TODAY’S S&P 500 SET-UP – December 20, 2013

As we look at today's setup for the S&P 500, the range is 29 points or 0.97% downside to 1792 and 0.63% upside to 1821.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.56 from 2.57

- VIX closed at 14.15 1 day percent change of 2.54%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: GDP Annualized q/q, 3Q rev, est. 3.6% (pr. 3.6%)

- Pers. Consumption, 3Q revision, est. 1.4% (prior 1.4%)

- 11am: Kansas City Fed Manuf Activity, Dec., est. 6 (pr 7)

- 1pm: Baker Hughes rig count

GOVERNMENT

- 9:30am: U.S. Chief Negotiator Dan Mullaney, EU Chief Negotiator Ignacio Garcia-Bercero hold press conference

- 10am: U.S. Treasurer Rosie Rios signs currency

- Senate adjournment will follow confirmation of nominations including John Koskinen to lead IRS

- President Barack Obama, family scheduled to depart for Hawaii for Christmas

- China’s Vice Premier Wang Yang, U.S. Commerce Secretary Penny Pritzker, U.S. Trade Representative Michael Froman chair mtg of U.S. and China Joint Commission on Commerce and Trade; Beijing,

WHAT TO WATCH:

- Senate pushes Yellen confirmatione to Jan. in nominee deal

- Passes defense authorization totaling $625.1b

- Obama kills health insurance mandate for canceled policies

- Bankers say agencies’ answer on Volcker CDO rule inadequate

- SEC internal clashes said to flare over CMBS cases, NYT says

- Banks said to snitch on FX competitors to avoid EU fines

- Sycamore to buy Jones Group fashion co. for $1.2b

- Jazz Pharma. buys rare disease drugmaker Gentium for $1b

- Banks said preparing for Sprint bid for T-Mobile: WSJ

- Axiall to tap cheap gas with $3b Louisiana ethylene plant

- Apple’s Oracle dispute split from patent-infringement suit

- Apple says demand for Mac Pro outstripping supply: Forbes

- AmEx merchant settlement allows different debit surcharges

- Cathay Pacific orders 21 Boeing planes valued at $7.5b

- Fisker won’t make cars at Delaware GM plant, Carper says

- TD Bank not focusing on large U.S. retail expansion: CEO

- Chinese accused of plotting to steal DuPont’s GMO corn

EARNINGS:

- BlackBerry (BB CN) 7am $(0.46) - Preview

- CarMax (KMX) 7:35am $0.48

- Finish Line (FINL) 7:05am $0.02

- Navistar International (NAV) 7am $(1.56) - Preview

- Walgreen (WAG) 7:30am $0.72 - Preview

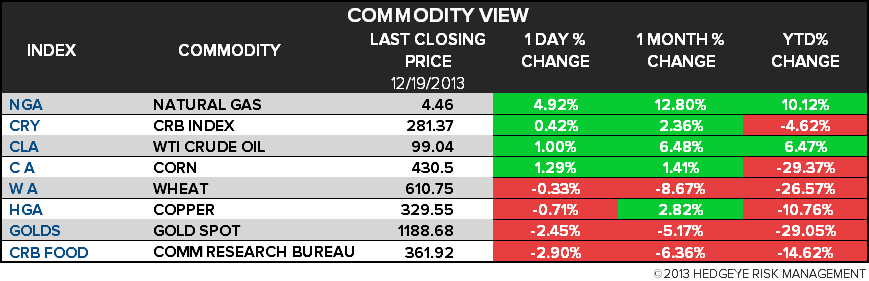

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Wheat Reaches 19-Month Low as Argentine Crop Adds to Supplie

- Gold Climbs From Lowest Close Since 2010 as Goldman Sees Los

- Barrick Omen for Gold Miners With $44 Billion Debt: Commoditie

- Brent Heads for Weekly Gain on Growth Prospects After Fed Mov

- Copper Rises as Growth Outlook Fuels Closing of Bets on Declin

- Raw Sugar Rallies for 2nd Day as Robusta to Arabica Coffee Dro

- WTI-Brent Spread Narrowing as U.S. Exports Record Fuels: Energ

- Indonesia Must Consider Economic Impact From Ore Ban: Wacik

- Shanghai Gold Exchange Contract Volume Surges on Price Slump

- Commodity Funds Post First Outflow Since 2000: Chart of the Da

- Aluminum Surplus May Widen Through 2015 on Output, Marubeni

- Refiners Turn to Exports, With 4% Growth Expected: 2014 Outloo

- Wheat Traders Turn Bullish After Two Weeks of Betting on Decli

- Rebar Posts Worst Week in a Month on China Cash Crunch Concerns

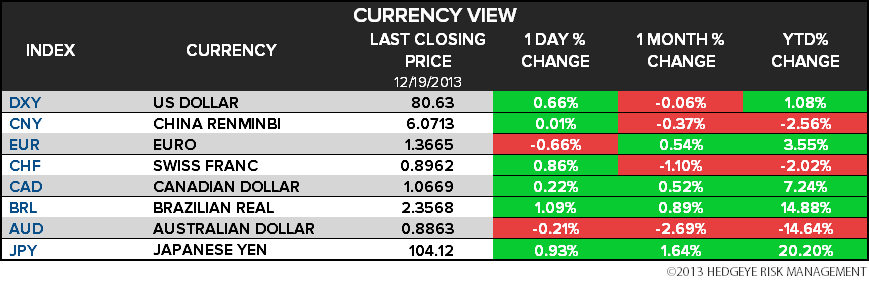

CURRENCIES

GLOBAL PERFORMANCE

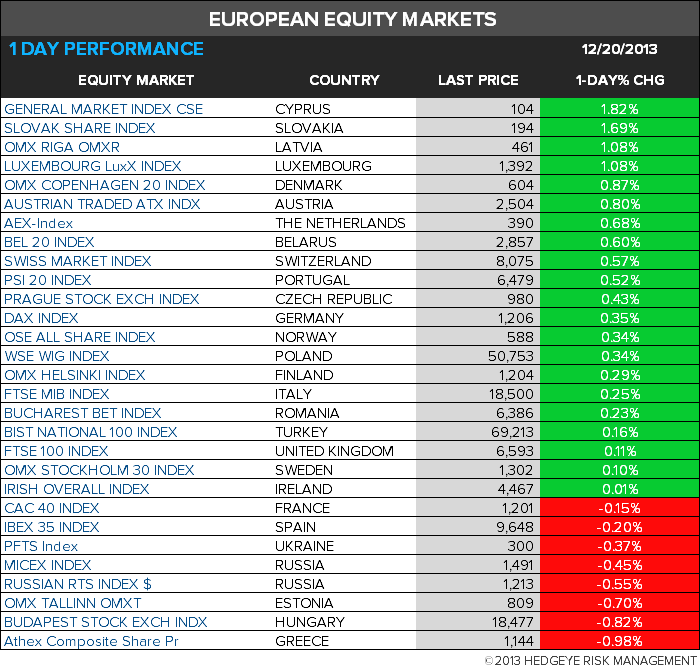

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team