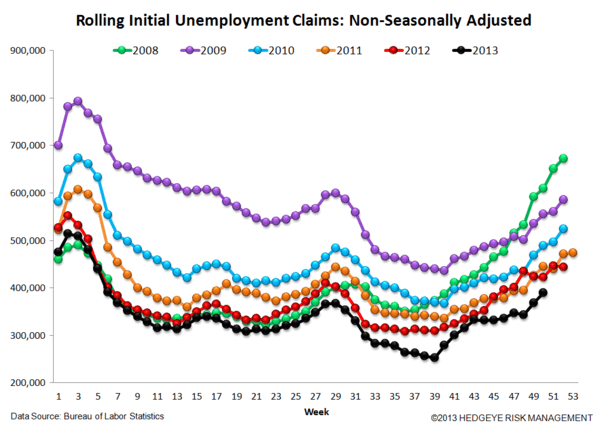

This morning’s Initial jobless claims data reflected a second week of deterioration for the domestic labor market. While the broader trend remains healthy and seasonality will continue to build as a tailwind, the recent softness is noteworthy in that there is no discrete, identifiable distortion other than the seasonal volatility that generally characterizes the peri-holiday period. We wouldn’t read too much into the recent advance in claims, but it is worth a flag.

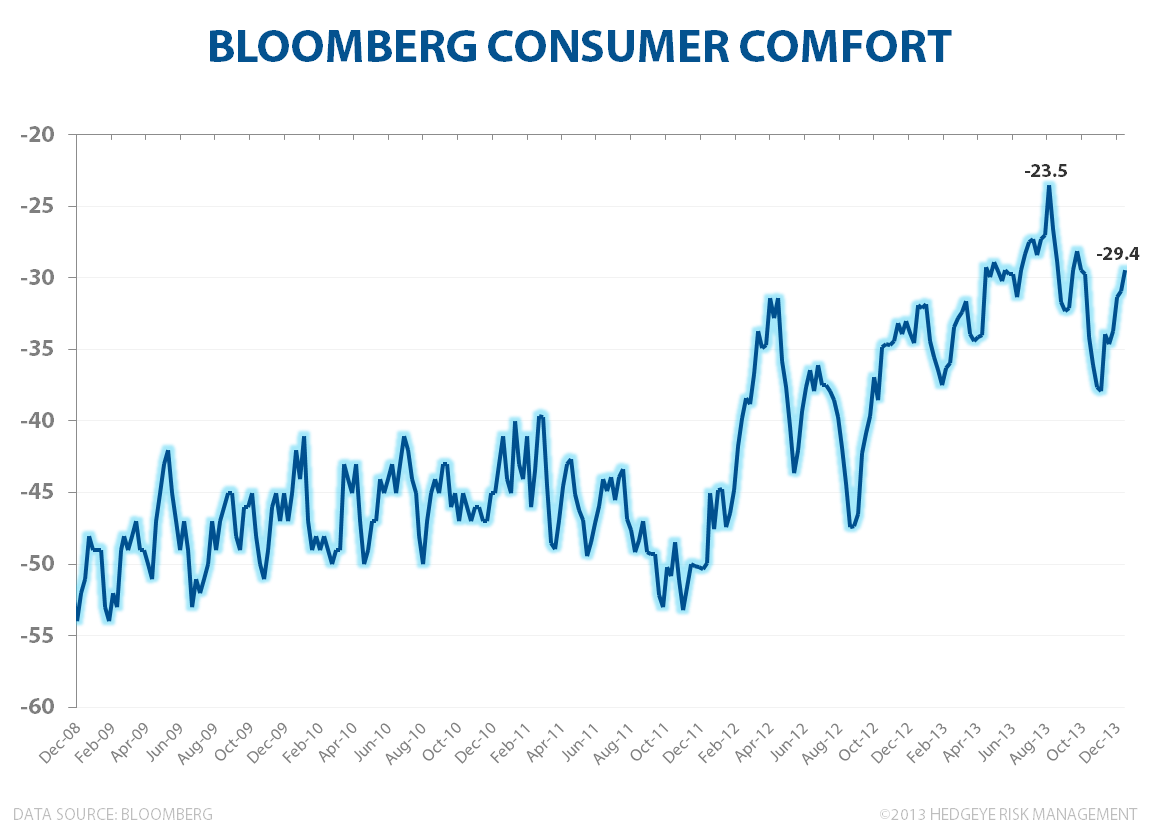

Confidence, meanwhile, remains resurgent with bloomberg’s weekly read on consumer confidence recapturing the elusive 20-handle as the post-government shutdown hangover in populace sentiment continues to ebb. We’ll get the final University of Michigan reading on Monday, but the preliminary data showed a positive inflection similar to that observed in the bloomberg survey.

The U.S. dollar has moved in lockstep with monthly confidence over the past year and, now, with the taper announcement on the tape and the dollar recapturing the $80.15 TRADE line, we’re vapidly optimistic we could see a return to sustainable, #StrongDollar led growth into 2014.

Below is the breakdown of this morning's claims data from the Hedgeye Financials team along with some sector specific insight. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

- Hedgeye Macro

--------------------------------------------------------------------------------------------------------------------

INITIAL CLAIMS: Should We Be Concerned?

The labor data has softened now for two weeks in a row. The first week of weak data (two weeks ago) represented a seasonal mismatch and wasn't anything overly noteworthy. The second week - the most recent week - however, showed a more legitimate soft patch in the data.

Normally, we see a surge in claims following black Friday representing the seasonal layoff of retail workers. Then, in the following week we see claims drop sharply. For reference, the average increase in claims from post-Black Friday layoffs over the last six years has been 175,000 (NSA). The subsequent decline in claims has averaged 91,000. That works out to a 52% reduction in the post-black Friday surge. This year, we saw an increase of 147,000 post-black Friday followed by a decline of 48,000, or right around a decline of 1/3 - well below the normal retracement. We'll keep a close eye on the trends into year-end.

Separately, with the Fed finally tapering its bond purchases we think it's important to remind investors of the setup going into the new year. Remember that the labor market has a built in tailwind that strengthens steadily from September through February, peaking in February/March and then reversing, and, ultimately, troughing in August/September.

This should be supportive of rising rates through 1Q14. We've shown rate correlations across the Financials over the bulk of 2013 and we would expect that the playbook through the next 2-4 months should mirror that. For more information on how to position in that environment, see our note from 11/22/13 entitled #Rates-Rising: A Current Look at Rate Sensitivity Across Financials.

The Data

Prior to revision, initial jobless claims rose 11k to 379k from 368k WoW, as the prior week's number was revised up by 1k to 369k.

The headline (unrevised) number shows claims were higher by 10k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 13.25k WoW to 342.25k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -7.7% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -13.0%

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT