EVENTS TO WATCH OVER THE NEXT 24 HOURS

Hedgeye Black Friday Consumer Survey: Focus on JCP. We'll be conducting a follow-up to our prior consumer survey (which helped us call a JCP beat and KSS miss) following Black Friday weekend and Cyber Monday. We'll have results next week, and will have an updated presentation accordingly. If you are interested in our results, please email sales@hedgeye.com, or .

ARO - Earnings Call: Wednesday (12/4) 4:15 pm

GES - Earnings Call: Wednesday (12/4) 4:30 pm

WTSL - Earnings Call: Wednesday (12/4) 5:00 pm

FRAN - Earnings Call: Thursday (12/5) 8:30 am

SKX - Analyst and Investor Meeting: Thursday (12/5) 9:30 am

HBI - ISI Group Consumer Holiday Conference: Thursday (12/5) 9:30 am

DG - Earnings Call: Thursday (12/5) 10:00 am

ECONOMIC DATA

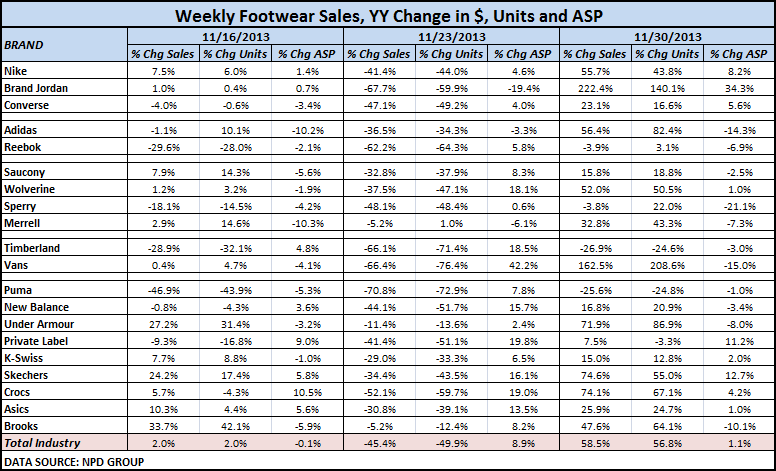

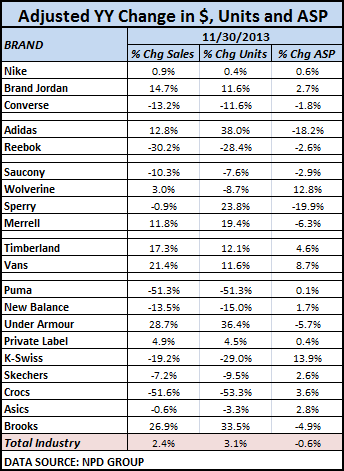

Weekly Athletic Footwear Data

COMPANY NEWS

JCP - J. C. PENNEY COMPANY, INC. PROVIDES HOLIDAY UPDATE

(http://ir.jcpenney.com/phoenix.zhtml?c=70528&p=irol-newsCompanyArticle&ID=1881648&highlight=)

- "J. C. Penney Company, Inc. today provided a preliminary update on the Company's performance for the fiscal month ending November 30, 2013. During that period, which includes the important Thanksgiving weekend, the Company's comparable store sales grew 10.1 percent over last year. The Company also noted that its e-commerce sales through jcp.com continued to be strong, running well ahead of last year, consistent with last month's trend."

Takeaway: See our note "JCP The Bear Case Lacks Intellectual Honesty"

WMT - Walmart.com Has its Best Sales Day Ever on Cyber Monday 2013

- "Walmart today announced that Cyber Monday 2013 was the biggest online sales day in its history. The five-day period from Thanksgiving to Cyber Monday is the highest five-day stretch in online sales for the retailer to date, and Walmart.com processed more than 1 billion page views during that period."

Takeaway: It's kind of funny…every retailer will cherry pick the highlights and report them to the world. The bad news gets stifled. At least Wal-Mart had SOMETHING good to say -- even though it had nothing to do with store sales over Black Friday weekend. JCP had good news. So far, crickets from the rest of US retail.

ANF - Engaged Capital Tells Abercrombie: Replace CEO

(http://online.wsj.com/news/articles/SB10001424052702304355104579235882032904384)

- "Engaged Capital said in a letter to the Abercrombie board that it should start looking for a replacement for chairman and chief executive Michael Jeffries, whose employment contract expires Feb. 1."

- "The hedge-fund firm, which said it owns about 0.5% of Abercrombie's stock, also said the sale of Abercrombie to a private-equity buyer 'may represent the best option for shareholders.'"

- "Abercrombie on Tuesday said it welcomed 'input from all shareholders' and that it had held 'extensive discussions' with many shareholders, including Engaged Capital, over the past several months."

Takeaway: We hope they succeed. We've been tempted to get involved with ANF over the years, but the fact that Jeffries is still CEO has repeatedly held us back. It's rare to see one person destroy significant equity value at a company, but that's the one area where Jeffries has succeeded.

HMB - H&M Sport to Compete in Activewear

- "The Swedish high-street retailer will reveal today that it is launching H&M Sport, an expanded concept with a new visual identity, on Jan. 2 in all its markets worldwide."

- "Dedicated areas in selected stores will feature activewear and accessories including windproof and water-repellent running jackets; warm-up tops and trousers for working out; comfortable garments for yoga; tennis shorts, and protective fleece jackets for outdoor activities."

- "H&M signaled its intention to deepen its sportswear offering earlier this year when it said it would dress Sweden’s athletes for the Winter Olympics and Paralympics in Sochi, Russia, next year and the Summer Olympics and Paralympics in Rio de Janeiro in 2016."

Takeaway: So many retailers are hopping on the Athletic bandwagon. Heck, you can buy yoga apparel at Whole Foods now. Nike and UnderArmour have been dealing with this for a long time. But Lululemon better keep an eye on the price gap between its Down Dawgs and what the H&M's of the world are offering.

SHLD - Filing Reveals Edward Lampert's Stake in Sears

(http://www.wwd.com/fashion-news/fashion-scoops/still-number-one-7298342)

- "Edward Lampert, Sears Holdings Corp.’s chairman and chief executive officer, pared his stake in the company over the last few months and no longer controls the majority of its shares, but the pruning job was relatively modest."

- "In a regulatory filing Tuesday, Lampert and his various investment vehicles, including ESL Partners LP, were listed as owning 51.6 million shares of Sears stock, 48.4 percent outstanding. That’s down from the 58.9 million shares, or 55.4 percent, listed in March. The reduction was caused by distributions to ESL investors."

Takeaway: Perhaps this is a complete non-event if it was simply a distribution to ESL Investors. But if there was any part that was driven by his desire to downside his stake, then it would be catastrophic to SHLD. In fairness, Lampert is savvy enough to not let that happen.

AEO - American Eagle Inks Overseas Deals

(http://www.wwd.com/retail-news/specialty-stores/american-eagle-inks-overseas-deals-7298239)

- "American Eagle Outfitters Inc. is expanding its presence in the Americas and in Asia-Pacific. The teen retailer has signed three new licensing agreements for stores that are set to begin opening in time for back-to-school in 2014."

- "According to Simon Nankervis, senior vice president for the Americas and global licensing, one agreement is with Grupo David Enterprises. That contract covers Venezuela, the Caribbean Islands and, in Central America, the countries of Panama, Costa Rica, Honduras, Guatemala, El Salvador, Nicaragua and Belize."

- "A separate agreement was signed with Grupo Comercializadoras for Colombia. In Asia-Pacific, the retailer signed an agreement with Pacifica Lifestyle Co. for stores in Thailand."

- "All agreements are for two, five-year tranches. Each agreement also allows the licensing partner to open aerie concept shops-in-shop or side-by-side stores...While many of the stores in the U.S. are about 7,000 square feet, Nankervis said those overseas range on average from 4,000 square feet to over 7,000 square feet, depending on location and availability of real estate."

Takeaway: American Eagle is doing the unthinkable -- taking the 'American' Eagle brand outside of America. Let's face it, the US isn't too popular on the world stage. If AEO can make this work, they definitely tack on another leg of growth to the story.

Burton - Burton Unveils U.S. Olympic Snowboard Look

- "When the 2014 Winter Olympics take place in Sochi, Russia, Feb. 7 to 23, the U.S. snowboarding team will be sporting Burton. The Vermont-based brand unveiled the original men’s and women’s designs at its flagship here Tuesday night."

Takeaway: Out of any sport in the games, the apparel that gets the greatest focus is arguably snowboarding. Burton was the first and remains the premier snowboarding brand. Though it's surprising that one of the bigger brands with deeper pockets has not stepped up and bid away the deal.

NKE - Nike starts waterfree fabric dyeing facility in Taiwan

(http://www.fibre2fashion.com/news/textiles-company-news/newsdetails.aspx?news_id=156717)

- "NIKE, Inc. celebrated the opening of a waterfree dyeing facility featuring high-tech equipment to eliminate the use of water and process chemicals from fabric dyeing at its Taiwanese contract manufacturer Far Eastern New Century Corp."

- "NIKE, Inc. has named this sustainable innovation 'ColorDry' to highlight the environmental benefits and unprecedented coloring achieved with the technology."

INDUSTRY NEWS

Visa’s Black Friday weekend online sales up 30%

(http://www.chainstoreage.com/article/visa%E2%80%99s-black-friday-weekend-online-sales-30)

New Rules to Dictate Spending Habits of China Officials

- "In what could be a further blow to luxury consumption in China, the nation’s leadership is deepening its pledge to crack down on corruption and ostentation with the release of new rules outlining how officials should avoid extravagant spending on activities ranging from overseas travel to the purchase of new vehicles."

- "With 12 chapters outlining 65 rules on how to manage funds and employ more transparent spending, the document, released last week, is extensive and is causing analysts to question whether the antigraft campaign that began nearly a year ago under the new administration of President Xi Jinping will continue to have a far-reaching impact on China’s luxury sector. Spending on luxury products has historically been bolstered by the purchase of expensive gifts between officials and business associates as bribes."