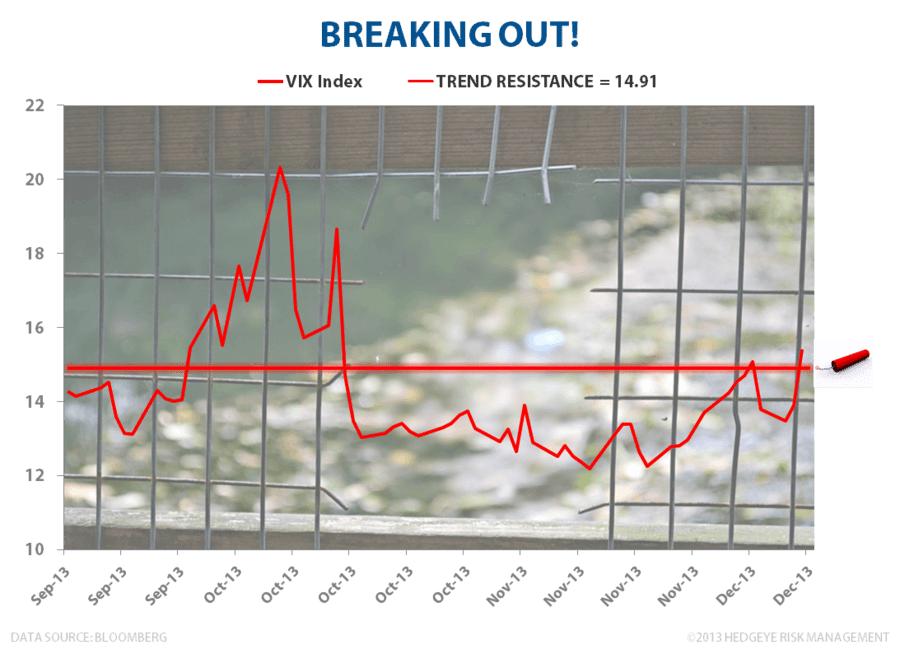

Equity volatility starting to look primed to breakout into 2014.

After making a series of higher-lows since August, front month VIX (volatility) broke out above our Hedgeye TREND resistance of 14.91 yesterday.

Fed confusion is going to breed contempt.

This equity market is as complacently positioned as I have seen it in six years. Yesterday’s II Bull/Bear survey hit a fresh year-to-date high of +4390 basis points to the Bull side!

Editor's note: This a complimentary excerpt from Hedgeye CEO Keith McCullough's research this morning. Click here for more information on you can subscribe to Hedgeye research.