TODAY’S S&P 500 SET-UP – December 18, 2013

As we look at today's setup for the S&P 500, the range is 51 points or 0.95% downside to 1764 and 1.91% upside to 1815.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.51 from 2.52

- VIX closed at 16.21 1 day percent change of 1.12%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Dec. 13 (prior 1%)

- 8:30am: Housing Starts, Nov., est. 954K

- 10:30am: DOE Energy Inventories

- 2pm: FOMC seen maintaining federal funds target of 0% to 0.25%; releases summary of economic projection

- 2:30pm: Fed’s Bernanke holds news conference

GOVERNMENT:

- Senate in session, House not in session

- 10am: Senate Foreign Relations panel meets on “Economic Engagement in the Asia-Pacific”

- 2:30pm: Senate Commerce Cmte holds hearing on data brokers’ use of personal information about consumers

WHAT TO WATCH:

- FOMC to issue policy statement, new forecasts at 2pm today

- JPMorgan sues FDIC over >$1b Washington Mutual liabilities

- JPM sued by Mississippi on credit card conduct: Reuters

- Silver Lake said in $2.4b deal for Forstmann Little’s IMG

- GE seen raising margins on demand for industrial goods

- Facebook acquires startup SportStream, AllThingsD says

- Wal-Mart to open 2 Sam’s Clubs in China in 2014

- Nintendo experimenting with smartphones, tablets: KING-TV

- Blackstone buys 3 Texas power plants from Centrica for $685m

- China Mobile plans smartphone sales of 220m in 2014

- Chipotle testing pizza as next possible fast food: WSJ

- ResCap sues UBS, SunTrust, Capital One over CMBS buybacks

- EU set to fine Goldman PE unit over cable maker price fixing

- Novartis’s cancer therapy faces question of logistics

- Pentagon says dependence on China rare earths has lessened

- Cantor to get $135m from American Airlines over 9/11 attacks

- Israel wants Google royalties for local content, Globes says

EARNINGS:

- Apogee Enterprises (APOG) 4:30pm, $0.35

- FedEx (FDX) 7:30am, $1.64 - Preview

- General Mills (GIS) 6:58am, $0.87 - Preview

- Herman Miller (MLHR) 4pm, $0.40

- Lennar (LEN) 6am, $0.62 - Preview

- Oracle (ORCL) 4:01pm, $0.67

- Paychex (PAYX) 4:01pm, $0.42

- Quanex Building Products (NX) 7am, $0.14

- Steelcase (SCS) 4:01pm, $0.26

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- EU Proposes Ban on Cloning Farm Animals and Sale of Clone Meat

- Goldman Sachs Said to Name New Global Commodities, Metals Heads

- Rio Tinto CEO Sees Iron-Ore Price Decline Next Year: Commodities

- Brent Trades Near One-Month Low Before Federal Reserve Decision

- Copper Falls a Second Day Before Fed Policy Meeting’s Outcome

- Gold Climbs in London Before Fed’s Decision: Palladium Advances

- Wheat Reaches 18-Month Low on Outlook for Rising Global Supply

- White Sugar Extends Drop to 2010-Low on Supply; Coffee Advances

- Australia Seen Boosting Bauxite Exports on Indonesia Ore Ban

- U.S. Pump Prices Seen Setting 2013 Low as Supply Swells: Energy

- U.S. Refiners Have Steep, Sustainable Advantage: 2014 Outlook

- Silver Proving No Store of Stability in Flight: Riskless Return

- U.S. Auto Revival Boosts Shipping as Jeeps Go to China: Freight

- Australia to Boost Iron Ore Exports as Rio to BHP Expand Output

CURRENCIES

GLOBAL PERFORMANCE

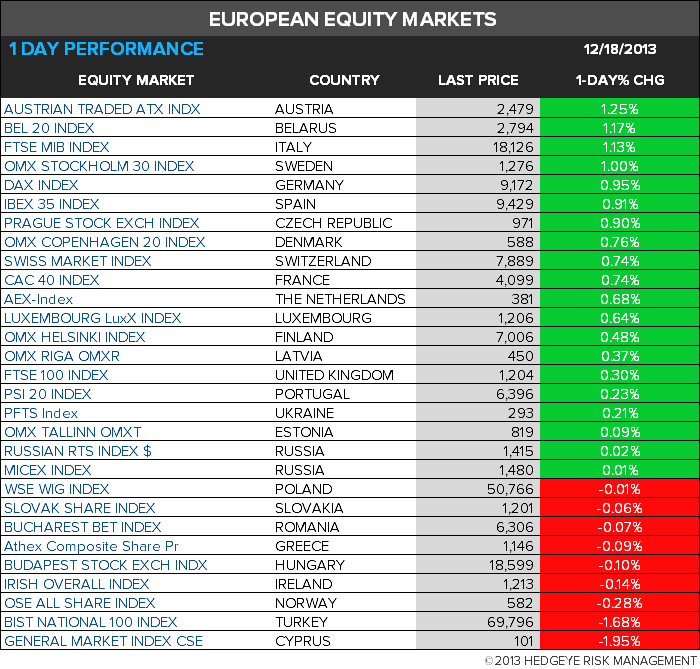

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team