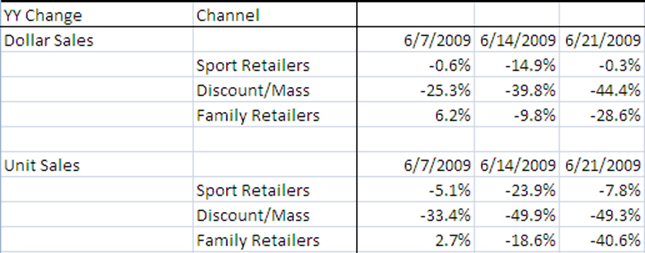

Slightly better SportscanINFO numbers last week, but the headline is deceiving. There was a marked improvement in the athletic specialty channel, but additional weakness in mass and family channels. That drop-off is so severe that any sane analytical mind needs to question the validity of the data.