Draghi Backstop In Place, EUR/USD grinds higher

After a very surprising 25bps cut to the main interest rate at its last meeting on 11/7, the ECB kept rates on hold today, as expected by consensus forecasts. We actually saw no need to use the monetary “powder” last month given the improving economic data across the region supporting our Q4 macro theme call of #EuroBulls. (For more see our note titled “Just Charts - #EuroBulls”).

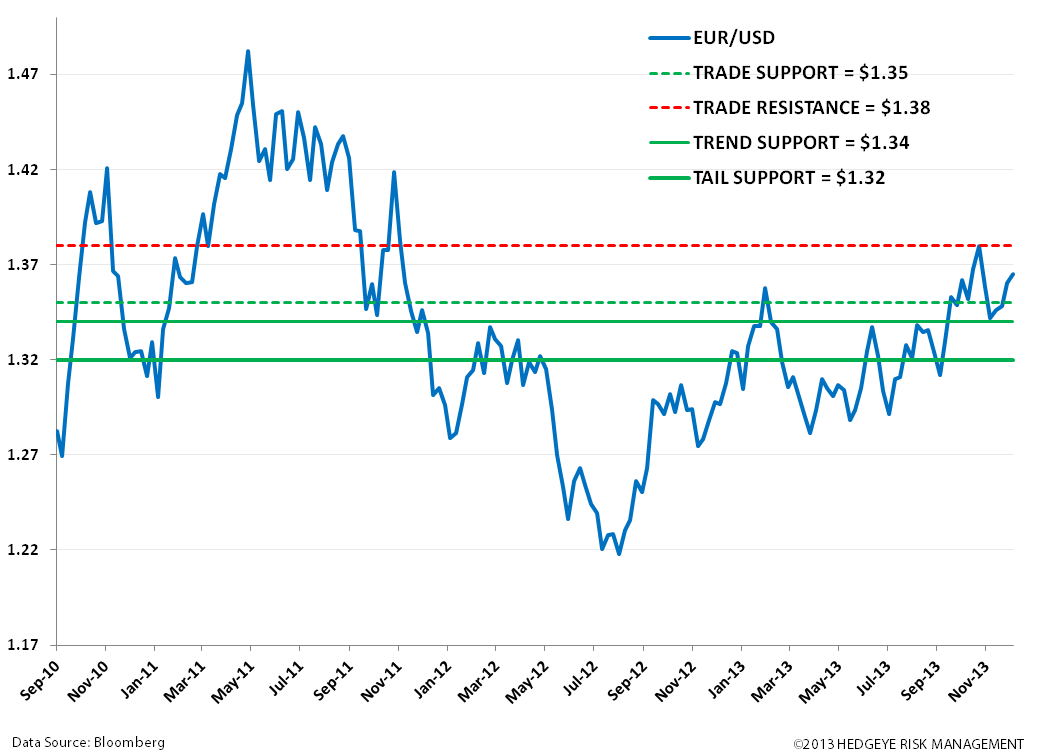

We expect the ECB’s accommodative stance to continue to support both equities and the common currency. Our preference is German equities (via the eft EWG); we also like the EUR/USD (etf FXE), which got a lift following today’s announcement. Our quantitative levels are included in the chart below.

Press Conference Details

- No material change to the economic and inflation assessment or outlook (Dec. Projections below). Mario Draghi says fiscal consolidation measures at the country level should be “growth friendly” and to expect a prolonged period of low inflation, followed by inflation rates close but below 2%

- Continued mantra that monetary policy will remain accommodative for as long as necessary and to expect key ECB interests rates at present or lower levels for an extended period of time

- On non-standard measures, Draghi noted that a negative deposit rate was briefly discussed

- On the use of non-standard measures Draghi said the Bank is “ready and willing to act within the forward guidance framework” and is considering numerous options, if needed

- On the issuance of another LTRO, Draghi made a point to note that first LTROs were successful given the level of uncertainty around when they were issued two years ago. However, he said if a similar operation were to be issued, the framework must assure it’s being used to extend credit to the real economy, and not used to subsidize capital formation (carry trade operations) by the institutions.

To read a copy of Draghi’s prepared remarks click here.

ECB’s December Macroeconomic Projections

GDP: -0.4% in 2013 (unch vs Sept.); +1.1% in 2014 (revised up 10bps); +1.5% in 2015 (unch)

CPI: +1.4% in 2013 (revised down -10bps vs Sept.); +1.1% in 2014 ( revised down -20bps); and +1.3% in 2015 (unch)

UK Fiscally Strong; Growth Projections Push Higher:

As we expected, the BOE kept the main interest unchanged at 0.5% and the asset purchase program (QE) target unchanged at £375B. We continue to be bullish on the UK economy, the GBP/USD, and UK equity market (via the etfs FXB and EWU, respectively). For more see our note titled “Just Charts - #EuroBulls”).

Additionally, today Chancellor of the Exchequer George Osborne presented his Autumn Statement. In it, he revised many economic forecasts (versus a prior March forecast) that point to an improved outlook, and supportive of our bullish outlook on the GBP/USD (via the etf FXB) and UK equities (etf EWU).

GBP/USD Levels

Forecast Updates:

2013

- GDP +1.4% vs prior +0.6%

- CPI +2.6% vs prior +2.8%

2014

- GDP +2.4% vs prior +1.8%

- CPI +2.3% vs prior +2.4%

2015

- GDP +2.2% vs prior +2.3%

- CPI +2.1% vs prior +2.1%

- 2015 unemployment rate at 7.0% in 2015 declining to 5.6% in 2018

- Budget deficit forecasts as % GDP lower and will run a small surplus in 2018/19

- Pension age raised to 68 in the 2030s and 69 in the late 2040s

- Bank levy raised to 0.156% from 0.13% from Jan-14; raises £2.7B and £2.9B in next two years

- Will introduce a new tax allowance for investment in shale gas

- Foreigners who sell second homes in the UK will have to pay capital gains tax

To read a copy of Osborne’s Autumn Statement 2013 speech click here.

Matthew Hedrick

Associate