This note was originally published at 8am on December 09, 2013 for Hedgeye subscribers.

“History tells us that the threat to prosperity is not debt but socialism.”

-George Gilder

After a +3.6% US GDP print and back to back bullish monthly surprises on the US employment front, you’d think that America’s currency would get a bid. Nope. Why?

Irrespective of December-taper “odds” doubling last week (34% of “economists” in the Bloomberg survey think DEC-taper = #on versus 17% prior), Mr. Macro Market is still telling you that Ben Bernanke will devalue the Dollar for as long as he can.

Since the Fed is both un-elected and unaccountable, would you call this socialism? Whatever you want to call it, not letting free-market prices clear is a threat to the long-term economic prosperity of this country. So make sure to sell some stuff high on that.

Back to the Global Macro Grind…

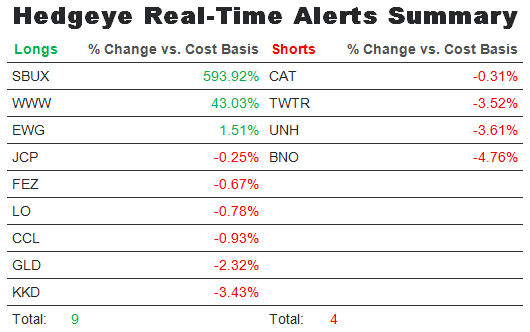

After 5 consecutive down days, the 2013 US stock market bears got ripped for a +1.12% move on Friday. You either bought-the-damn-bubble #BTDB on red during the -1.2% five-day correction, or you did not. We call this managing the risk of the range.

If @FederalReserve continues to debauch the Dollar, the makeup of what works on US stock market up days will start to change. This is what happened in 2011 in particular. It’s also what happened last week:

- Utilities (XLU) = +1.1% on the week

- Consumer Discretionary (XLY) = -0.7% on the week

In other words, Policies to Inflate slow the expectations of future real-inflation-adjusted-economic-growth. This is not new to anyone who lives in the real world – it just annoys the Keynesians.

Here’s another way to look at inflation expectations rising in the face of US purchasing power falling:

- US Dollar Index down another -0.5% last week (down 4 straight weeks) to +0.7% YTD

- CRB Commodities Index (19 commodities) +1.4% last week to -5.5% YTD

In other words, if the market expects the Fed to devalue the value of money, it will start to bid up the prices of things you buy with those moneys. Venezuela burned its currency at the stake. Its stock market index is now 2,597,592.25 (+451% YTD). #Cool, eh?

Obviously the USA going back to where we were in 2011-2012 (weak currency and nothing sustainable to speak of from a real-economic growth perspective), would be bad. I don’t doubt, for one second, that the Fed can perpetuate that.

To review why we were bullish on US #GrowthAccelerating in 2013:

- PURCHASING POWER: US Dollar was baking in A) fiscal sequestration and B) tapering well into Q313

- INFLATION: #StrongCurrency + #RatesRising would Deflate The Inflation (CPI surprised consensus on the downside)

- GROWTH: from 0.14% in Q412 to +3.6% in Q313, and business expectations cycle took hold

And yes, as business and consumer confidence rose in Q3, fixed investment and inventories rose. It’s called a cycle. So did the Savings Rate (5.0% in Q3 vs 4.7% in the prior report). When people have more money, they have more to save too!

The other thing that happened in Q313 that got zero attention from the disingenuous (whining) 2013 perma bears last week was that the DEFLATOR in the US GDP report actually understated GDP growth by almost 0.3%.

After almost hitting a 40-yr low in Q2 (yes that was stimulative for US consumption growth, like it was in Q109), the US GDP Deflator was 1.96%. That was more than a double, sequentially, and +24 basis points higher than MIT’s Billion Prices Project inflation rate of 1.72%.

*higher deflator (i.e. more inflation) subtracts from reported GDP growth

Put another way, in our GIP (GROWTH, INFLATION, POLICY) model, provided that the Fed doesn’t taper in December, you can pretty much bake the opposite call we’ve had in the last year into the cake:

- US DOLLAR could start to see more downward pressure into Q114

- INFLATION (both CPI and PPI headline) should bottom, sequentially, in Q413 (rise in Q1)

- GROWTH should slow, sequentially, in Q413-Q114, in kind

So what do you do with that? That’s easy. Buy “slower-growth” assets and some inflation protection.

We also like the prospects for European #GrowthAccelerating (see our Q413 #EuroBulls Macro Theme) if EUR/USD continues to strengthen like it did again last week (+0.8% to +3.9% YTD).

You might call some Europeans socialists; but they might just call Americans that now too.

Our immediate-term Risk Ranges are now (we have 12 Big Macro Ranges in our Daily Trading Range product):

UST 10yr yield 2.79-2.91%

SPX 1785-1813

VIX 12.23-14.91

USD 80.09-80.63

EUR/USD 1.35-1.37

Gold 1216-1259

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer