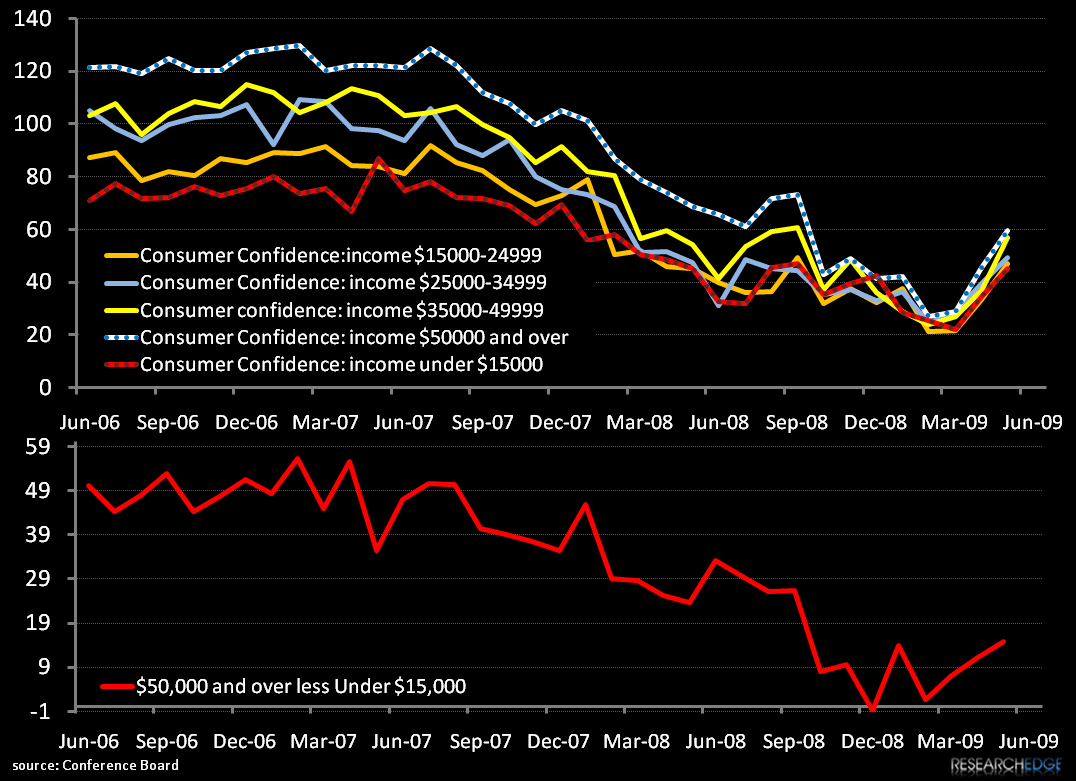

My colleague Andrew Barber just floated me the following consumer confidence chart. These are Conference Board numbers, so they are not proprietary to us, but note 2 things... 1) Not only has confidence in aggregate popped since the market rally, but 2) it has disproportionately impacted higher incomes.

Thanks for stating the obvious McGough... not many people making $15k per year on stocks never mind feel more confident in the face of a market move. But obvious or not, a fact is a fact. We can't ignore it.