This note was originally published at 8am on December 04, 2013 for Hedgeye subscribers.

“My reading of history convinces me that most bad government results from too much government.” -Thomas Jefferson

Over the Thanksgiving break, I started reading “Thomas Jefferson: The Art of Power” by Jon Meacham. For many of you Americans (like Keith I’m Canadian), undoubtedly studying the founding fathers is old hat, but for me the book has a number of revealing insights.

The key insight relates to the quote at the outset. Specifically, this idea that too much government may, in fact, be too much government. No doubt there are some pensioners in Detroit who are thinking just that as they are beginning to realize that the “government guarantee” of their pension is not as solid as they believed it to be.

Like most great men, Jefferson had his faults. Regardless, the author of the Declaration of Independence was a stalwart protector of individual liberty, especially in the face of the threat of government. Compared to the Jeffersonian era, the individual American certainly has much broader freedoms than he, and especially she, would have had in the early 1800s.

The one caveat to this of course is in the area of economic freedom, specifically taxation. From the Jeffersonian period to the early 20th century, the government was both a small percentage of the economy and direct taxation was originally very limited. On the last point, as recently as 1895 the Supreme Court of the United States actually ruled that federal income tax was unconstitutional.

Today as we “gladly” hand over 1/3+ of our incomes to the federal government and the government comprises 20%+ of the economy, it certainly begs the question of whether we have the personal economic freedoms that our Founding Fathers envisioned.

Back to the global macro grind . . .

Related to the topic above, one sneaky macro positive that has been emerging domestically is a shrinking of the federal budget deficit. Over the past four years, the federal budget deficit has been cut in half from the peak level of $1.4 trillion. Certainly, a $700-ish billion budget deficit is still too large, but in this regard the trend is definitely our friend, especially as it relates to U.S. dollar tailwinds.

Sadly, none of today’s current politicians have the political acumen of Thomas Jefferson, so the primary method to halt federal government spending growth has been for the Tea Party to effectively hijack the government, which most recently led to a government shutdown.

In 2014, we may have déjà vu all over again. Consider the federal government catalysts we have in front of us in the next three months:

- December 13th – The bipartisan budget committee is supposed to report back on budget / compromise progress;

- January 15th – The Current Continuing Resolution runs out; and

- February 7th – The next debt ceiling deadline. . .

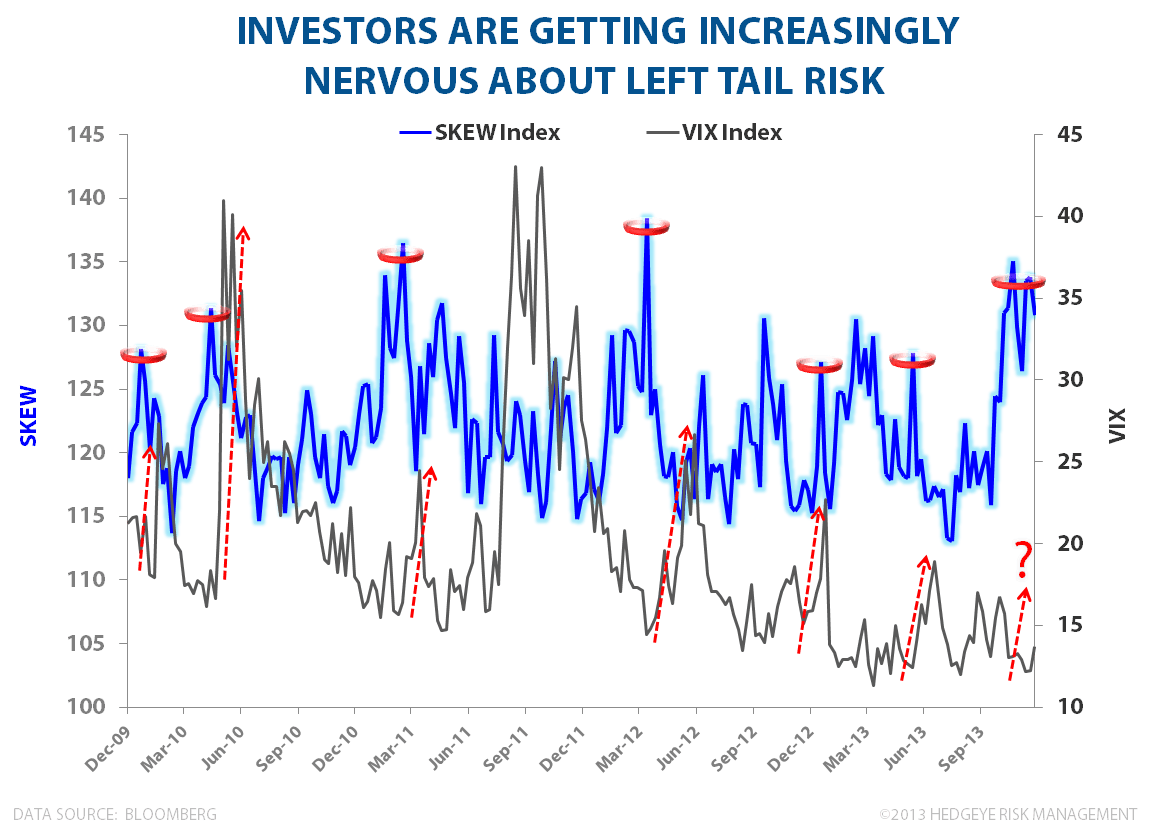

The threat of more negative government catalysts is actually coming at a really complacent and inopportune time for the U.S. equity markets. Specifically, the VIX’s monthly average price was just under 13 in November and at the lowest level we’ve seen in over two years. As many of you well know, there is an inverse correlation between the VIX, a measure of volatility, and the price of the SP500. Suffice it to say, the equity volatility ball is sufficiently under water . . .

In the Chart of the Day, we highlight the SKEW Index compared to the VIX index. As the chart shows, SKEW is spiking and historically SKEW has been a decent leading indicator of volatility. Intuitively this makes sense as investors are becoming more compelled to hedge exposure given the highs in the market and the fact that year-end is fast approaching.

A potential spike in volatility and decline in equities also makes sense given a number of other signs of a near term top.

Consider a couple of headlines from the Wall Street Journal and Reuters from yesterday:

- “More Hedge Funds Turn to Long-only Strategies”

- “Short Sellers Trying to Cope”

No doubt, this has been a challenging year for short sellers as stocks with high short interest have outperformed meaningfully, but when more than half of hedge funds launch or plan to launch long only strategies it does reek of capitulation. (And no, the Hedgeye Long Only ETF won’t be launching anytime soon!)

Before signing off, I also wanted to remind you of Hedgeye’s Energy Best Idea call on Boardwalk Partners (BWP) this Thursday at 11am. BWP is a $6.4 billion market cap MLP primarily engaged in the transportation and storage of natural gas in the south/central US. The diversified holding company Loews Corp. (L) owns the 2% GP interest in BWP, all IDRs (currently in the 50/50 split), and 52% of the BWP’s outstanding common units.

BWP is a high-conviction short idea given the Company’s deteriorating base business, aggressive accounting, high leverage, unsustainable distribution, valuation. If this thesis sounds a little like our calls on Kinder Morgan (KMP) and Linn Energy (LINE), it should. We think the valuation of the MLP sector is grossly overstating the intrinsic value of the underlying businesses held in these structures. If you’d like to get access to the call, email sales@hedgeye.com.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research