TODAY’S S&P 500 SET-UP – December 11, 2013

As we look at today's setup for the S&P 500, the range is 30 points or 0.98% downside to 1785 and 0.69% upside to 1815.

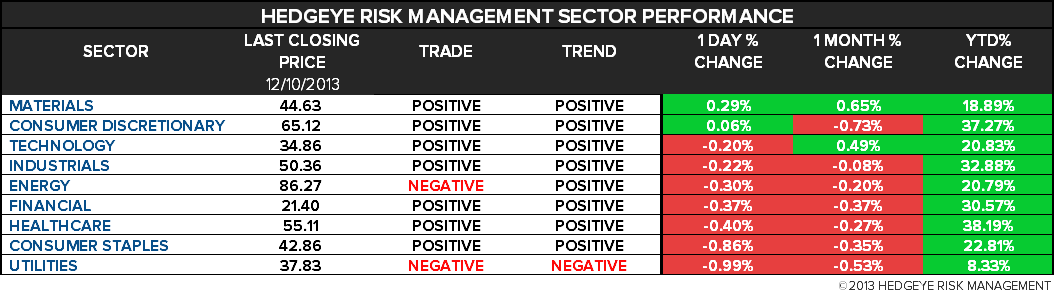

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.51 from 2.50

- VIX closed at 13.91 1 day percent change of 3.11%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Dec. 6 (prior -12.8%)

- 10:30am: DOE Energy Inventories

- 11am: Fed to purchase $1.25b-$1.75b in 2036-2043 sector

- 1pm: U.S. to sell $21b 10Y notes in reopening

- 2pm: Monthly Budget Statement, Nov., est. -$140b

GOVERNMENT:

- 8:30am: NTSB holds investigative hearing on crash landing of Asiana Airlines flight 214 at San Francisco Intl Airport

- 9:15am: Senate Finance Cmte reconvenes confirmation hearing on John Koskinen to take over as chief of IRS

- 10am: House Energy and Commerce Cmte panel hears from HHS Secretary Kathleen Sebelius on Affordable Care Act

- 10am: Senate Environment Cmte hears from EPA, Energy, Dupont on renewable fuels standard and ethanol

- 10am: Michael Gibson, director of Fed bank supervision, speaks at panel discussion on insurance industry in Washington

- 1pm: House Ways and Means panel holds hearing on identity theft, with acting IRS Commissioner Daniel Werfel

- 3pm: House Armed Services Cmte panel hears from Congressional Research Service on People’s Liberation Army

WHAT TO WATCH:

- U.S. budget negotiators reach deal easing spending cuts

- EU finance chiefs set creditor-writedown rule parameters

- FCC set to approve in-flight calls as Congress resists

- NSA using Google cookies to pick hacking targets: Wash. Post

- Costco net misses ests. as warehouse chain boosts discounts

- MasterCard to buy back $3.5b in shrs, boosts qtrly div 83%

- Foxconn may start funding startups for wearable technologies

- Chinese drugmakers may see increased FDA scrutiny

- IEA raises 2014 global oil demand forecast on U.S. recovery

EARNINGS:

- Hudson’s Bay (HBC CN) 7am, $0.10

- Joy Global (JOY) 6am, $1.12 - Preview

- Laurentian Bank of Canada (LB CN) 8:40am, $1.31

- Men’s Wearhouse (MW) 5:30pm, $0.86

- Nordson (NDSN) 4:30pm, $0.94

- Oxford Industries (OXM) 4pm, $0.11

- Vera Bradley (VRA) 4:03pm, $0.33

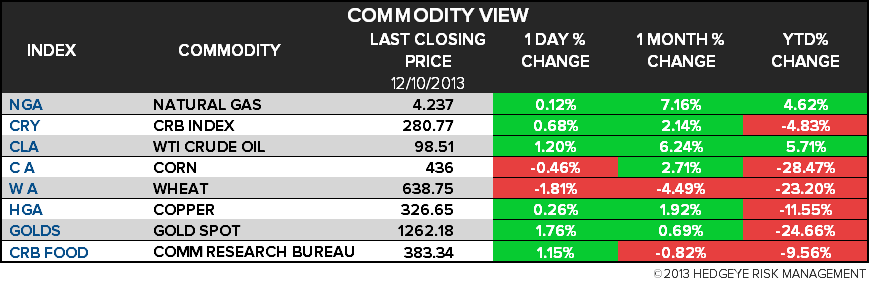

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- IEA Boosts 2014 Global Oil Demand Forecast on U.S. Recovery

