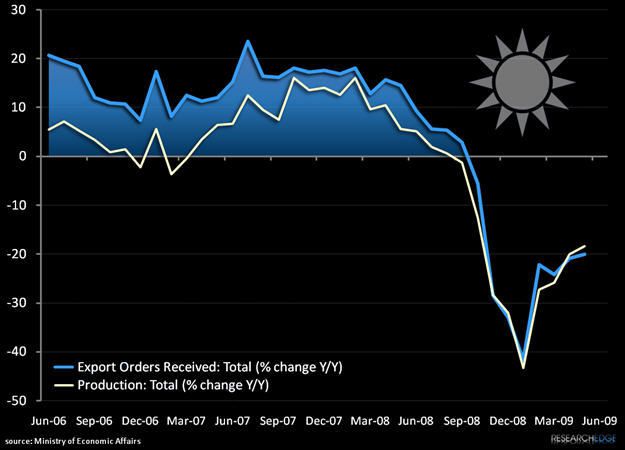

With all eyes focused on any signs of slackening demand from China, today's production and export order data from Taiwan was a disappointment. Orders declined by 20.9% year-over year, a sequential improvement from last month, while output registered at -18.31% y/y. Economists had predicted levels over 1% higher.

On a deeper dive basis, the export order data shows that "the Client's" appetite for high margin consumer electronics is demonstrating resilience, with order for electronic products in general improving sequentially to -11.33% while information and communication products have improved to -11.9% Y/Y (an increase of over 30% on a 3 year basis). This demand acceleration has been felt by producers across the tech spectrum, with multiple firms guiding estimates higher for the second half based on rising sales to People's Republic.

Our Technology team posted on this data earlier today, in which they noted that order trends are starting to exhibit familiar expansion patterns on a longer term basis.

Although today's improving data disappointed many, we still see confirmation that consumer demand is strengthening in China -perhaps not enough to offset Taiwan's lost business in Europe and North America completely, but more than enough to support our strategic stance on "the client" himself.

Andrew Barber

Director