We added Panera to the Best Ideas list as a short on 4/5/13 and continue to believe it is positioned as one of the best shorts in the QSR space heading into 2014. Until the street realizes the near-term severity of the situation, we will maintain our bearish bias.

AGGRESSIVE EXPECTATIONS

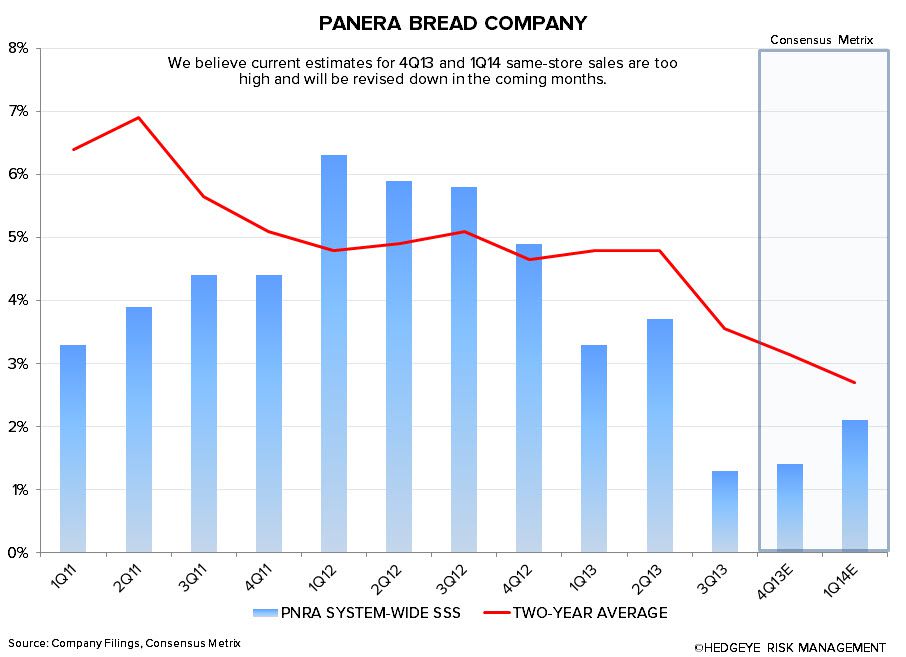

The current EPS estimate for 4Q13 is $1.94, well above the $1.86 we are modeling. We expect to see sales deleverage in the quarter and believe general & administrative costs and occupancy costs will come in higher than the street anticipates. The street is looking for $666 million in sales in 4Q13. Considering PNRA’s current operational and secular issues, we expect sales to come in closer to $655 million. Looking out to 1H14, EPS estimates appear overly aggressive and will likely be revised down in the coming months.

OPERATIONAL ISSUES

In the 3Q13 earnings call, management acknowledged the bevy of operational issues that the company faces today. These are largely self-inflicted and range from a lack of kitchen equipment to a lack of seating space in their cafes. According to CEO Ron Shaich during the 3Q13 earnings call:

“We analyzed every café to assess its physical capacity levels. What we found is that approximately 10% of our cafes are capacity constrained and approximately a third of our cafes would be constrained should we have a meaningful lift in transactions.”

