I've been a vocal bull on Under Armour. Finish Line management made what I would consider cautionary comments about UA footwear. Here at Research Edge, we don't hide from facts. We face the music. Ok, let's dance...

Here's what management said in response to a question about UA footwear...

- o Initial running pretty good

- o Has slowed down a bit

- o Though running category overall is positive stand out

- o Played down UA, looking forward

- o Noted that expectations were just too high off the bat

My Take

Is this a disaster? No, but the tonal change toward the back half can't be ignored. My sense is that these guys were expecting the UA launch to allow them to perform well in a horrible retail environment. But that's just not the kind of roll-out this was. It is slow, steady and more measured. It is not, and was not, geared to be a near-term sales pop for retail. There's simply not enough product out there to drive the retailers' comps.

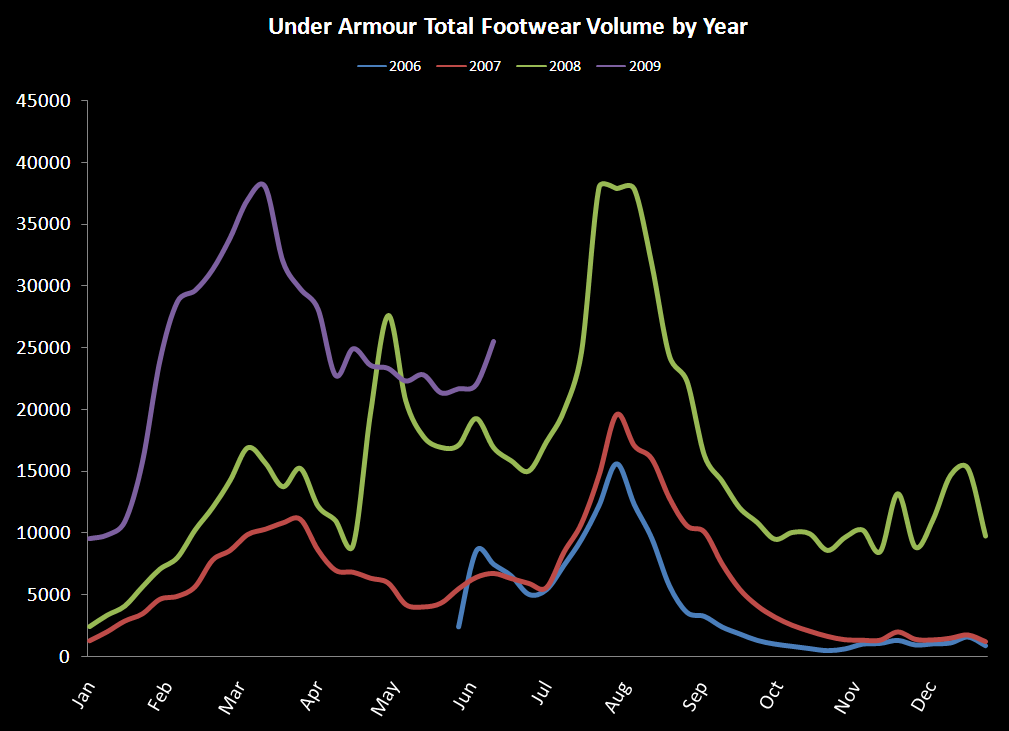

Weekly NPD sales numbers look fine to me. Within the context of a growing running category, UA's share remains constant with where it has been since March (3% of the category). Are there incremental discounts in price in the final weeks of June? Yes. But ASP remains at $82, with Nike at $75 and the industry average closer to $50. This is normal activity as retailers clear the shelves for product coming in for July 1 (especially after 6 weeks of rain).

Call me stubborn, but I still think that the big call here is taking this business from 1% of the market to 5%, and then 10% -- and most importantly, getting the management structure in place o achieve such growth. I'm really confident that UA is making that happen, as outlined in my recent research.

I must admit, I was initially surprised to see UA trade up on these comments. Then it dawned on me... this is because of the Foot Locker announcement of its CEO change. After all, if you are the Chief Merchant of one of the largest retailers in the US that has sheer dominance over all of its customers, how comfortable would be if you took on the role at a smaller retailer where one vendor (Nike) accounts for over half of your sales. You're not gonna like that very much. I'm not suggesting that we see Nike/Foot Locker channel war all over again (as we saw 6 years ago), but it is not impossible. Either way, the new guy is going to be looking to harvest relationships with brands that the Consumer genuinely wants to succeed. Enter Under Armour...

Oh, and by the way, the Nike acquisition rumour is back. I'd place a higher probability of Abercrombie buying Procter & Gamble.