Holiday discounting, recovery, and Royal Caribbean outperformance.

Apparently, CCL/ NCLH engaged in some aggressive promotional discounting through Thanksgiving weekend. However, at least CCL recovered post weekend in the slow bookings period before Wave. The Royal Caribbean brand was the standout in our latest survey but the picture is mixed for RCL’s other major brand, Celebrity. In Europe, Summer 2014 looks encouraging. Please read on for details.

Below are some observations from our proprietary pricing survey (>12,000 itineraries) for CCL, RCL, and NCLH. We analyze YoY pricing, as well as sequential trends which is determined by comparing pricing relative to the last earnings/guidance date for a cruise operator i.e. CCL: 9/24; RCL: 10/24; NCLH: 10/28. For a more in-depth and quantitative analysis, please contact sales at .

MAJOR TAKEAWAYS FROM LATEST SURVEY:

- CCL: Volatile pricing by Carnival brand due to Thanksgiving week promotions

- RCL: RC brand showing healthy pricing gains for FQ1 but mixed picture for Celebrity

- NCLH: Continues to discount Caribbean pricing due to increased competition

CCL ANALYSIS

NORTH AMERICA

- For their Thanksgiving Week promotion, Carnival brand lowered pricing for Summer 2014 double digits relative to early November for the Caribbean and Mexico

- Pricing surged back post the weekend promotion with pricing for 2Q/3Q nicely higher

- Alaska pricing is mostly steady

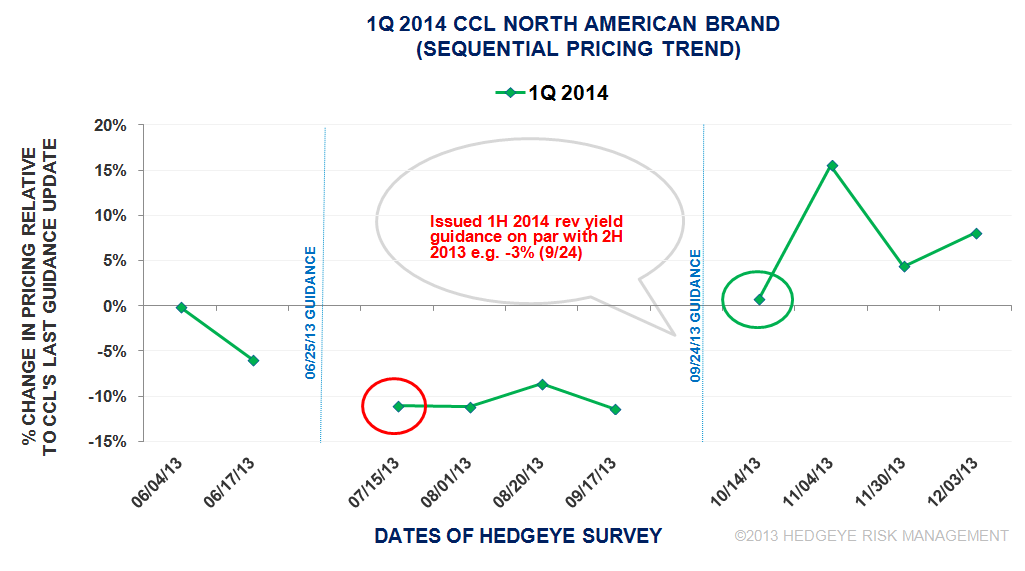

CCL North American Brands - FQ1 sequential chart:

F1Q sequential pricing remained higher relative to late September. We saw a bearish pricing trend (red circle) in mid-July as pricing deteriorated significantly relative to pricing seen in late June. A bullish pricing trend (green circle) emerged in mid-October as pricing broke the downtrend seen in the past few months and was actually slightly positive relative to pricing seen in late September.

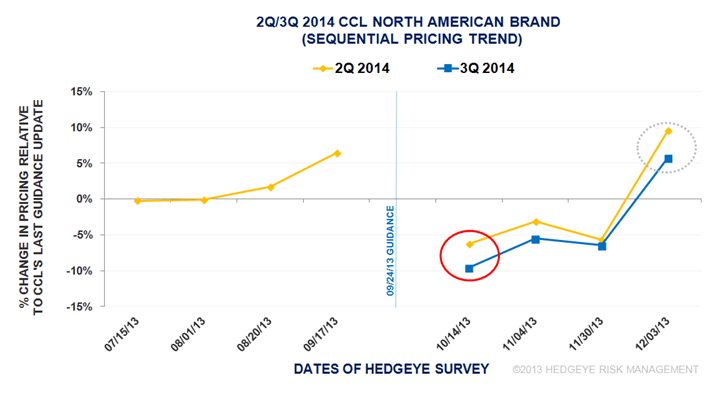

CCL North American Brands - FQ2/FQ3 sequential chart:

For very early Summer 2014 itineraries, we saw weak sequential pricing in mid-October, which continued into Thanksgiving weekend. Pricing strongly recovered immediately after Cyber Monday. It remains to be seen whether the higher pricing is sustainable heading into Wave Season. We look for the next pricing survey for bullish confirmation.