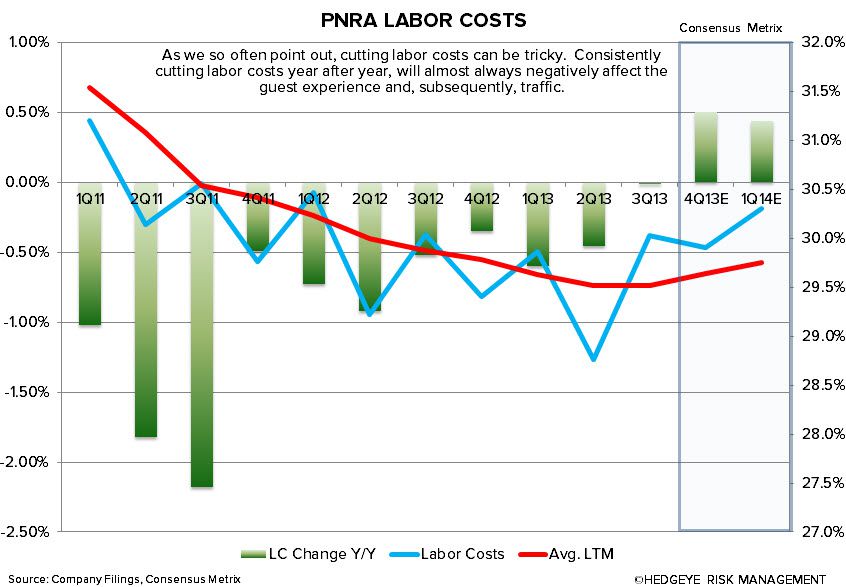

These capacity constraints, coupled with a lack of adequate labor, have stymied PNRA’s same-store sales growth in recent quarters. Slower speed of service and throughput issues, particularly during peak hours, have led to a less favorable customer experience and, subsequently, declining traffic. The two charts below illustrate why PNRA is having these issues today.

In an effort to improve throughput, capacity, and service, PNRA is now allocating additional capital to labor and equipment. We expect these increases on the labor and G&A lines will squeeze margins more than the street is anticipating in the coming quarters, particularly given the company’s soft sales trends. The fact of the matter is, these are not issues that will be solved in one quarter. It is a process that will take time.

SECULAR ISSUES

There are several secular forces working against Panera that didn’t exist a couple of years ago. Perhaps the most notable is increased competition. For one, there are now more fast casual options available than ever before. But it doesn’t end there. Panera is also seeing increased competition from QSR chains that have been upgrading there menus to include healthier items. These QSR chains heavily market their products and offer them at a cheaper price point than Panera’s core offerings, making them attractive to consumers.

All told, Panera’s value equation is out of sync. With cheaper prices offered at quick-service restaurants and aggressive discounting at casual dining chains, PNRA has no pricing power. With an average check in the $9 to $10 range, PNRA has created a pricing umbrella for non-traditional competitors to take advantage of. We have seen this play out over the course of the year, as many casual dining restaurants are currently offering meals in the $6-$7 range. Management is aware of this value issue and is working to fix it, but, once again, this will take time.

These operational and secular issues have manifested in the form of declining comparable sales and traffic trends. This is always bad, but particularly bad when coupled with an increase in spending. Margins will inevitably contract and earnings growth will decelerate. Considering the street’s aggressive expectations, we believe PNRA is well positioned to post a couple of subpar quarters.

CURRENT INITIATIVES

What we like most about Panera’s current situation is that management is aware of the company’s issues and is working to fix them. Chairman and CEO Ron Shaich is a great leader that we believe will eventually be able to get the company on the right track again. That being said, the team has several initiatives planned for 2014 to right the ship.

These include investing to improve its café operating experience, reconfiguring product lines, adding labor to cafes, improving speed of service and the customer experience, streamlining its menu offerings, testing lower priced items to improve its value perception, improving product consistency, and ramping up advertising spend to drive incremental traffic.

To be fair, the vast majority of PNRA’s initiatives address our concerns. But, to believe the effect of these will be immediate is, in our view, misguided. We can’t help but wonder if the system can handle all of these changes at once.

BULL CASE

We understand the bull case. Panera is a beloved company, management is promptly addressing the issues, and trends will begin to accelerate. In fact, we don’t completely disagree with this view in the long-term. However, the bulls are underestimating the length of this turnaround, or regrouping, process. Increasing expenses, which they must do, while traffic is declining and the secular backdrop is discouraging will undoubtedly negatively affect margins. We just happen to think it will negatively affect margins more and for a longer time than the street currently expects.

CONCLUSION

PNRA is a good company that has many factors currently working against it in 4Q13 and through 1H14. That being said, if management is able to quickly address operational issues and successfully implement the planned demand drivers, we believe trends will accelerate through 2H14 and into 2015. As it stands, Panera is well positioned for the back half of 2014 – but there will be some near term pain.

Recent Notes

10/23/13 – PNRA: The Pace of Change?

10/21/13 – PNRA: Stage 1 Denial

9/26/13 – PNRA: No Quick-Fix Recipe

7/23/13 – PNRA Short Thesis Playing Out As Expected, Part II

4/24/13 – PNRA Short Thesis Playing Out As Expected

4/05/13 – PNRA Hype Makes It Shortable

3/26/13 – PNRA Happy Camper Facing QSR Wounded Bears

2/15/13 – PNRA Mix Tapped Out?

1/30/13 – PNRA Bread Not Quite Baked

Let us know if you have any questions or would like to discuss any of our current ideas in more detail.

Howard Penney

Managing Director