2QF14 RESULTS

As expected, DRI reported 2QF14 results in which both top and bottom lines came in light. Revenues of $2.05 billion and diluted EPS of $0.15 missed consensus estimates by -0.76% and -22.6%, respectively. Resembling a company in dire need of revival, restaurant level margins and operating margins fell -143 and -140 bps, respectively, in the quarter. Prior to the call, management released its plan to increase shareholder value. This includes plans for a spin-off or sale of the Red Lobster brand. We will hit on the details of the plan and our initial thoughts later in the note.

GUIDANCE

Management finally did what it was so reluctant to do last quarter and guided down their projections for FY14. As it stands, the company expects FY14 diluted EPS to decline 15-20% year-over-year. Blended same-restaurant sales for Olive Garden, Red Lobster, and LongHorn Steakhouse are also expected to be lower than initially anticipated. Due to this, the company expects revenues to grow 4% to 5%, rather than the prior estimate of 6% to 8%.

Revised FY14 SRS Estimates

- Olive Garden (1%) to (2%)

- Red Lobster (4%) to (5%)

- LongHorn +2% to +3%

SEGMENT PERFORMANCE

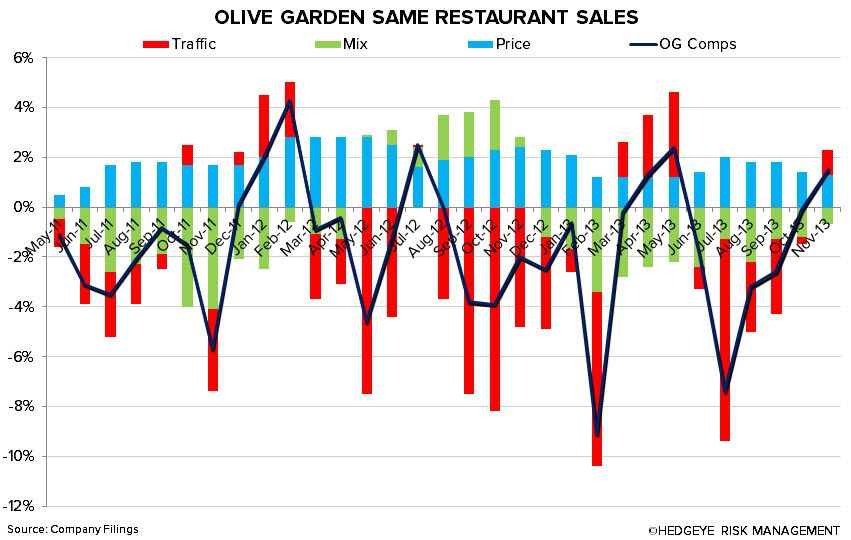

2QF14 was another quarter of ugly same-restaurant sales and traffic trends, specifically at DRI’s two largest brands: Olive Garden and Red Lobster. Clearly these two business models (the most important two) are broken. Darden’s smaller brands fared much better in the quarter. Same-restaurants sales were up at LongHorn (+5%), Capital Grille (+6.7%), Bahama Breeze (+5.7%), Eddie V’s (+5.7%), Yard House (+1.2%) and Seasons 52 (+1.2%) during the quarter.

What Darden’s plan failed to address this morning, was how they are going to turn around Olive Garden and Red Lobster. Same-restaurant sales and traffic trends have been anemic for the past several years. We didn’t learn enough about the “Brand Renaissance" initiative at Olive Garden to conclude that it will have a material impact on sales. After all, they just introduced a hamburger to the menu -- How authentically Italian can their vision be? In regards to Red Lobster, management is simply pushing it to the side. There is no real plan to fix it and, to be honest, we’re not even sure it can be fixed.

DARDEN'S PLAN TO ENHANCE SHAREHOLDER VALUE

Separate the Red Lobster Business

The company plans to execute a tax-free spin-off of Red Lobster to shareholders that would close in early FY15. They will also consider a sale of the Red Lobster business. No final decision had been made on the form of separation.

Per page 7 of the company’s investor presentation, the strategic focus of the New Darden and New Red Lobster will be:

New Darden

“Retaining core customers and expanding customer base to grow same-restaurant sales and market share.”

“Selective investment in expanding customer base and new unit growth to drive cash flow growth and growth in return of capital to shareholders.”

New Red Lobster

“Retaining core customers to maintain stable same-restaurant sales.”

