TODAY’S S&P 500 SET-UP – December 23, 2013

As we look at today's setup for the S&P 500, the range is 33 points or 1.39% downside to 1793 and 0.42% upside to 1826.

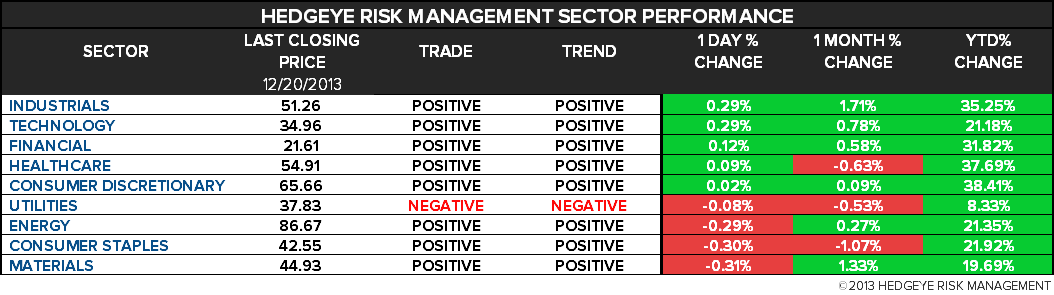

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.52 from 2.51

- VIX closed at 13.79 1 day percent change of -2.54%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Chicago Fed Natl Activity Index, Nov. (prior -0.18)

- 8:30am: Personal Income, Nov., est. 0.4% (prior -0.1%)

- 9:55am: UofMich. Conf., Dec. final, est. 82.7 (pr. 82.5)

GOVERNMENT:

- Deadline for Americans who want coverage effective Jan. 1 under ACA; hundreds of thousands whose health plans are being canceled as their coverage doesn’t meet rules are exempt next yr

WHAT TO WATCH:

- Apple strikes deal to sell iPhone through China Mobile

- U.S. eco growth to quicken next yr, IMF’s Lagarde says

- OPEC ministers see no ’14 glut amid signs of demand growth

- Tiffany ordered to pay Swatch $449m over venture dispute

- Shoppers get big discounts on last-minute holiday purchases

- Apple CEO Tim Cook sees “big plans” for 2014: 9to5Mac

- YRC said close to getting $250m in equity: WSJ

- Darden shrholder Starboard to push company reorganization: WSJ

- Elliott “irrevocably” rejects McKesson’s offer for Celesio

- “Hobbit” sequel leads N.A. weekend box office w/ $31.5m

- Goldman real-estate investment fund escapes Volcker rule: WSJ

- Paulson sells Washington Mutual debt amid FDIC lawsuit: WSJ

EARNINGS:

- No earnings expected from S&P 500

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gas in New York Surges to Highest Intraday Price in Two Years

- Hedge Funds Cut Gold Bull Bets Amid Record Outflows: Commodities

- WTI Trades Near Two-Month High on U.S. Growth, Sudan Violence

- Nickel Reaches Seven-Week High as Indonesian Export Ban Nears

- Soybeans Advance as Dry Conditions in Argentina May Stress Crops

- Gold Resumes Decline in London on Less Haven Demand Speculation

- Rebar in Shanghai Falls to One-Month Low as Ore Price Declines

- Cocoa Climbs as Much as 0.5% to Highest Price Since Sept. 2011

- Gold Assets Post Biggest Weekly Drop Since July as Prices Slump

- Last U.S. Lead Smelter Closes Toxic History in Ore-Rich Missouri

- Speculators ‘Throwing Money’ at Natural Gas on Icy Blast: Energy

- Refiner EPS, Ebitda May Rebound on WTI-Brent: 2014 Outlook

- Qatar to Boost Europe LNG Sales as Gas Trades at 7-Year High

- Raw Sugar Falls as Traders Have First Net Short Since September

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team