TODAY’S S&P 500 SET-UP – December 5, 2013

As we look at today's setup for the S&P 500, the range is 23 points or 0.27% downside to 1788 and 1.01% upside to 1811.

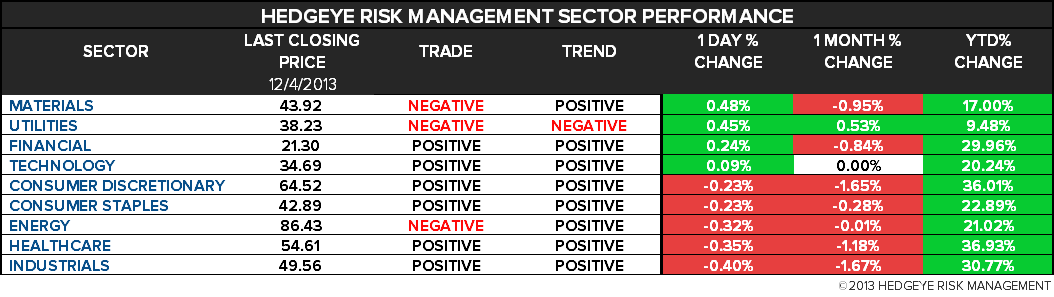

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.53 from 2.55

- VIX closed at 14.7 1 day percent change of 1.03%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: BOE seen maintaining benchmark lending rate of 0.5%

- 7:30am: Challenger Job Cuts y/y, Nov. (prior -4.2%)

- 7:30am: RBC Consumer Outlook Index, Dec. (prior 47)

- 7:45am: ECB seen holding benchmark interest rates at 0.25%

- 8:15am: Fed’s Lockhart speaks in Fort Lauderdale, Fla.

- 8:30am: ECB’s Draghi holds news conference on interest rates

- 8:30am: Init. Jobless Claims, Nov. 30 est. 321k, (pr 316k)

- 8:30am: Revised 3Q GDP q/q, est. 3.1% (prior 2.8%)

- 9:45am: Bloomberg Consumer Comfort, Dec. 1 (prior -33.7)

- 10am: Factory Orders, Oct., est. -1.0% (prior 1.7%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 11am: U.S. to announce plans for sale of 3Y notes, 10Y notes and 30Y bonds

- 11am: Fed to buy $1.25b-$1.75b in 2036-2043 sector

- 12:15pm: Fed’s Fisher speaks in College Station, Texas

GOVERNMENT:

- 8:30am: Treasury Sec. Jack Lew to speak on financial reform at Pew Charitable Trusts

- 9am: EPA hearing on 2014 standards for Renewable Fuel Standard

- 9:30am: SEC roundtable on proxy firms used by investment advisers

WHAT TO WATCH:

- China Mobile moves closer to iPhone with 4G network license

- GM to pull Chevrolet from Europe to focus on expanding Opel

- Nov. comp. sales may gain on Y/y comparisons, holiday deals

- Goldman Sachs sued by Singapore client Oei over trading loss

- Volcker rule won’t allow portfolio hedging for banks: WSJ

- China bans financial companies from Bitcoin transactions

- Alibaba will probably prefer London listing over Nasdaq: Times

- Microsoft to expand encryption to protect against spying

- Icahn plans shareholder vote pushing Apple to boost buyback

- Merck KGaA to acquire AZ Electronic Materials for $2.6b

- BNP agrees to buy Rabobank’s Polish unit BGZ for $1.4b

AM EARNINGS:

- Canadian Imp. Bank of Comm (CM CN) 5:30am, C$2.15 - Preview

- Cantel Medical (CMN) 8am, $0.24

- Conn’s (CONN) 7am, $0.64

- Dollar General (DG) 7am, $0.70 - Preview

- Dollarama (DOL CN) 7:30am, C$0.88

- Francesca’s Holdings (FRAN) 7am, $0.20

- Jos A Bank Clothiers (JOSB) 6am, $0.50

- Kroger (KR) 8:30am, $0.53 - Preview

- Methode Electronics (MEI) 6:30am, $0.35

- Royal Bank of Canada (RY CN) 6am, C$1.40 - Preview

- Toro (TTC) 8:30am, $0.03

- Toronto-Dominion Bank (TD CN) 6:30am, C$1.99 - Preview

- Transcontinental (TCL/A CN) After open, C$0.74

- UTi Worldwide (UTIW) 8am, $0.08

PM EARNINGS:

- Cooper (COO) 4:01pm, $1.80

- Esterline Technologies (ESL) 4pm, $1.78

- Finisar (FNSR) 4pm, $0.39

- Five Below (FIVE) 4:01pm, $0.05

- Ulta Salon (ULTA) 4pm, $0.74

- Veeva Systems (VEEV) Aft-mkt, $0.05

- Zumiez (ZUMZ) 4pm, $0.46

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Brent Seen Over $100 for Fourth Year as OPEC Bets on Demand

- Banks Cut Raw-Materials Staff to Fewest Since ’09: Commodities

- Indonesia to Press Ahead With Ore-Export Ban in ’14, Wacik Says

- Gold Drops in London on Speculation of Federal Reserve Tapering

- Cocoa Drops as Ivorian Arrivals Signal More Supply; Coffee Rises

- Eni’s Scaroni Says Had Long, Warm Meeting With Iranian Minister

- Rebar Falls From 7-Week High on Ore Inventory, Freezing Weather

- OPEC Maintains Output Quota; Will Member Countries Toe Line?

- Coffee Cost Surge in Vietnam Seen Curbing Plantation Investment

- Goldman Sachs Antitrust Suits Over Aluminum Set for Venue Debate

- World Food Prices Little Changed in November, Oils Jump, UN Says

- Glasenberg Raises Glencore’s Bet on Coal as BHP Pauses: Energy

- Iran, Libya Have Capacity to Raise Oil Output If Tensions Ease

- WTI-Brent Spread Shrinks to 10-Day Low as U.S. Supply Declines

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team