,200

- Copper Gains as Economic Growth May Lift Industrial Metal Demand

- Bug Bites Cut Florida Orange Crop to Two-Decade Low: Commodities

- China’s Soybean Demand May Rise Amid Scrutiny of DDGS Imports

- WTI Crude Little Changed Amid Low Volumes on U.K. Boxing Day

- Palm Oil Climbs to Two-Week High as Output May Drop in Malaysia

- Rebar in Shanghai Closes Near Five-Week Low as Inventory Climbs

- WTI-Brent Squeezed in December, Though Above 2013 Lows: BI Chart

- Red Kite Metals Fund Gains More Than 40%, Telegraph Reports

- Iraq Seeks to Buy 30,000 Metric Tons of Rice: Ministry

- BTG Grows in Commodities as Big Banks Retreat: Corporate Brazil

- Russia Seeks Belarusian Gasoline to Cover Peak Demand in 2014

- Batista Cedes Control of Oil Explorer in $5.8 Billion Debt Deal

- China Said to Increase Scrutiny of U.S. Imports for GMO Corn

CURRENCIES

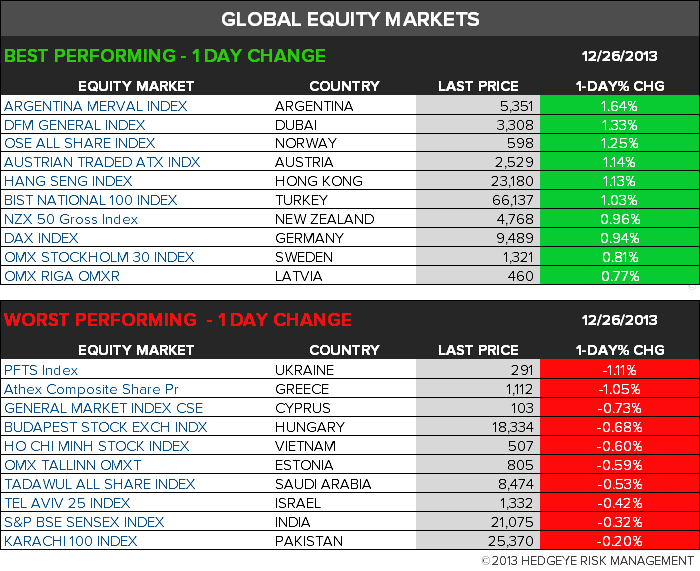

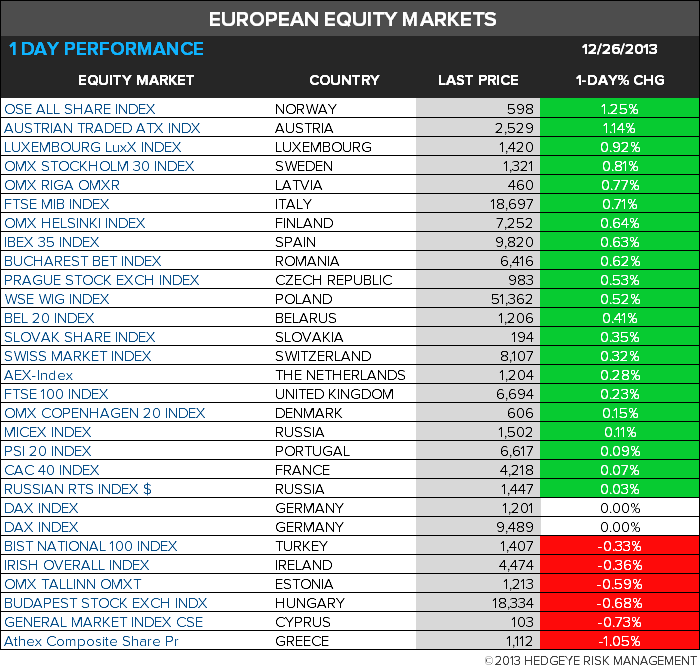

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team