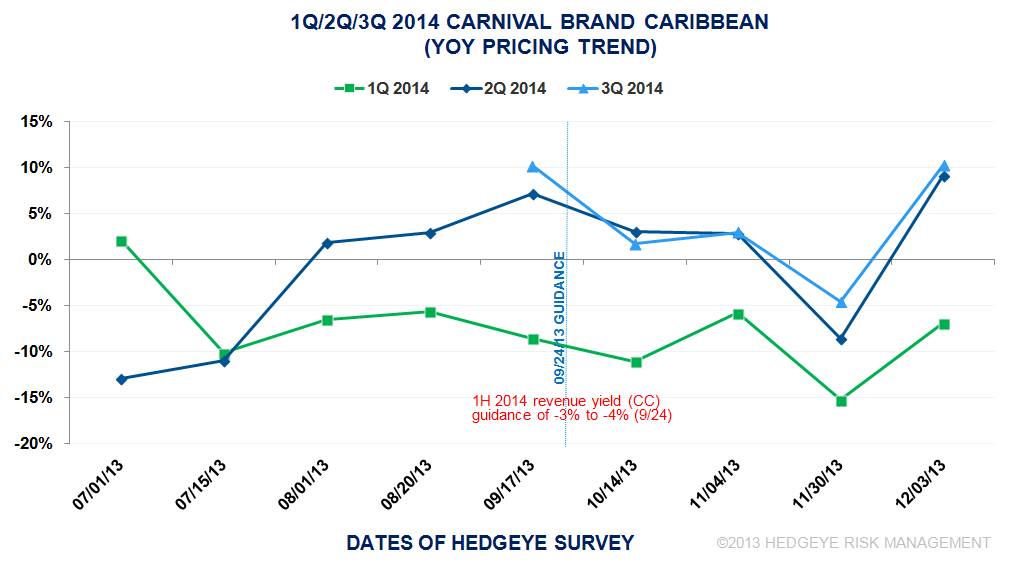

Carnival Brand (Caribbean) - F1Q/2Q/3Q YoY change chart:

On a YoY basis, mainly due to difficult comps, F1Q pricing continued to be lower for the Carnival brand in the Caribbean. However, in early December, F2Q/F3Q showed the strongest YoY pricing performance yet.

EUROPE

- Costa

- Weak FQ1 2014 European pricing remains but FQ1 has the lowest capacity by quarter for the year

- Modestly higher pricing for FQ2-FQ4

- AIDA

- Weakness in Eastern Med/Western Europe offset by better performance in Western Med

- Overall 2014 sequential pricing is a tad lower

- Cunard

- Improvement in FQ2 pricing offset by weaker FQ3 pricing

RCL ANALYSIS

CARIBBEAN

- RC brand

- FQ1 pricing has reversed into positive territory

- Flat pricing for FQ2/Q3, with sequential trend slightly positive

- Celebrity

- Modest discounting for FQ1 relative to early November

- Modestly higher pricing for FQ2

- Pullmantur

- Pricing is mostly steady

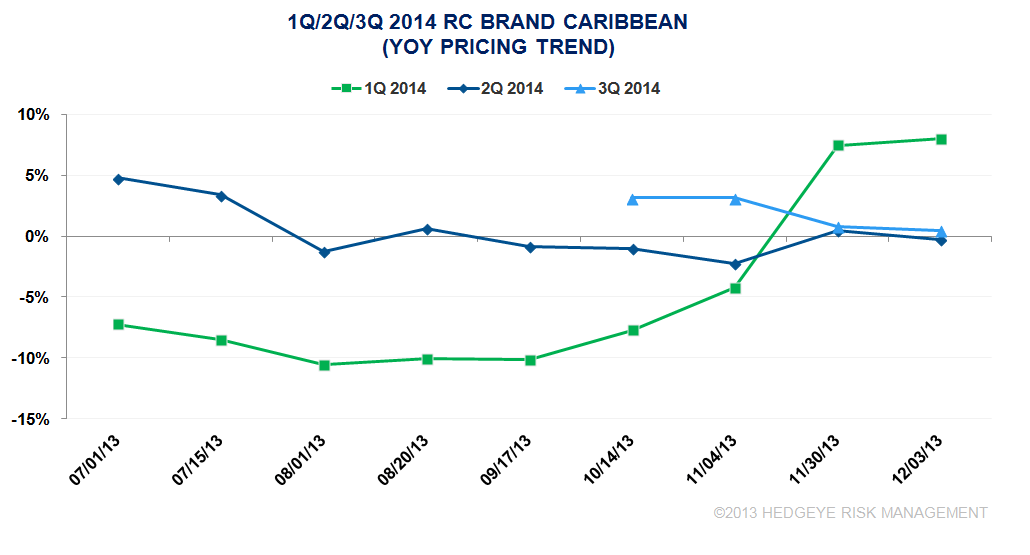

Royal Caribbean Brand (Caribbean) - F1Q/F2Q/F3Q YoY pricing chart

F1Q pricing is now modestly higher while F2Q/F3Q pricing has flatlined.

EUROPE

- RC brand

- Solid pricing for RC brand

- Celebrity

- Flat pricing for FQ2 but significant discounting for FQ3

- Pullmantur

- Pricing has finally stabilized

OTHER

- Alaska: RC brand weakness offset by Celebrity (ex Millennium) strength

- South America quite robust

NCLH ANALYSIS

CARIBBEAN

- Pricing lower during promotional period but not as aggressive as Carnival

- Pricing remained lower following holiday week, particularly for FQ1 2014

EUROPE/ALASKA/HAWAII

- Steady 2014 pricing