We've never seen the Street more bearish on RH -- especially headed into a print. We find that interesting, if not perplexing, given that there should be such a positive change in fundamentals with the upcoming quarter. We still think RH is on its way to $175. The quarters will ebb and flow. But despite the bearish sentiment we like it into the 3Q print.

Consider the following

Last quarter -- when RH was flirting with $80...

- RH missed the comp -- coming in at 'only' 26% versus expectations of something well into the 30s.

- RH continued its string on new business announcements -- but instead of announcing businesses that are actually commercially viable, it came out and announced that it would start RH Music and RH Hotels (whereby it would outfit a small number of niche hotels with RH garb). The company made a mistake in announcing these -- even though it only cost them about $5mm annually out of the $35mm they saved by not producing the Fall sourcebook -- it was really more of a marketing initiative than a new business initiative. All they succeeded in doing is scaring the lights out of Wall Street about their strategic direction.

- Gross Margins were off by 253bps, the biggest decline RH experienced since 2009 -- when it was in the tank.

- They announced the elimination of the Fall sourcebook -- which caused a not-so-minor freak out by investors who were concerned that the company's Direct (non-store) business -- which is about 47% of total -- would start to evaporate.

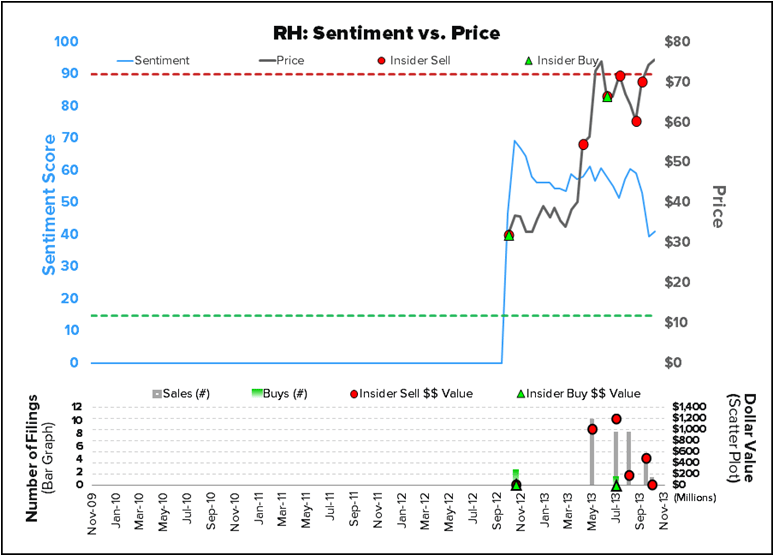

- Shortly after the print, the three 'founding shareholders' who took it private and subsequently public all sold out simultaneously (the structure of the deal required that they all move in tandem).

- Then as a kicker there was one extremely bearish sell-side initiation with a Sell rating due to structural reasons -- arguments that we think are weak at best (we'll debate them anytime). Then earlier this week, another firm was out talking about how weaker ComScore data suggested that dot.com sales were falling.

Package that all together, and it's easy to see why sentiment is so poor.

But here why we're more optimistic…

- We think comp will accelerate meaningfully this quarter -- from 26% to something well north of 30%. The company did not articulate as well as it should have that comps were weak because it simply did not have enough inventory. Part of that was that product was on the water for 2-4 weeks longer than expected, and as such they could not recognize revenue. That revenue will show up in 3Q. Is the supply chain issue fixed? No. That will take the better part of a year. But we're convinced that the problem has not gotten worse, and in fact has started to improve.

- Gross Margins should improve dramatically this quarter -- from -253bps last quarter to better than -100bp this quarter. We would not be surprised to see it closer to flat.

- As it relates to dot.com, we're simply not as concerned as everyone else seems to be. We think that the following chart flies in the face of those who think that the elimination of the sourcebook hurt revenue. Specifically, it shows the traffic trend at RH over the past six months. To be clear, you want to have a declining traffic rank (Facebook is #1, Nike is 972, and Saucony is 77,500). The point here is that RH.com's traffic rank improved consistently from 15,000 down to 10,000 over the time period that people are worried that RH's web business dried up.

THIS IS THE CORRELATION BETWEEN SOURCEBOOK MAILINGS AND REVENUE -- NADA

HERE'S WHAT 1,000 PEOPLE TOLD US ABOUT WHAT WHAT THEY DO WITH CATALOGS. THEY DON'T DO MUCH.

Sentiment for RH is just about as low as it's ever been -- despite the fact that fundamenals are getting better on the margin, and we’re inching closer to the period (in 12 months) when square footage should start to accelerate.