“Consistent and stable cash flow generation to support stable return of capital to shareholders.”

THE HEDGEYE TAKE: This plan is a desperate, yet unfulfilling attempt to appease shareholders. In fact, this separation doesn’t solve much other than removing an underperforming brand from the portfolio. Fixing Olive Garden should be management’s number one priority. Our vision of the New Darden properly aligns Darden’s brands and organizes the portfolio in a way that would be beneficial to each NewCo.

Reduce Unit Growth, Lower Capex, and Forgo Acquisitions

The reduced unit growth will come primarily from Olive Garden, where management plans to halt any new unit growth for at least a few years. They also plan to slightly slow unit growth at LongHorn and expect unit growth at the Specialty Restaurant Group to be slightly lower next fiscal year. This unit growth reduction is estimated to save approximately $100 million in capital expenditures per year. In an effort to allay concerns over the company’s oversized portfolio, management also announced that it will forgo acquisitions of additional brands for the foreseeable future.

THE HEDGEYE TAKE: Similar to Darden’s plans to spin-off the Red Lobster business, these initiatives simply aren’t enough. In our opinion, the company needs to stop growing altogether. We believe management is cutting capital expenditures to cover their dividend this year. In a sense, they aren’t slowing growth because they want to, they are slowing it because they have to.

Increase Cost Savings

Through support cost management, the team expects annual savings of $60 million beginning in FY15. This is slightly up from the $50 million in annual savings the company announced last quarter. They plan to continue the search for cost efficiencies.

THE HEDGEYE TAKE: There’s nothing new here. We actually view this news as disappointing. Darden’s business is riddled with excessive spending. For management to only find an additional $10 million in annual cost savings is, at the very least, discouraging.

Increase Return of Capital to Shareholders

The company plans to use the reduction in capital expenditures and additional cash flow from savings to fund dividends, make opportunistic share repurchases, and strengthen its credit profile. They intend to maintain their $0.55 quarterly dividend.

THE HEDGEYE TAKE: This is one of the only things Darden has been good for over the past several years. As we stated earlier, we believe they were forced to cut costs in order to maintain the current quarterly dividend.

Refine Compensation and Incentive Programs

The company plans to refine compensation and incentive programs for senior management to more directly emphasize same-restaurant sales performance and free cash flow growth. The company currently rewards management for growing sales and earnings.

THE HEDGEYE TAKE: There weren’t too many details provided with this, but it sounds like a step in the right direction. Compensation and incentive programs, however, should be very far down the priority list if the team is serious about fixing the business and unlocking shareholder value.

EARNINGS CALL

A number of analysts appeared agitated on the call, particularly in regards to management’s loose projections for FY15. Analysts appeared concerned with the authenticity of the strategic plan, the feeble cost cuts, the potential for a REIT or sale leaseback, and whether meaningful value would be created through the spin-off of Red Lobster.

CONCLUSION

We don’t believe the initiatives announced today are enough to unlock the true, underlying value of Darden. Quite frankly, it seems as though these moves were made simply because management had to do something. Spinning off Red Lobster, slightly slowing growth, and cutting capital expenditures to fund the dividend does very little to help fix the business.

The company’s number one priority should be turning around Olive Garden. It is a strong, iconic brand that should be the leader in the casual dining category. This starts with getting the right management team in place that will harness the brand’s authentic Italian heritage.

Following the call, we are as convinced as ever before that this is not the final step. We expect to see more activist pressure in the coming months and believe that Darden will eventually be properly restructured; if this is the case, there will be significant shareholder value to be had. As we've said before -- we know how this will end, we just don’t know when.

Recent Notes

12/17/13 – Best Idea Update: Long DRI

12/11/13 – Restaurant Impossible: Fixing Olive Garden

10/30/13 – DRI: Pending FY2Q14 Disaster?

10/18/13 – Dismantling Darden: Hedgeye vs. Barington

10/15/13 – DRI: A Generational Opportunity

9/12/13 – Dismantling Darden

8/21/13 – DRI: Restructuring Charge Looming?

6/26/13 – DRI: Beware of False Narratives

6/21/13 – DRI Comps Flatter to Deceive

6/17/13 – DRI Remains a Win-Win

5/23/13 – DRI’s Jamie Question

Let us know if you have any questions or would like to discuss anything in more detail.

Howard Penney

Managing Director