TODAY’S S&P 500 SET-UP – December 19, 2013

As we look at today's setup for the S&P 500, the range is 29 points or 1.09% downside to 1791 and 0.52% upside to 1820.

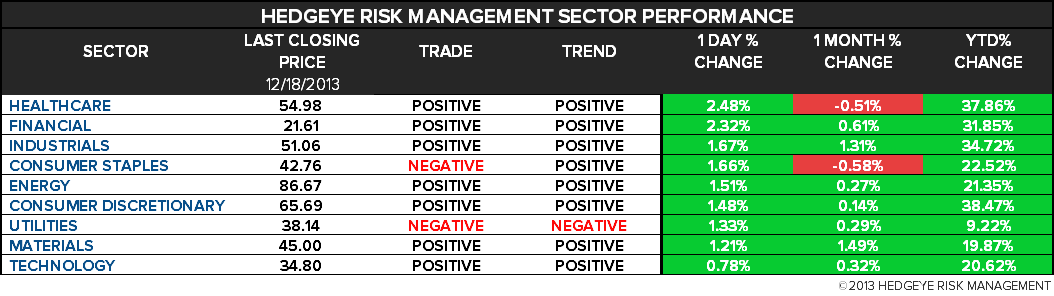

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.56 from 2.56

- VIX closed at 13.8 1 day percent change of -14.87%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Init. Jobless Claims, Dec. 14, est. 335k (pr 368k)

- 8:30am: Continuing Claims, Dec. 7, est. 2.77m (prior 2.79m)

- 8:30am: Fed’s Fisher speaks on economy in Dallas

- 9:45am: Bloomberg Consumer Comfort, Dec. 15 (prior -30.9)

- 10am: Philly Fed Business Outlook, Dec., est. 10 (pr 6.5)

- 10am: Existing Home Sales, Nov., est. 5.02m (prior 5.12m)

- 10am: Leading Index, Nov., est. 0.7% (prior 0.2%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

GOVERNMENT:

- Senate in session, expected to vote on defense authorization; House meets in pro forma session

- Agriculture Sec. Tom Vilsack, Commerce Sec. Penny Pritzker, US Trade Representative Michael Froman travel to U.S. Joint Commission on Commerce and Trade

- 10:30am: Senate Homeland Security panel holds hearing on alleged misconduct by office of DHS IG

WHAT TO WATCH:

- AstraZeneca to buy Bristol-Myers stake in diabetes JV

- Bayer to buy cancer-drug partner Algeta for $2.9b

- Tesla charger may have caused fire in garage, Reuters says

- Co. denies that car, charger, battery at fault

- NYSE passed as biggest market owner by merging upstarts

- Secret Service investigating data theft from Target

- Facebook, bookrunners must face class action, judge says

- NSA panel recommends meeting Yahoo, Facebook demands

- Some U.S. cities considering bans on e-cigarettes: WSJ

- Microsoft pulls Surface Pro 2 update on problems: Engadget

- Citi chooses AIA to sell insurance in Asia-Pacific branches

- Small shipping cos. expanding in threat to FedEx, UPS: WSJ

- Obama may sign first budget by split Congress since 1986

- CFTC glitch leads to misreporting size of swaps market: WSJ

- McDonald’s has chicken wing surplus after weak sales: WSJ

- Washington Post servers broken into by hackers: Wash. Post

AM EARNS:

- Actuant (ATU) 8am, $0.46

- Bio-Reference Labs (BRLI) 8:31am, $0.40

- Carnival (CCL) 9:15am, $0.00

- ConAgra Foods (CAG) 7:30am, $0.55

- Darden Restaurants (DRI) 7am, $0.20 - Preview

- KB Home (KBH) 8:32am, $0.48 - Preview

- Neogen (NEOG) 8:45am, $0.21

- Pier 1 Imports (PIR) 6am, $0.28

- Rite Aid (RAD) 7am, $0.05

- Scholastic (SCHL) 7am, $2.20

- Winnebago Industries (WGO) 7am, $0.37

- Worthington Industries (WOR) 8:30am, $0.55

PM EARNS:

- AAR (AIR) 4:05pm, $0.48

- Accenture (ACN) 4:01pm, $1.09

- Cintas (CTAS) 4:15pm, $0.68

- Nike (NKE) 4:15pm, $0.58

- Red Hat (RHT) 4:04pm, $0.35

- Tibco Software (TIBX) 4:05pm, $0.39

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Falls Below $1,200 First Time Since June on Fed Tapering

- WTI Trades Near One-Week High as Stockpiles Decline, Fed Tapers

- Brazil Crushing Sugar to Ethanol With Gasoline Caps: Commodities

- Copper Falls for Third Day on Dollar Rally, China Funding Costs

- Robusta Coffee Falls as Vietnam Sales May Advance; Cocoa Rises

- Indonesia Studying Rule for Miners With Smelters, Rajasa Says

- Rebar Falls to 3-Week Low After China’s Money Market Rate Jump

- EU Emission Slump Tests Broker Survival Skills: Carbon & Climate

- Rubber Nears 3-Month High as Yen Drops After Fed Tapers Stimulus

- Wheat Rebounds as Price Slump Seen Excessive Amid Import Demand

- Mars Blend Climbs to Six-Month High After Gulf Coast Stocks Drop

- Cocoa’s Cup & Handle Signals Extended Rally: Technical Analysis

- Vale Seeks Two U.S. Pellets Supply Contracts as Shale Gas Booms

- Billionaire Fredriksen’s Marine Harvest Seen Driving Fish Deals

- Ethanol’s Discount to Gasoline Widens on Increase in Stockpiles

CURRENCIES

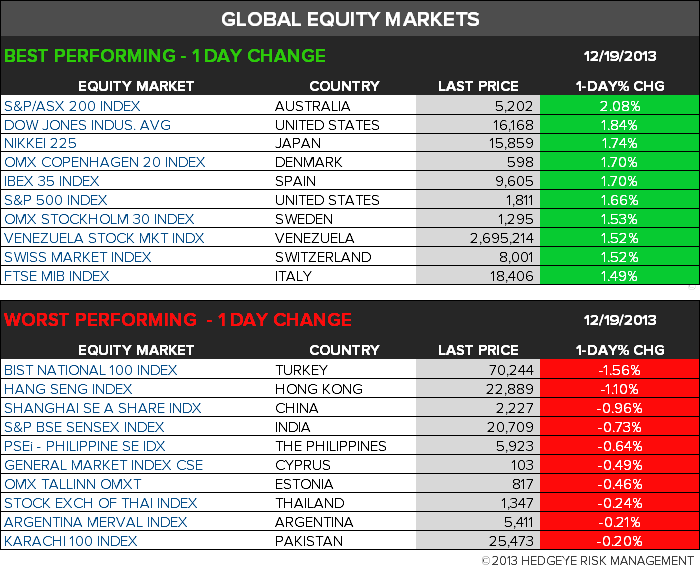

GLOBAL PERFORMANCE

EUROPEAN MARKETS

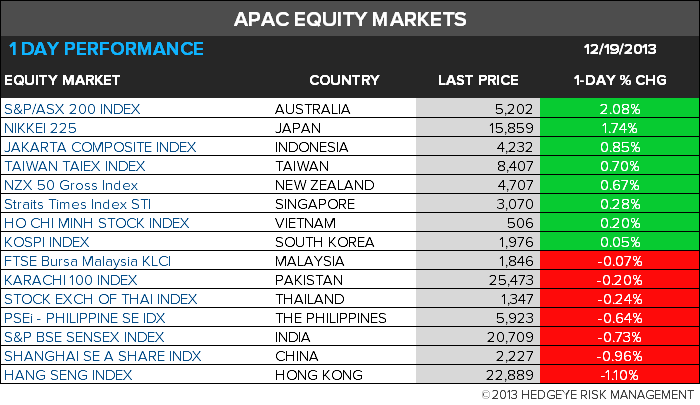

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team