- Gold Retreats From Three-Week High as Investors Weigh Rally, Fed

- Colombian Rebels Seen Blocking Farmland Overhaul: Commodities

- Coffee Spread Falls From Record on Vietnam Sales; Cocoa Retreats

- Nickel Leads Metals as Investors Add to Bets on Higher Prices

- WTI Trades Near Six-Week High; IEA Boosts 2014 Demand Estimate

- Wheat Rebounds From 18-Month Low as Demand to Gain After Drop

- Thailand to Reinstate Natural Rubber Exports Fee From January

- Chinalco Copper Output Cuts Set To Help Trim Global Surplus

- U.S. Sees Least Volatile Oil Prices in 17 Years: Energy Markets

- Solar Boom Boosts South Africa Salaries With 25% Jobless: Energy

- Wall Street Exhales as Volcker Rule Seen Sparing Market-Making

- Sugar Rout Deepening on Weaker Real, Thai Baht: Chart of the Day

- Robusta Coffee Seen Dropping as Vietnam Sales Set to Accelerate

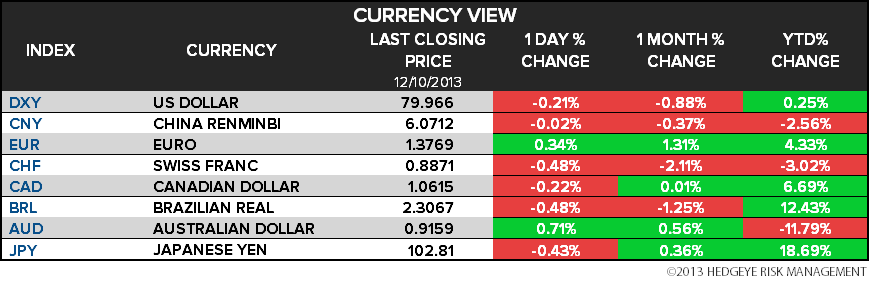

CURRENCIES

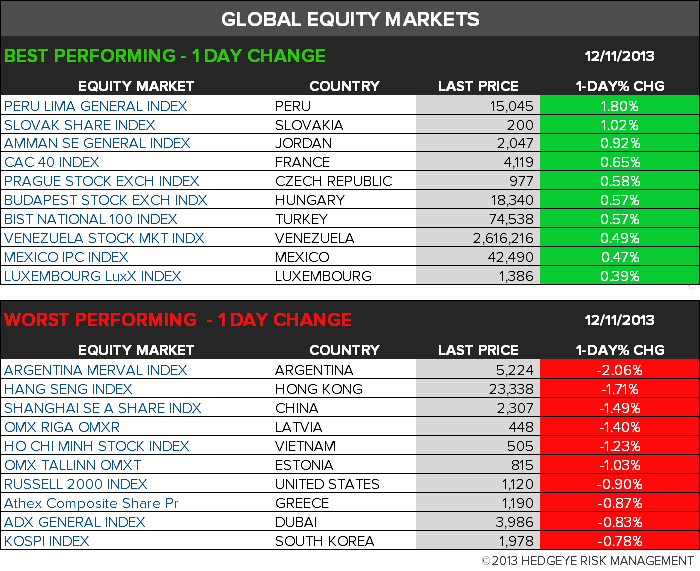

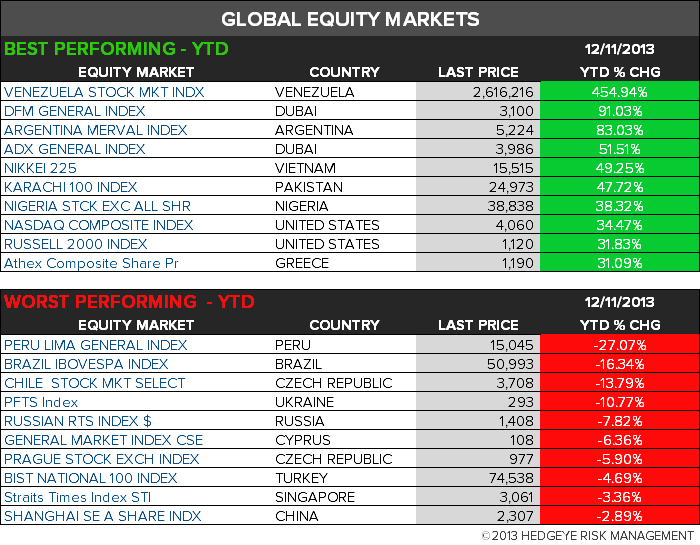

GLOBAL PERFORMANCE

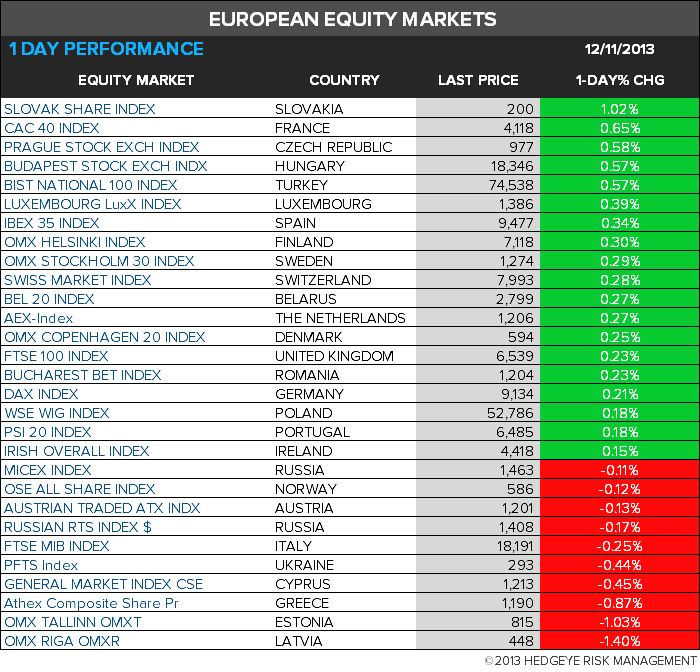

EUROPEAN MARKETS

ASIAN MARKETS

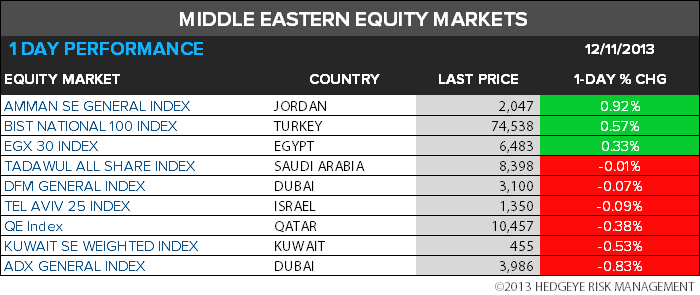

MIDDLE EAST

The Hedgeye Macro Team